The longest running bar fight on Main Street has been settled not in the street but in Monroe County Court with a judge ruling in favor of the owner of the Penn Stroud Hotel and against Barry Lynch, the former operator of Jock N' Jills, Sarah's Corner Cafe and the Hideaway Bar.In a 33-page opinion, Judge Arthur Zulick awarded sole possession of the hotel/restaurant premises to Bhavi Corporation, owner of the Penn Stroud in downtown Stroudsburg, and said the Galmay Corporation, the [...]

Source Business - poconorecord.com https://www.poconorecord.com/news/20190617/judge-rules-in-favor-of-penn-strouds-owner?rssfeed=true

الاثنين، 17 يونيو 2019

Questions About Auto Insurance, Electric Kettles, Electric Cars, Allergy Medicine, and More!

What’s inside? Here are the questions answered in today’s reader mailbag, boiled down to summaries of five or fewer words. Click on the number to jump straight down to the question.

1. Prioritizing college or retirement?

2. Types of auto insurance

3. Possibly illegal behaviors of boss

4. Kettle efficiency for tea

5. Buy low, sell high?

6. Generic allergy medications on Amazon

7. Learning how to program

8. Comparing Roth IRA options

9. Firestarters without newspaper

10. Impostor syndrome

11. Inexpensive electric car for commuting

12. Paper planner?

This past weekend was a wonderful Father’s Day weekend. I won’t bore you with the details of everything, but I deeply enjoyed the time I spent with my children doing things I really enjoy, which is about the best you can ask.

On with the questions!

Q1: Prioritizing college or retirement?

34 year old guy, wife’s 33. We have two kids ages 4 and 2. We have been contributing to our retirement plans since starting our current jobs, so I have 6 years of contributions and she has a little less than 5. We have 529 plans for our kids but don’t contribute automatically; instead we put “birthday gifts” and “Christmas gifts” in there and our parents have added more. It won’t add up to a major portion of their college costs though. We are wondering if we should be prioritizing college savings over retirement. Thoughts?

– Ben

Prioritize retirement. To me, it’s not even close. You want to make absolutely sure that your retirement is as stable and secure as you can right now. The best way to see why is to look at some worst case scenarios.

The worst case scenario if you save nothing for your children’s college is that they have to go to college, get student loans, and then pay them off themselves. It’s not fun, but it’s livable.

The worst case scenario if you save inadequately for retirement is that you have to work to a much older age than you want to, have a threadbare retirement, and potentially become a financial burden to your kids. This is a disastrous outcome.

College savings should only be happening if your retirement savings are generous enough to ensure a very stable retirement at a reasonably early date. If you’re not saving enough to get there, then you shouldn’t be saving for your child’s college education.

Q2: Types of auto insurance

Can you break down what the different kinds of auto insurance cover? Insurance guy talks a mile a minute and I don’t feel good asking questions. Googled it but it’s still clear as mud.

– Gary

There are a lot of different types of car insurance. The three most common are the following.

Liability insurance is insurance that covers you in the event of an accident where you’re at fault and you have to pay for damage done to another vehicle. Many states require you to carry this kind of insurance on your car at a minimum.

Collision insurance is insurance that covers damage to your car in the event of an accident with another vehicle, regardless of who’s at fault. It doesn’t matter if you were the one that caused the accident or someone else is, collision insurance will get your car fixed or replaced. Usually, the person at fault ends up covering the damage, provided they have insurance.

Comprehensive insurance is insurance that covers other damage to your vehicle that might occur other than accidents, such as storm damage. The exact things covered by a comprehensive policy can vary, so you’ll want to check into what exactly a comprehensive policy covers.

There are many other flavors of auto insurance that go beyond these to supplement for specific cases. For example, some drivers carry uninsured motorist insurance, which covers you in the event that you’re in an accident with some other driver who doesn’t have any insurance at all, or underinsured motorist insurance, which covers you when you’re in an accident with someone who has a very minimal insurance policy.

As an aside, if your “insurance guy” talks a mile a minute and makes you feel uncomfortable asking questions, you should probably search around for a new “insurance guy.” That’s not what you want out of your insurance contact.

Q3: Possibly illegal behaviors of boss

I have had a family vacation scheduled for early August for several months. My wife and kids and I were planning on going to Disneyworld and Harry Potter and I was taking two weeks off of work. On Friday, my boss called me into his office and told me that if I actually follow through on this trip I would come back to find that I had been fired for some cause that he would find. This seems illegal but I have no way to prove it and I think that if I were fired he would have some unrelated reason to fire me. What can I do?

– Jake

Regardless of how this specific situation turns out, you do not want to continue working for this boss. No matter what specifically happens in the next few months, you need to find a new position with your current employer with a different boss or a new position with a new organization. This is unacceptable treatment. You should start hunting for a new job immediately. Shine up that resume, talk to everyone you know who might help you get another job quickly, and get ahold of headhunters in your field who might be able to get you there.

Your boss is doing this because he believes you have to have this job and have no other options in life. If you go along with this treatment, then you are virtually guaranteeing yourself awful treatment as long as you stay there.

The unfortunate part of this is that you really have no legal recourse for this without some sort of clear proof of this treatment. Your boss knows this, which is why your boss pulled this stunt.

If I were you, I’d just tell my boss whatever he needs to hear to get off my back for the time being, then spend every moment you can getting another job lined up before your Disney World trip. I would not directly agree to skip your vacation at work; rather, I’d push off the issue for now and if pressure continues to be applied, talk to other members of management as the vacation approaches. I would not cancel the trip; rather, I’d do everything I could to have another job in hand before I leave, go on that vacation, and then come back and hand in your resignation letter with whatever notice is appropriate.

Q4: Kettle efficiency for tea

I drink tea a couple times a day. I have an ordinary stovetop tea kettle that I don’t like because the opening sticks. Looking to replace it and am considering an electric kettle. Trying to figure out what is more efficient over lifetime. Electric kettle is more expensive up front but does it make that cost back by being more efficient?

– Carly

A typical electric tea kettle is about 80% energy efficient, whereas heating water on a stove top seems to vary widely in efficiency based on model. This Treehugger article indicates that boiling a cup of water in a typical electric tea kettle consumes 0.04 kilowatt-hours (kWh) of electricity, whereas a convection stove top used 0.11 kWh to heat a cup of water. Each use of the electric kettle, then, saves you about 0.07 kWh.

So, let’s say you drink two cups of tea a day. That means you’re boiling a cup of water 730 times a year. Thus, over the course of a year, you’re saving about 51.1 kWh. The nationwide average cost of a kWh of electricity is about $0.13, so you’re saving about $6.64 per year with an electric kettle versus a stovetop if you’re boiling a cup of water twice a day.

Again, that’s an approximation; the type of stovetop you have, the exact model of electric kettle you have, the cost of electricity in your area, and many other smaller factors will vary these results. However, I’d feel pretty good saying that, given your usage, each year of using an electric kettle would save you between $5 and $10 on your energy bill.

So, is that worth it? I have this electric tea kettle on my desk (it was probably my favorite Christmas gift of the last year). It costs about $70 in most places, but can occasionally be found on sale for $50, but there are cheaper models that get down in the $30 range. There are a lot of traditional tea kettles to be found in the $15 range.

Given your usage level, if you buy a lower-end electric kettle, you’ll end up saving the cost difference in about two years. A fancier electric kettle could take as long as six or seven years to recoup the savings.

Of course, you may be able to find just what you want at a secondhand store for next to nothing, rendering this whole conversation moot. If you can get a $5 electric kettle at Goodwill, that’s your best solution, right there.

Q5: Buy low, sell high?

Don’t understand why you think it’s a bad idea to buy low and sell high. Your stock market advice makes no sense.

– Major

I don’t think it’s a bad idea to buy low and sell high at all. That’s how you make money on investing, after all.

It’s simply my belief that no one on this Earth has any idea what an actual “high” is and an actual “low” is in the stock market, at least to enough precision to be able to beat simply putting money into an index fund each month and forgetting about it until you actually need the money.

If you had the magical ability to predict every single stock market peak right when it peaks and also predict the bottom of every time the stock market drops more than 10% from its peak, then you’d be a brilliant investor. The problem is that literally no one can predict this. The game theory elements behind it – “if you do this, then I do this, but if you know I’m going to do that, then you’ll do this, so should I do that?” – and the real-world nature of what companies are doing makes it impossible for any machine or human to accurately predict the peak or the bottom of the stock market.

The problem is that if you miss those peaks and valleys by very much at all, you quickly erase most of the benefit of market timing, and if you miss them significantly, you’re actually doing worse than just contributing to an index fund like clockwork.

Thus, my advice for almost every investor who would ever read this site is to just contribute to an index fund with every paycheck and forget about it. That’s how people should save for retirement and for other long term goals in life.

It’s not that buy low, sell high is bad, it’s just that with the stock market, knowing what’s actually “low” and actually “high” is essentially impossible, and when you’re just buying kinda low and selling kinda high, you’re not getting enough edge for it to be worthwhile.

Q6: Generic allergy medications on Amazon

Is it safe to buy no name allergy medications on Amazon. They’re so cheap there but I don’t know if they’re safe.

– Ariel

I would have no problem buying generic over the counter allergy medications off of Amazon if I were willing to buy the same exact thing at my local pharmacy. For example, if I went down to my local pharmacy and was trying to decide between buying Zyrtec or generic cetirizine HCl (in other words, “no name Zyrtec”), I’d buy the generic without skipping a beat, and the same would be true buying that exact same item from Amazon.

For example, you can get a bottle of 365 cetirizine HCl tablets on Amazon for $15.99, whereas buying 100 tablets of Zyrtec – basically the same exact thing but with a name brand on it – costs $47.45. The active ingredient in both is the same, but you’re paying almost ten times as much per pill for the name brand.

What about generic Claritin? You can get a bottle of 365 loratadine tablets for $12.34, whereas buying 100 tablets of Claritin – the exact same thing – costs $37.88. Again, the name brand costs ten times as much.

If your pharmacist approves of the “no name” over the counter version of these types of allergy medications, and I sure they will, then ordering them off of Amazon is perfectly fine and a huge money saver for allergy sufferers.

Q7: Learning how to program

How does a person even start to learn how to computer program without taking classes on it? The devs at my company make 2-3x as much as me but I need a lot of skills to get where they are and I can’t even figure out where to start.

– Matt

I think the first thing I’d do in your shoes is figure out what language(s) the developers at your company use and start from scratch learning that language. Just start spending time with them and asking questions, just for your own curiosity. What languages do they use? What software do they use to write code? Then, dig into learning those things from scratch.

It’s hard for me to give any sort of specific advice without knowing what kind of development they’re doing, but your best step is to find a highly recommended beginner’s book for the languages they tell you about. Start with baby steps, even if they seem overly simple, because the difficulty will ratchet up and if you don’t start with the baby steps, you’ll never sprint.

The most important thing you can do is block off very regular and consistent blocks of time to learn. Don’t just decide, “Oh, I’ll learn it here and there.” It won’t work. Block off an hour or two each night to focus on learning how to program.

Once you’re able to write some basic things, come up with small projects for yourself that result in something useful. One of my first independent programming projects was a program for writing and encrypting and retrieving journal entries, for example. I wanted to be able to type out journal entries, save them with a password that encrypted them, and then be able to unlock and read journal entries with that same passcode. I eventually moved onto things like being able to search the entries even though they were encrypted, which taught me a lot about both programming and string algorithms, and that led right into my first career in data mining.

Probably the best free tool I’ve found for self-learning software development is Bento, but for me, I still learn better from a book.

Q8: Comparing Roth IRA options

I know you use Vanguard for your Roth, but how did you come to that conclusion? How do you compare investment houses and their Roth IRA offerings?

– Jana

First and foremost, a Roth IRA must be SIPC insured, which is basically the investment account equivalent of FDIC insurance for bank accounts. Don’t open any investment account that isn’t SIPC insured. For the most part, all brokers and dealers must be SIPC insured so this should be nearly a foregone conclusion. You can check their list of insured companies on their website.

After that, the most useful comparisons are the specific fees of their Roth IRA offerings (what does it cost to just have an account open and to buy/sell things within that account), their customer service ratings, as well as the expense ratios of the investments you’re interested in with each one (the expense ratio is how much the investment company slurps out of your investments each year, usually a fraction of a percent). Ideally, you want your Roth IRA to have no account fees and low expense ratios while having at least decent customer service.

These comparisons led me pretty quickly to Vanguard, but there are a lot of good companies that do well with those criteria – Fidelity usually scores well, as does Schwab.

Q9: Firestarters without newspaper

I used to always use newspaper to start fires but I subscribe online now and there just isn’t newspaper around like there used to be. What’s a good free substitute?

– Eric

There are a lot of things you can do. My favorite recently has been to stuff toilet paper rolls with dryer lint. I just save toilet paper rolls when the roll is empty and keep a small basket in the laundry room for dryer lint. I just stuff the roll with dryer lint and keep several in the garage. When I want to start a fire in our fire pit, I grab one of those and light it first, lighting the roll. The roll is enough to get the lint going and the lint is enough to get a few twigs going, and the twigs are enough to get some big twigs going, and the big twigs are enough to get a log going.

An alternative to the toilet paper lint rolls is to use a paper egg carton instead. Stuff each spot in the carton with lint, then melt an old candle remnant that’s not worth burning any more and pour the wax right on the lint until there’s enough to hold the lint in the egg carton. A carton full of these gives you twelve fire starters – just tear one off and light the paper egg carton part. These work really well but require a bit more prep work than the toilet paper lint rolls.

Another good strategy is to save bark off of any logs you get for firewood. Strip the bark off and save it somewhere and then use pieces of bark very early in the process. The lint in those lint rollers I described work well.

Q10: Impostor syndrome

Graduated college in 2009 and got a good entry level job that I stayed at for five years, then got another job that lasted for three. In 2017, got what I thought would be my dream job, but from day one I have felt utterly incompetent. Every day it is like I am not qualified enough to be here. People seem to like my work but I feel like everything I do whether it’s writing code or writing reports or contributing to meetings is just low quality. It has made it so that I don’t even like going to work. How can I fix this? I think others judge me as being good at my job but I think I am trash and am just hiding it.

– Allen

This is actually a pretty normal thing. It’s called “impostor syndrome,” which refers to the sense that you’re an “impostor” in some aspect of your life where others believe you to have competence that you do not believe that you possess.

I felt it pretty strongly when I started my first job after college. I was responsible for launching and largely writing by myself a software project that was orders of magnitude more complex than anything I had worked on to this point, and I felt really incompetent at the whole thing. It stuck with me for several months at least.

There are a lot of things you can do to overcome impostor syndrome, but the most effective one for me was to keep a running list of my achievements and look at them frequently. Could someone who didn’t know what he was doing actually do all of this stuff? After a while, it became hard to argue against it, so the feeling of being an “impostor” slowly went away.

Personally, my list began to include hitting large project objectives with flying colors. If I were incompetent, would I have been able to pull this off largely by myself? At first, I could think it was a fluke, but as our project kept hitting and exceeding our targets, I eventually realized that, yes, I was at the very least competent at my job.

Q11: Inexpensive electric car for commuting

Do you think an inexpensive electric car like a Chevy Volt or Nissan Leaf is good for a commuting car? Seems like it’s cheaper up front to buy a late model used high mileage gas car but do the electric cars end up saving in the long run?

– Jim

I’m assuming you’re comparing the cost of buying a late model Nissan Leaf or Chevy Volt with the cost of a late model used gas car like a Toyota Corolla. Sarah is thinking a bit about buying a Leaf or a Volt or similar car for her own commute, which is about 45 miles round trip each day.

It’s pretty easy to find a used late model Nissan Leaf around here for about $15,000 with about 40,000 miles on them. Toyota Corollas of the same year clock in about the same for the same price.

Here’s the issue with electric cars: the availability of charging them out and about is somewhat limited. You have to really look into what’s available along your commute for charging. You also have to get a home charging station that can charge your car overnight (most full electrics take a day at least to charge from an ordinary plugin, but a charging station can be installed at a relatively low cost that allows for much faster charging and many electric companies offer a rebate) and you have to get into a routine of charging your car. You can’t just go “Whoops, guess I’ll stop for gas.” It’s simply not quite as convenient as that.

However, the savings are impressive. By our math, we can get about 175 miles of range on a Nissan Leaf for $4 in energy charging at home. For comparison’s sake, even her Prius that she currently drives costs about $14 to charge over that same distance. On fuel alone, driving 15,000 miles a year, the Leaf would save us about $900 a year in fuel. That’s significant, especially if she drives it for several years.

We’re seriously considering toward replacing her Prius (which is over the 200K mark) with a Leaf or a Volt for commuting.

Q12: Paper planner?

I’m trying to understand how you do daily planning. So, you just write down tasks and events free form in your pocket notebook and in your journal and then transfer them into an online calendar and to-do list? And then don’t use a paper planner at all? Do I have that right?

– Jeremy

That’s exactly it.

I keep a pocket notebook and a pen with me pretty much all the time. When a task or an appointment or some other piece of info I need to deal with soon pops up in my life, I write it down immediately either in that notebook or into the Evernote app in my phone. I also do a daily journaling practice, and after I do one of those, I go through it looking for any tasks that I might have thought of while doing it.

A couple times a day, I go through my new notes in Evernote and my recent pages in my pocket notebook and move everything actionable into my to-do list manager (Omnifocus) or into Google Calendar. Those are the things I use for reference.

In short, my actual thinking about tasks takes place on paper, but I use digital tools for storing that thinking as discrete and sortable appointments and tasks.

Got any questions? The best way to ask is to follow me on Facebook and ask questions directly there. I’ll attempt to answer them in a future mailbag (which, by way of full disclosure, may also get re-posted on other websites that pick up my blog). However, I do receive many, many questions per week, so I may not necessarily be able to answer yours.

The post Questions About Auto Insurance, Electric Kettles, Electric Cars, Allergy Medicine, and More! appeared first on The Simple Dollar.

Source The Simple Dollar http://bit.ly/2XRQQsc

Shop Your Way to Better Credit? Amazon Introduces a Credit Builder Card

Amazon, the online retailer that wants to be all things to all people, has just rolled out what may be the retail industry’s first secured credit card.

Aimed at consumers with subprime credit scores or those who have no credit history at all, the card is a smart move for Amazon on many levels.

The Amazon Credit Builder Card is a closed-loop card, meaning it can be used only for purchases on Amazon.com. Thus, Amazon will receive the revenue from any spending on the card.

And in order to get the card, users must provide a deposit of anywhere from $100 to $1,000. (The money will be held by Synchrony Bank, the financial firm Amazon has partnered with to launch the card.)

Bottom line: Offering this card to consumers presents very little risk for Amazon, and a great deal of reward. The company has not only opened a new income stream from the credit card itself, it’s also reaching out to a vast new segment of potential customers.

“This is tapping into a larger trend of 79 million people who have subprime credit and 53 million who don’t even have a credit score,” said Ted Rossman, industry analyst for CreditCards.com. “There are a lot of people who are building or rebuilding credit.”

“This is a smart move by Amazon; there’s a sizable part of the population that is a candidate for this,” Rossman said.

But how good a deal is the Amazon Credit Builder for its intended consumer base — those with subprime credit or no credit history at all? Is it a win-win for them too? Here’s a closer look.

A Foot in the Door

More than 100 million people are credit-challenged, meaning they struggle to access affordable credit because they either have subprime credit scores or are unscorable because of a lack of credit history.

Cards like the Amazon Credit Builder can help this demographic, said Rob Levy, vice president for Financial Health Network.

“When used properly, secured credit cards can be a fantastic tool to help people build or improve their credit, in as little as six months,” Levy said. “Unfortunately, they aren’t well-known or understood by the millions of people who could really benefit from them.”

Indeed, secured cards make up less than 1% of U.S. consumer credit, according to the Federal Reserve Bank of Philadelphia.

The Deposit

Secured credit cards are backed by a payment from the cardholder that’s used as collateral. In the case of the Amazon Credit Builder Card, applicants must provide a deposit of $100 to $1,000, which will be held by Synchrony Bank.

The deposit is not the money you’ll be using to make purchases with. Rather, the cash is held by the bank in the same manner a rental deposit is held by a landlord until you move out.

While the consumer can choose how much money to deposit, this feature still may be somewhat confusing or even a drawback for some of low-income users, Rossman said.

“If you put down $500, you will have a $500 credit line, but you still have to come up with a separate $500 to pay that bill. You can’t use the deposit to pay the bill,” he said. “People often have misconceptions thinking deposit means I’m prepaying for the things I want to buy. There may be a little bit of a cash-flow issue for some people.”

In order to build your credit profile, Amazon and Synchrony Bank want to see that you’re regularly coming up with the funds to make responsible payments, Rossman said.

On the plus side, the minimum deposit on Amazon’s Credit Builder card is low enough that it may make the card accessible to those who have previously been shut out from such opportunities.

“When almost 40% of Americans can’t come up with $400 without borrowing or selling something, the security deposit is often one of the biggest hurdles for getting more people into secured cards,” Levy said. “By lowering the minimum deposit to $100, cards such as Amazon’s make the hurdle much easier to clear for lower-income people.”

The Interest Rates

At 28.24%, the Amazon Credit Builder’s rate is high, Rossman said. However, many retail credit cards have steep rates, he added, with the average retail card charging about 25%.

Issuers charge more interest for retail and secured cards because such cards are often easy to get. But that steep interest could be an issue for some users — particularly those who are not responsible with repayment.

“Secured cards typically have higher interest rates than unsecured credit cards, so if consistently maxed out and not paid off, consumers can face significant fees and can actually lower their credit score,” Levy said. “However, a secured credit card’s limit is usually set to be the same as the security deposit amount (typically around $300), so the impact of a slightly higher APR isn’t huge and the chances of getting into significant debt are limited.”

Users should also be clear about the fine print with regard to the Amazon Credit Builder’s 0% offers for larger purchases. For instance, for purchases of $149 or more on the Credit Builder Card, users are eligible for 0% financing for six to 24 months.

Purchases of $300 or more are also eligible for 0% financing, but cardholders must adhere to what’s known as “Equal Pay Financing,” a repayment structure that requires making equal payments every month for 12 months.

The concern about these options is that they may cause consumers to overspend. What’s more, there’s often a lack of understanding of how 0% financing works, Rossman said.

“The thing some people get trapped by is the 0% promotions,” Rossman said. “They have a big ‘gotcha’ to be aware of, and that’s the deferred interest. “When they say 0% for 12 months, that means if you don’t pay in full by the time that time clock runs out, they’re going to charge you back interest, on your average daily balance, all the back to the beginning.”

The Payoff: Upgrade to a Regular Card in 7 Months

For those who do manage to make responsible, consistent payments, the reward is Amazon’s offer to allow users to upgrade to a regular credit card after seven months. It’s yet another attractive feature for those working to build their credit.

“I think this is a really good starter card,” Rossman said. “It’s incredibly easy to get because you’re putting down a deposit. And if you have good payment history, they will evaluate you for an upgrade to their regular card. There can be some pretty quick improvement using this card. You can rebuild a subprime score or build a new score relatively quickly.”

But to truly reap the credit improvement benefits being dangled by this card, Levy adds one last tip: Keep your credit utilization low.

“In order to maximize the positive impact on a credit score and limit fees paid, secured card users should keep their credit utilization to less than a third of their overall credit limit and should pay their balance in full every month,” Levy said. “In that regard, a retail-based secured card such as Amazon’s, which is limited to store or site purchases only, may actually make it easier for consumers to keep their balances at the right level and not overspend.”

Read more:

- Like it or Not, a Secured Credit Card May Be the Key to Rebuilding Your Credit

- Best Credit Cards for Bad Credit

- Two Rewards Cards Every Amazon Prime Member Needs

Mia Taylor is an award-winning journalist with more than two decades of experience. She has worked for some of the nation’s best-known news organizations, including the Atlanta Journal-Constitution and the San Diego Union-Tribune.

The post Shop Your Way to Better Credit? Amazon Introduces a Credit Builder Card appeared first on The Simple Dollar.

Source The Simple Dollar http://bit.ly/2ZDbM6T

The Ultimate Guide to Content Marketing For Ecommerce Websites

Content marketing has arguably become the biggest buzzword in the marketing industry today.

It seems like you can’t have a conversation with a business owner who has an online presence without the term being brought up. Every online “expert” claims to hold the secret to content marketing.

But the reality is this. Like most marketing strategies, what works for one business won’t necessarily work for another. Content marketing campaigns will vary by industry as well.

So what exactly is content marketing?

By definition, it’s the process of creating and distributing digital materials online to directly or indirectly promote a brand, product, or service.

But that definition is so broad. To have a successful content marketing strategy as an ecommerce website, you need to take an ecommerce-specific approach.

Your content strategy won’t be the same as a B2B SaaS company or a B2C local retailer without an online presence.

I’ve seen countless ecommerce sites get so caught up in their marketing plan, that they actually lose sight of what drives their business. Rather than trying to copy the content strategy of a competitor (who may or may not have a good approach) you should be focusing on ecommerce conversions.

Everything you do needs to drive conversions. That’s the ultimate way to survive as an ecommerce shop.

So if you can’t directly or indirectly connect conversions to your content strategy, then it’s a wasted effort. That’s what inspired me to create this guide.

I want to clear up any misconceptions that you might have about content marketing and how it works. I’ve outlined a straightforward content marketing approach that’s specifically designed for ecommerce shops.

Ecommerce content marketing process

Before you start blogging or uploading videos to YouTube, you need to establish a clear plan for your content strategy. Remember, everything you do ultimately needs to drive conversions.

This is something that I encounter all of the time when I’m consulting with ecommerce companies.

They start to tell me about their plan, which sounds great in theory, but they don’t know the “why” behind the strategy.

For example, let’s say you’re putting all of your efforts into advertising on LinkedIn. You saw some information online about how many users are on the platform and how much it’s been growing over the years. Must be a good place to deploy a content marketing campaign, right?

For some businesses, sure. But that’s not the case for ecommerce.

You would know this if you took the time to create a plan before putting a strategy in motion. I’ve simplified the planning process into three easy steps. It’s crucial that you follow them in order.

Step #1: Identify your target audience

I know this may sound simple, but you’d be surprised at how many people don’t know the answer to this question. Take a moment to see if you really know your target audience.

Here’s the thing. Your target audience needs to be crystal clear before every content marketing campaign. Otherwise, it won’t have a high success rate and lead to conversions.

Without knowing your target audience, you won’t know how to reach them.

- Age

- Gender

- Location

- Likes

- Dislikes

- Habits

These are just the basics that you need to know, at a minimum. Identifying the target market of your startup is something that you should have done a long time ago. But your overall audience isn’t always the same for individual campaigns and strategies.

For example, let’s say your company sells sports equipment online. Your audience isn’t just “people who play sports.”

You can’t tailor your content around that because it’s way too broad. High school softball players aren’t the same as middle-aged male golfers.

Step #2: Learn their online habits

Remember, content marketing is all about distributing digital touchpoints online. That’s why it’s so important to figure out who your audience is.

You need to know where these people live online. Otherwise, you won’t know how or where to distribute the right content.

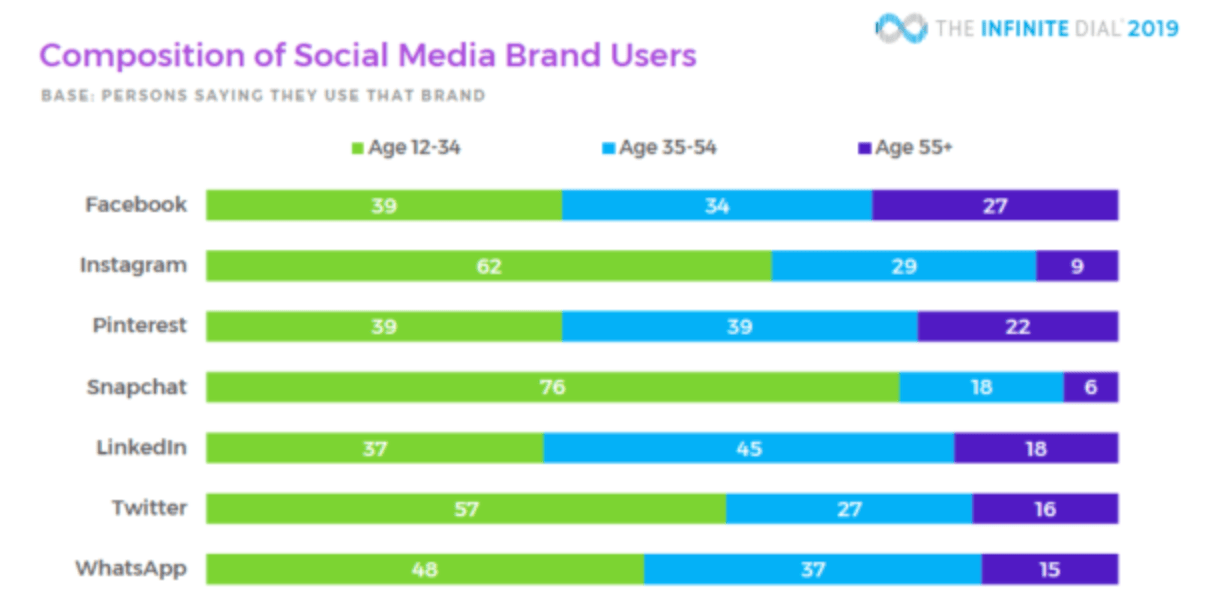

Social media is a great way to distribute your content. Here’s a basic breakdown of social media usage based on age.

This will tell you more about your target audience, but it’s still not enough information.

Sure, based on this graph, you could eliminate the possibility of targeting users over the age of 55 on Instagram and Snapchat since they only make up 9% and 6% of the population on those platforms, respectively.

However, other times broad information like this can be misleading. Take a look at the Snapchat usage. 76% of Snapchat users fall between the ages of 12 and 34.

So if you’re targeting younger consumers, like Millennials or Generation Z, this might seem like the place to do it. But you need to learn their habits as well.

For simplicity sake, let’s continue using the example from before. You have an ecommerce sports shop, and you’re trying to sell equipment to high school softball players.

If you assume that Snapchat is the best place to distribute your content, you’re making a mistake. You haven’t done all of the research yet.

In fact, 49% of Generation Z females say that they prefer to use Snapchat for sending videos of themselves. 43% of that same group says they prefer using Snapchat for posting selfies. They don’t use this platform to interact with brands.

However, 48% of Generation Z females say that Instagram is their preferred social media network for following brands.

Even though Snapchat has a greater marketing penetration of your target audience, it doesn’t matter if they’re not using that platform to interact with businesses online.

You can’t make assumptions about habits. I alluded to this earlier about LinkedIn. While your customers may be using the platform, that network is designed for B2B marketing, not B2C ecommerce shops.

Step #3: Create and distribute content

Once you figure out what platforms are the best places to distribute content for your previously identified target audience, now you can start to create content.

If you start building the content before you go through the first two steps, it’s a big mistake. You might be wasting your time creating content that people won’t end up seeing or using.

Let’s say you’re spending 90% of your content marketing resources on blogging. But your audience is consuming content on YouTube and Instagram. That’s not an efficient use of your resources.

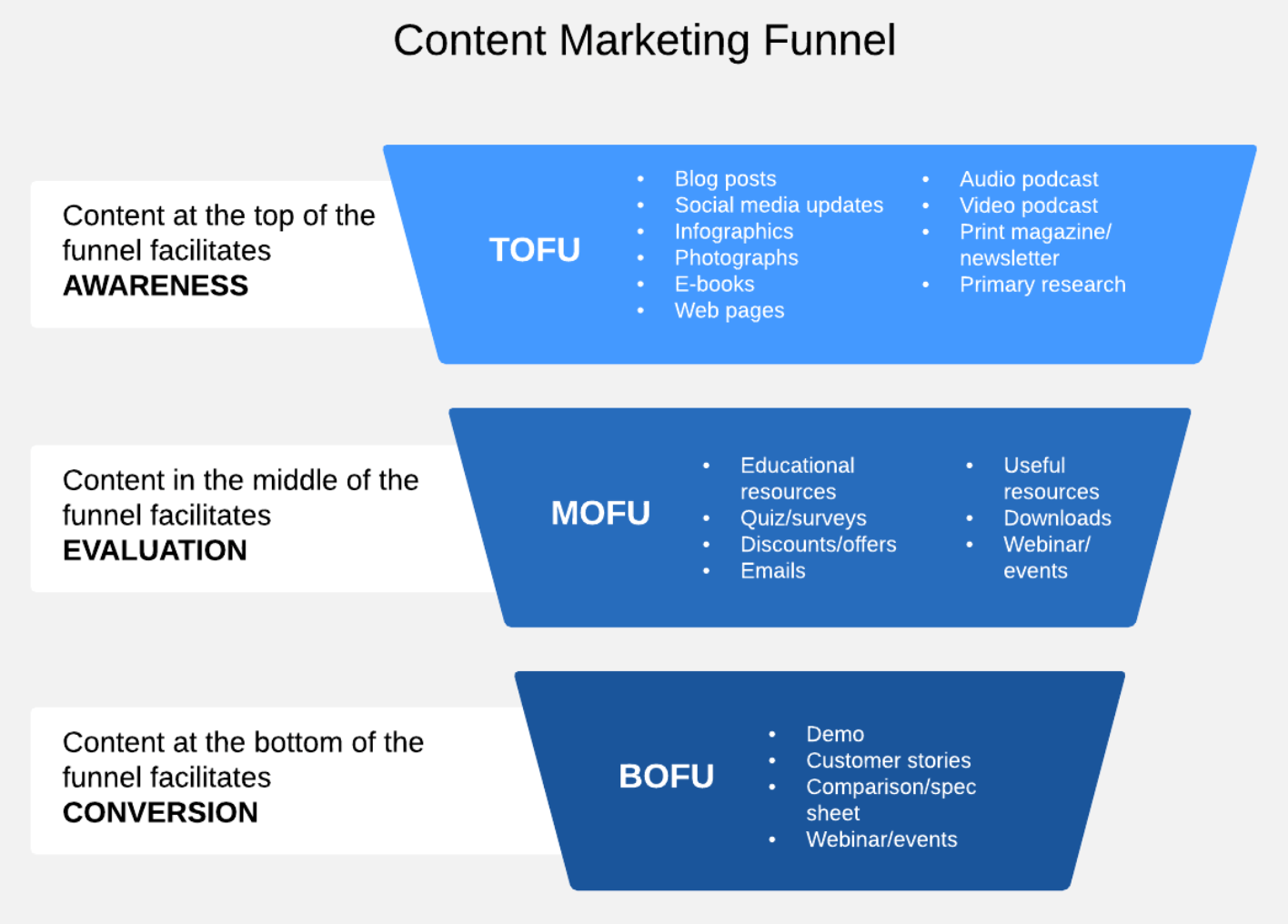

The type of content you create will also depend on who you’re targeting people based on their stage in the marketing funnel.

This graphic is a great resource to give you inspiration for content ideas.

A consumer who has never heard of your brand or ecommerce site will be targeted differently than repeat customer who knows what they’re looking for and is ready to make a purchase.

Breaking this entire process down into these three steps simplifies content marketing for ecommerce brands. But if you mix up the order of these steps, it won’t be as effective.

Types of ecommerce content marketing

Now that you understand the approach behind content marketing for ecommerce sites, it’s time to look at some more specific types of content that you can use for your campaigns.

Keep in mind, not all of these will be applicable for every campaign you run. The content will always vary and be based on who you’re targeting and the platforms you’re planning to distribute on.

Blogging

I always recommend starting your content marketing strategy with blogging. While this may not be the most popular approach for ecommerce companies, it’s very beneficial in terms of SEO.

There are ways for you to scale your lead generation through blogging as well.

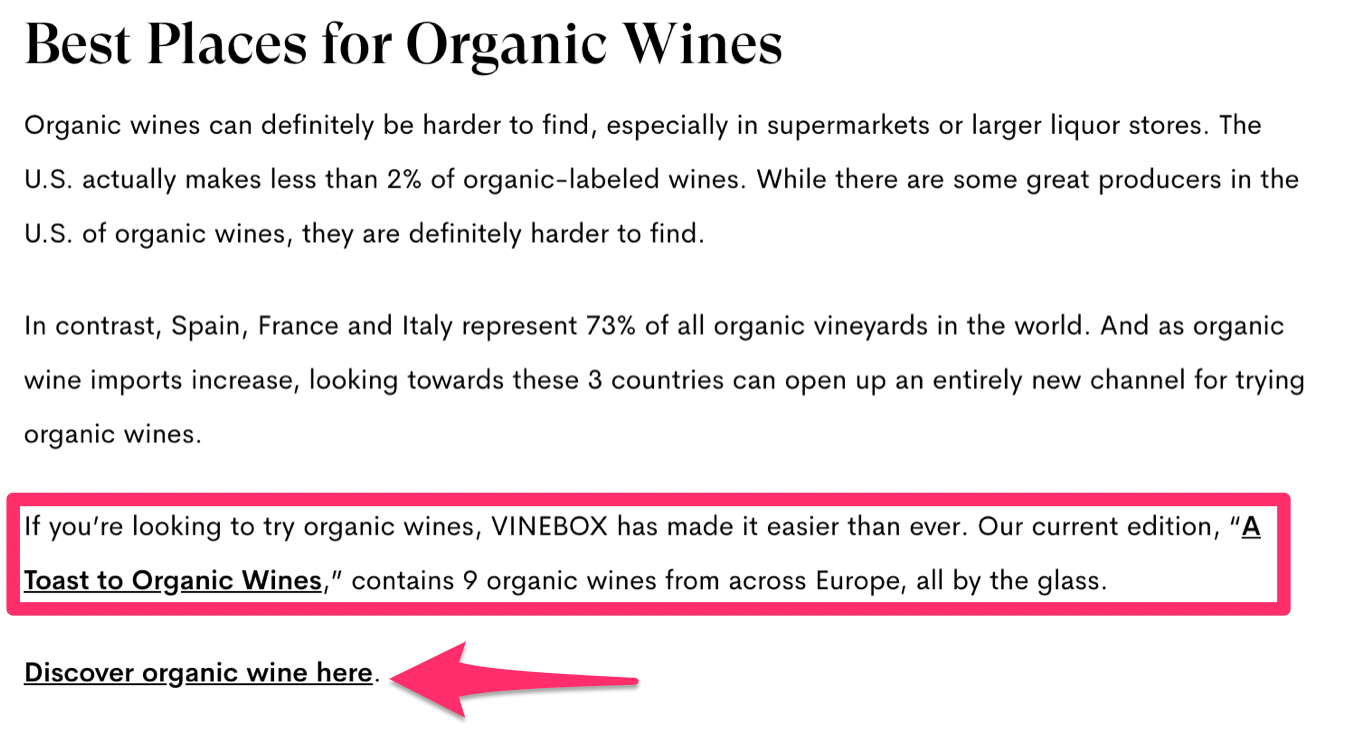

Let me show you an example from Vinebox, an ecommerce store that sells wine.

Here’s a blog post I pulled from their site about the benefits of drinking organic wine.

So if someone is browsing online and searching for more information about organic wine, how it works, and the effect it has on their body, this post can pop up. People can navigate to this website even if they never heard of Vinebox.

As an ecommerce shop, you’re competing with dozens, hundreds, or even thousands of other brands across the web. You can’t rely on all of your customers going directly to your site to buy.

While this page serves as an informational guide on organic wine, it’s also designed for conversions.

This is the final section of the blog post.

The blog closes with two CTAs about buying organic wine directly through their website. It’s a simple, yet effective approach.

You can definitely mimic this strategy for blog posts related to the products you’re selling online.

Original photos

The biggest challenge of selling online is that customers can’t touch and feel what you’re offering before they buy it.

They rely heavily on visuals for this. So it’s up to you to ensure that you have tons of pictures of your products from nearly every imaginable angle. This is necessary for your product pages, but you can also repurpose those images on other channels as well.

For example, you can take an original photo of a model wearing the clothes that you’re selling and turn it into an Instagram shoppable post.

Again, this is only under the assumption that you’ve done the right research and recognized this platform as a place to reach your target audience.

Include photos in your blogs. Add them to your email campaigns. Share them on other social media channels. Keep taking original photos because you’ll always be able to find a use for them.

Video content

This piggybacks off of my last point about how consumers need to see your products before they buy anything.

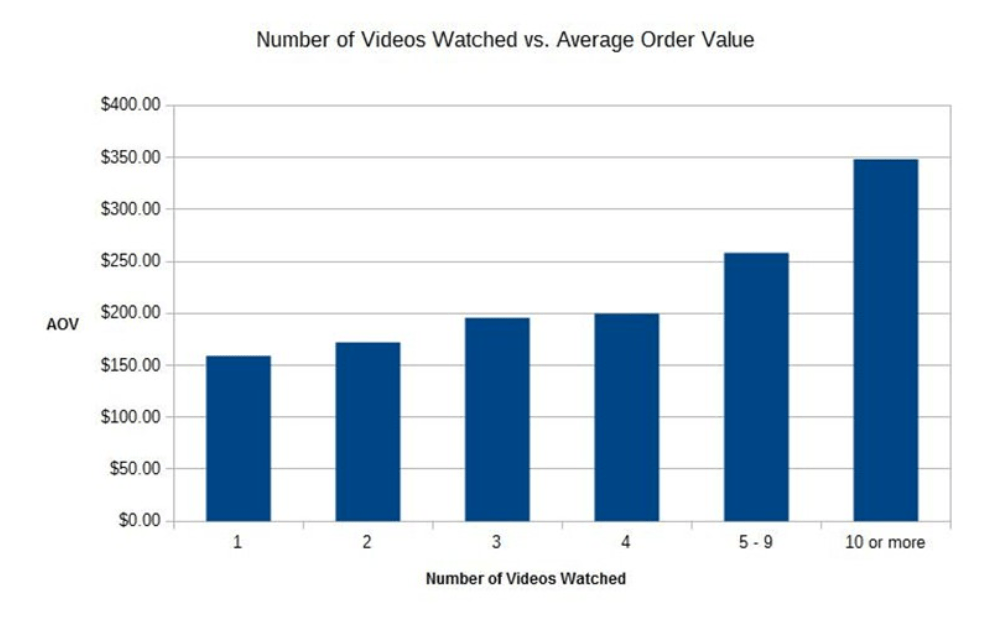

Images are somewhat limited, but videos can tell the full story. Just look at how big of an impact video content has on purchases.

The more videos people watch about a product online, the higher their average order value is.

Videos can also be repurposed across multiple channels. Your blog, product pages, email campaigns, and social media profiles are all great places to distribute.

Furthermore, 90% of consumers say that videos assist their buying decisions. 54% of consumers want to see more video content from brands they support. Videos on landing pages can increase conversions by up to 80%.

Just adding the word “video” to an email subject line can increase your open rates by 19%.

- “How to” videos

- Product demonstrations

- Brand advertisements

- Interviews

- Animations

- Live video broadcasts

The list of possibilities goes on and on. Video content must be incorporated into marketing strategies for all ecommerce sites.

Product buying guides

Product buying guides are essential for the same reason as blogs. They can be used to drive organic traffic to your ecommerce site when people are looking for more information about specific products.

The biggest difference between product buying guides and blogging is that they will each target different types of people.

Blog posts are typically ToFu (top of funnel) content since the consumer is still in the product and brand awareness stage. On the other hand, product buying guides are MoFu (middle of funnel) content as the consumer reaches the evaluation stage of the purchase process.

Make sure that all of your buying guides have CTAs to drive conversions.

Email marketing

Truthfully, email marketing isn’t just an ecommerce-specific content marketing strategy.

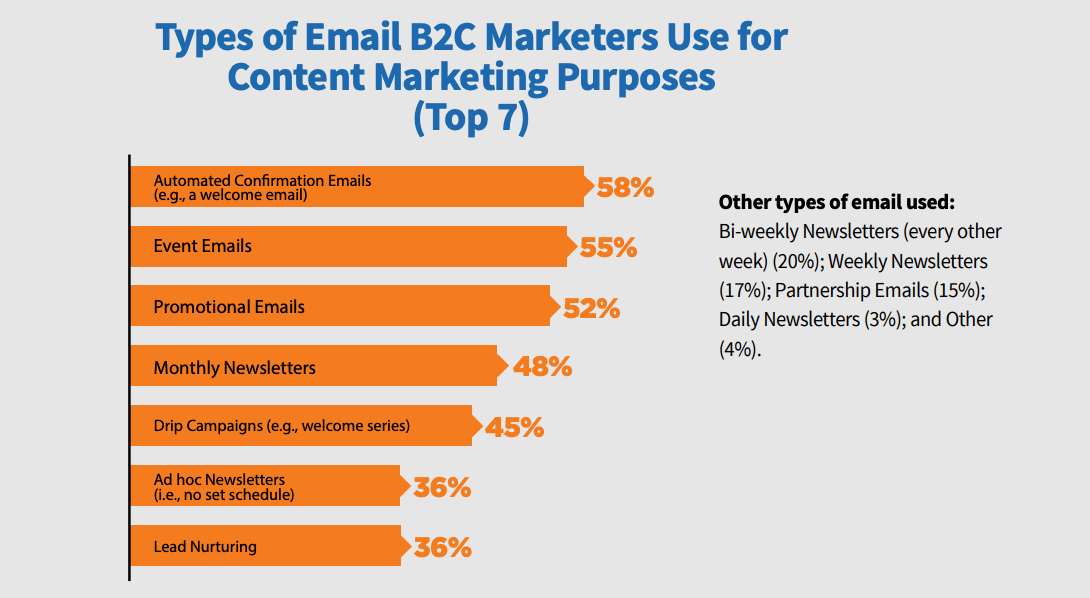

But with that said, there are definitely ways that your ecommerce shop can leverage emails that other businesses cannot. Here’s a look at how B2C marketers are using email marketing.

Your ecommerce site can take this to the next level.

Any time someone makes a purchase on your website, you have the opportunity to send them a drip campaign that’s relevant to that order.

- Order confirmation

- Shipping notification

- Package delivered

- Follow up

That’s four emails that you have an excuse to send. All of them are relevant to the customer and provide information that they want to see.

You can use these messages to drive more conversions. Provide discount codes off of an upcoming purchase. Show product recommendations based on what they bought.

If a customer buys a surfboard, send them an email about a wetsuit. If they buy workout shorts, send them an email about more new workout gear.

Customer stories

There are lots of different formats you can use to tell a customer story.

- Reviews

- Testimonials

- Case studies

These can be in text format, image format, videos, or blog posts. Display them on your homepage. Create separate landing pages for customer stories. Share them on social media.

If you look back to the content marketing funnel that we talked about earlier, customer stories fall into the BoFu (bottom of funnel) category.

At this point, the consumer is close to converting. The customer stories can be the factor that drives them to complete the purchase process.

Interactive content

Adding interactivity to your content strategy is a great way to bring a personalized touch to the customer.

Here’s an example from the Beardbrand website.

When you land on their homepage, you aren’t shown any specific products, and they don’t have any CTAs saying something like “buy now.”

Instead, there is an original photo of three men, each with three very different beards. There is a link to a quiz that will “help you find the perfect product.”

This interactive quiz makes the customer feel confident about the product that they’re purchasing. By answering a series of questions designed to meet their needs, it gives them an incentive to buy.

Conclusion

There are lots of misconceptions about content marketing and how it works. As an ecommerce business, you need to look for strategies that are specific to your industry.

Before you do anything, you need to know the process for ecommerce content marketing.

- Identify your audience

- Find out how to reach them online

- Create content and distribute them on those platforms

When you take this approach, everything else gets easier. Just remember that every content strategy you apply needs to ultimately drive conversions.

Keep this guide as a reference, and use the examples I listed above as inspiration for some high-converting content strategies.

Source Quick Sprout http://bit.ly/2wVt4Qe

This App Will Give You Cash Back for Eating at Chipotle

Some of the links in this post are from our sponsors. We provide you with accurate, reliable information. Learn more about how we make money and select our advertising partners.

I lived on Chipotle in college.

Could I afford it? Not really. But that wouldn’t keep me away from that flavorful cilantro-lime rice, the juicy carnitas, those giant dollops of sour cream or the warm tortillas.

I mean, it could’ve been worse (ahem, Taco Bell). But it also could’ve been way better if I’d known how to save money at Chipotle. My only trick? I’d wear my Halloween costume to get a $3 burrito.

Luckily, it’s way easier to save money at Chipotle these days. Just download the free Ibotta app, and start earning cash every time you dine.

How to Earn Cash Back on Chipotle Orders — For Life

You might’ve heard of Ibotta. It’s known for helping savvy shoppers earn cash back on groceries. (We once talked to a woman who earned $432 in cash back in a year!)

But Ibotta can also help you earn cash back on flights, Amazon orders, Uber rides — you name it.

Now, it has another fun perk called “Pay With Ibotta.” It’s an easy way to earn instant cash back from dozens of retailers and restaurants, including Applebee’s, Bed Bath & Beyond, Old Navy, Lowe’s and — yup! — Chipotle.

Here’s what you have to do to start earning cash back:

- Download the app, and create your account.

- Connect your debit or credit card by tapping “account” then “payments.”

- Peruse your cash-back options. When you’re at one of the listed restaurants or retailers, tap its name, and add the checkout amount. Then Ibotta generates a QR code or barcode you’ll hand to the cashier to scan.

You’re done! The cash will be added to your earnings instantly.

I mean, what better excuse do you have to go to Chipotle now?

Carson Kohler (carson@thepennyhoarder.com) has thankfully recovered from her Chipotle obsession.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://bit.ly/2InVXv2

الاشتراك في:

التعليقات (Atom)