It wasn’t that long ago when an entrepreneur’s marketing options were limited to flyers, tacky magazine ads, or expensive TV commercials.

However, with the advent of the Internet, the number of marketing options available to both budding and experienced entrepreneurs has become staggering.

Sometimes, when I’m surfing the web—it’s what I do a lot—I find myself thinking, “Wow! So many tactics! So many choices!”

If I were just getting started in digital marketing, I would be in a total freakout mode. Where do I start? Which one should I pick? What do I need to do first?

But it gets worse. Few businesses have the luxury of trying a lot of tactics. Marketing costs money—quite a bit of it, actually. And if you’re just testing out a bunch of tactics, you’ll run out of money before you run out of tactics.

Thankfully, with a little bit of know-how, you can achieve more marketing success than you ever imagined, even on the tightest budget.

How do you go about shaving thousands of dollars off your digital marketing costs without sacrificing the quality and results of your marketing campaigns?

Seems like a tough call, right?

Maybe not as tough as you think.

I’ll show you how.

First, some ground rules

Before I delve into all of the juicy strategies for increasing the success of your digital marketing while saving money, I want to discuss the most important principle of this whole article.

Here it is: less is more

The ultimate goal of all the points I list below is this: eliminate the fluff from your marketing strategy, and focus only on the things that work.

This is why I recommend minimizing your approach and using the 80/20 rule. This rule dictates that

80% of your results come from 20% of your marketing.

You need to understand that this means that you’ll have to give up good marketing opportunities—but only so that you can take advantage of the great ones.

If you are looking to save thousands, you want to put your focus and your money only into the opportunities with the highest yield. That way you can not only save money but also increase your results.

With that in mind, let’s begin.

1. Create a rock-solid strategy

I know that the title of this article promised to teach you “surprising” things you need to put in place for a great marketing strategy. Some of you may be scratching your heads right about now, wondering why I put something so seemingly obvious as a rock-solid strategy as the first point in this article.

Quite simply, I put this first because most people don’t do it!

We live in an era when entrepreneurship has such a low barrier to entry that many first-time business owners and online marketers just throw stuff at the wall to see what sticks.

They don’t ever take the time to develop a proven plan of action with contingencies, review processes, and clearly defined goals.

Sure, it may not be the most exciting part of digital marketing, but it sure is the most important.

Before you even begin to try to save money on your digital marketing, you need to have a clear strategy in place.

Are you wondering how to create a strategy? Here are some questions you should ask yourself:

- How much will I spend? This question is essential since it prevents you from spending money on low yield opportunities.

- What are my goals? Do I want increased traffic, sales, SEO ranking? Everyone wants revenue as the ultimate goal. Back down from this top-level goal, and figure out what KPI-related goals will get you there.

- What competencies do I have that can help me determine which channels to use? Am I good at SEO, copywriting, ad design? Use your existing skill set and resources to determine which marketing channels you’ll be focusing on.

Don’t just ask these questions. Answer them. And write your answers down.

There. Now you have a strategy.

Remember, like the Navy SEALs say, “The more you sweat in training, the less you bleed in battle.”

Or in our case, “The more you plan in marketing, the less you spend on useless garbage and experimentation.”

Trying out new marketing tactics like Kim Kardashian tries on new outfits will only waste time and money.

Get your strategy in place, and the smart tactics will follow.

2. Hire a team of experts for your niche

While it’s common sense to allocate a sizable amount of your budget to hiring experts and consultants with experience in digital marketing, it’s paramount to hire the right experts.

Who are the right experts? People who have experience in your specific niche.

Just because someone is good at digital marketing doesn’t mean they are the best fit for your company.

Remember, you need to find the best options, not just good ones.

How would you like to have the guy in the middle working with you on your music label?

If you run a copywriting firm and are looking to rank higher on Google, what should you do? Hire an SEO expert with a portfolio full of previous clients from copywriting firms for whom they were able to boost rank and quantifiably improve results.

This will ensure you are hiring someone who not only knows the trade but understands how to optimize in your niche as well.

3. Set up a tiered approach to your marketing

It’s easy to get caught up in pursuing all the latest marketing fads and trends. The result, however, is not fun. You spread yourself too thin instead of focusing on one thing and mastering it.

This is why I recommend a “tiered” approach to marketing.

What exactly does this mean?

Basically, create a list of 3-5 digital marketing mediums where you have a certain amount of strength and expertise or affordable access to people who do.

Next, decide what strongest one is—the one you believe will have the highest ROI based on the data for your industry.

Master that one.

I mean really master it. Don’t be content with a novice status. You’ve got to nail this thing!

Once you master the first medium (I’d say Facebook Ads), you can move on to the next one.

Keep doing this until you have mastery over several forms of digital marketing.

If you take this approach, you’ll be able to understand the best practices for each medium, know how to optimize your investments within each medium for maximum ROI, and automate your marketing systems.

You’ll be amazed at the impact. Not only are you gaining solid ROI, but you’re also building a foundation for future marketing efforts.

For example, let’s say you own a landscaping company in Tennessee. You understand Facebook marketing, AdWords, and have a basic grasp of SEO.

Your approach may look something like this:

- Master Facebook marketing with a budget of $1,500/month and an ROI goal of $2,250 a month.

- Once you hit your ROI goal and have created systems or hired experts that allow you to continue this marketing, move on to AdWords.

- Using the ROI from Facebook, invest into AdWords marketing with a budget of $750 a month and an ROI goal of $1,500.

- Now, you have mastered both mediums. Plus, you’ve been able to boost your ROI within each. You are now spending a total of $2,000/month for digital marketing between the two mediums but netting $5,000/month. You’re already winning. But don’t be content.

- You can now systematize both your Facebook and AdWords marketing based on the mastery in each field. Use a set amount of the profit from the marketing to fund your next step, maybe SEO.

- And on and on it goes until you start dominating each marketing medium.

You see, most people (myself included) dive into a new project and focus on far too many things at once, blowing their budgets and diminishing the potential for their ROI.

By limiting yourself to a single medium at a time, you’ll be able to master each one and save yourself time and money in the long run.

4. Analyze your metrics, and be willing to adjust

If you’re familiar with Murphy’s Law—”anything that can go wrong will go wrong”—you understand the struggle many digital marketers face.

Even if you have a rock-solid strategy, completed an 80/20 analysis of your business, have a team of experts at your disposal, and you are focusing on one medium at a time taking a tiered approach, you can still fail at your digital marketing efforts.

Which makes this point the most important.

Analytics.

And pivoting.

Marketers must know their numbers. Become BFFs with Google Analytics or whatever analytics platform you choose. Know your numbers. Understand them. Interpret them.

The only way you can make smart marketing decisions is with data!

For example, if you have an analysis system in place, you’ll be able to see why your conversion rates significantly increased between the 15th and 22nd of June. Then, you would be able to replicate the process moving forward.

You wouldn’t know any of that if you aren’t tracking your progress and monitoring your analytics!

To be successful in digital marketing and save yourself thousands of dollars, you need an efficient way to analyze your efforts.

This happens through knowing data.

For example, let’s say you have gone against my previous advice and are trying to master Facebook marketing and AdWords at the same time.

After you’ve run a few campaigns and been investing for a couple of months, you decide to take stock of your efforts.

Let’s say you are spending $10 on AdWords a day and are earning back $10.50. That’s a positive ROI. Great!

But when you look at your Facebook marketing, you notice that you are actually losing money on the ad campaign. You’re earning more likes but seem to be hemorrhaging more money.

This presents an interesting conundrum.

On the one hand, logic would say to ditch Facebook marketing and double down on AdWords. However, depending on your niche and your vision for your company, those likes and views may be worth more than the pennies you are earning from AdWords (especially if you earn money from affiliates or sponsorships).

Without a clearly defined goal and an understanding of your ultimate vision for your marketing, you’ll be like a ship in a storm with no anchor, getting tossed around by the waves of emotion and confusion.

That’s why it’s important to know your numbers, analyze your data, and make strategic pivots based on what you discover.

Once you’ve clearly defined your goals and selected a marketing medium to pursue, don’t be afraid to discard other campaigns and move on.

If you are not seeing the results you want after a reasonable amount of time, pivoting is your best option.

5. Build a personal brand

I’ll let you in on a little secret:

People rarely buy from a company; they buy from a brand.

Others have made this point and even written books about it (so maybe not that much of a secret, after all).

It’s true.

A company is about profits, losses, products, management, revenues, and shareholders. How boring is that?

A brand is about excitement, engagement, smiles, experiences, and personality.

You’ll understand this dichotomy if you recall the old Apple ads.

Think about it: there are thousands of companies failing every year. While there could be a great number of reasons for their demise, one of those reasons is poor branding.

People like to buy from people they trust.

I want you to take a look at the branding behind 3 SUPER successful online entrepreneurs.

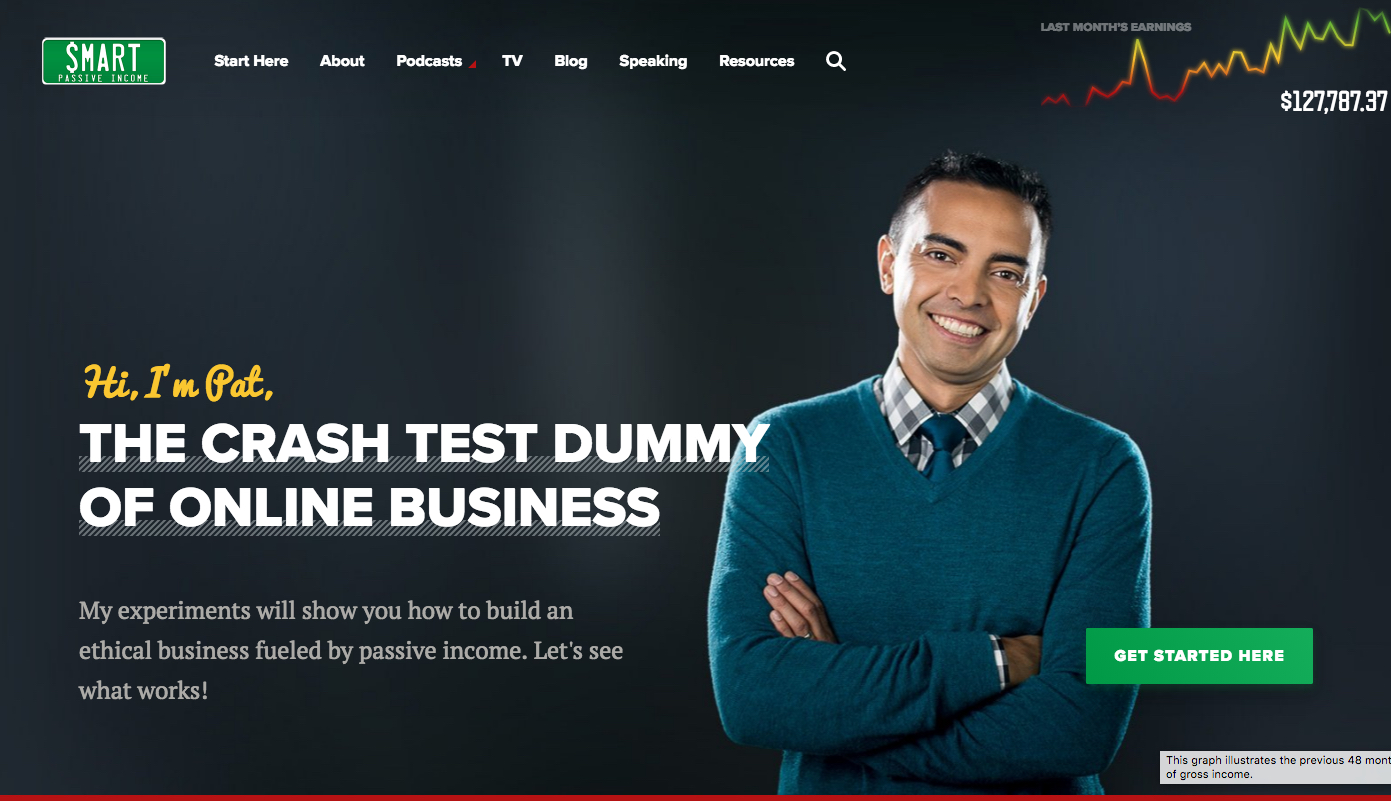

Here is Pat Flynn of Smart Passive Income:

Here is Ramit Sethi of I Will Teach You to be Rich:

And here is, of course, the 4-hour emperor, Tim Ferriss:

Do you notice anything in particular about these blogs…other than the fact that the owners are multi-millionaires?

All of them are about PERSONAL brands. They are focused on the face behind the site, not some ambiguous logo that people can hide behind.

I’m not saying that every business needs to have a figurehead like Ferris or Sethi. What I am saying is that your brand needs personality.

Before you invest a cent into digital marketing, you need to make sure your brand has attitude, emotion, and an authentic feel.

And then, by all means, build your personal brand too—the brand of you.

As an ambassador for your businesses, you can use your personal brand to drive your business.

The better you brand yourself, the less business-focused digital marketing you’ll need to do. People will find you, and they will want to buy from you without needing to be persuaded to do so.

I’ve spent thousands of dollars on courses and seminars I knew very little about. Why? Because I trusted the person selling it and knew their track record as a top performer.

Conclusion

Saving money with digital marketing is more straightforward than many “gurus” would want you to believe.

To have a bigger marketing impact you don’t need a bigger budget.

What does it take instead?

It takes discipline.

It takes discipline to pick a single marketing medium at a time and stick to it.

It takes discipline to invest all your money into your personal brand and continue doing so even when you aren’t seeing an immediate ROI.

It takes discipline to develop a strategy, hire the experts to execute it, and then trust them to do their jobs even when results aren’t coming as fast as you want.

Like most things in life, mastering digital marketing on a budget is simple but not easy.

If it were easy, everybody would do it.

Tactics are tempting, but it’s the rock-solid strategy—driven by experts, strategically structured, backed by data, and built upon a personal brand—that will get you places!

How have you learned to save money while also improving and expanding your marketing reach?

Source Quick Sprout http://ift.tt/29eh2Xz