The world of technology is constantly evolving.

As a marketer, you need to stay up to date on new advancements that could benefit your company.

You don’t want to be left behind while your competitors forge ahead by adapting to the new world.

In my consulting work, I often see marketers and business owners who don’t believe these advancements are relevant to their marketing strategies. But this couldn’t be farther from the truth. New types of technology such as AI and machine learning are reshaping marketing.

While the technology is advancing rapidly, the basic concepts behind its applications remain unchanged. Everything is still focused on the customer.

Your marketing efforts need to reach your target audience. Your campaigns must find ways to speak to these people, and you can achieve that by personalizing and improving their experience.

Predictive analysis can make this possible.

Some of you may already be running campaigns and have strategies in place that focus on improving the customer experience and personalizing content.

However, predictive analysis technology will bring these ideas to the next level. You’ll see what I mean as I continue.

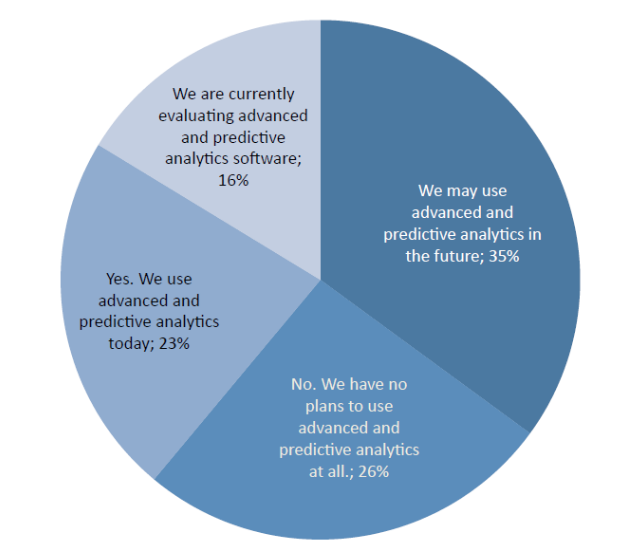

Surprisingly, only 23% of businesses are currently using advanced and predictive analysis tools:

That said, about 90% of businesses believe it’s at least somewhat important to implement predictive analysis tactics in their strategies.

What does this information tell you?

Well, it seems as though the vast majority of business owners and marketers recognize the need for predictive analysis, but they just haven’t proceeded.

Since you’ve navigated to this guide, I’m assuming you fall into this category. Or maybe you fall into the 16% of marketers currently evaluating advanced analytics software.

People want to use this technology, but they don’t know where to start or how to apply it. This was my inspiration for this guide.

You need to be able to adapt. In fact, adaptability is one of the top marketing skills you need to survive in the age of AI.

Making the decision to move forward with predictive analysis is the first step.

Now you need to figure out how this technology will improve your marketing strategy. If you apply the concepts I’ve outlined in this guide, you’ll have a huge competitive advantage.

Enhance your customer segmentation strategy

Your customers don’t fall into the same group.

Treating all people the same is not an effective marketing strategy. I hope you’ve already started segmenting your customers.

Marketers have been doing this well before the days of big data. But this can be drastically improved with predictive analysis.

Predictive analysis can make it easier for you to compile demographic data. I’m referring to parameters such as:

Typically, it’s easy to learn this information about your customers. But segmenting them by those factors alone is not enough.

By using predictive analytics technology, you can identify trends for deeper segmentation.

You’ll ultimately pair demographic data with psychographics. This type of information can be obtained from social media, website analytics, surveys, and focus groups.

It doesn’t stop there. You can also collect behavioral data, such as how each customer uniquely uses your service or platform, e.g., your website or mobile app.

When you combine all the demographic, psychographic, and behavioral data about your customers, your predictive analysis model will create segmented groups with greater accuracy than it would if it used only one type of information at a time.

You can create customer personas once the data has been optimized from the predictive analysis formulas:

Once the segments have improved, your customer personas will be more precise and targeted accordingly.

Customer personas and customer segmentation are not quite the same although they’re often confused with each other. Ultimately, the two concepts work together.

With the information you get from your advanced segmentation strategy, you’ll be able to build a customer persona. These personas will be used for driving sales and conversions.

You can eventually use your predictive analysis software to improve lead scoring.

Once someone has been properly segmented, you can send them the right campaign, which will make it easier for them to convert. I’ll discuss lead scoring in greater detail later.

Improve automation

Customer personalization needs to be a key part of your marketing strategy.

But efficiency needs to be a priority as well.

It’s unrealistic for you to manually analyze every customer in your database. Most people leverage basic details with their automated platforms.

They use basic factors, such as the customer’s name, email address, location, and maybe their age.

For example, you could have an automated email go out to a customer on their birthday. This strategy is OK, but it can definitely be improved.

By using your customer segments and customer personas, you’ll be able to have a more advanced automation strategy.

With this type of data, you can create campaigns to show your customers you fully understand their wants and needs. Furthermore, you’ll know how to address those wants and needs.

Once your automation efforts improve, it will be much more profitable for your business.

That’s why such a large majority of marketing executives who have been using predictive analytics to improve their marketing strategies are seeing a high ROI.

If the initial cost of this type of software is holding you back from investing in it, know that you’ll ultimately see a return on your investment.

Reduce churn

When businesses focus only on customer acquisition, allowing their retention strategies to become an afterthought, they underperform.

If this sounds like you, you’re making a big mistake. It’s much easier to sell to your current customers than to new ones.

In fact, you can even increase revenue without acquiring new customers.

These tactics should be a priority for your marketing department.

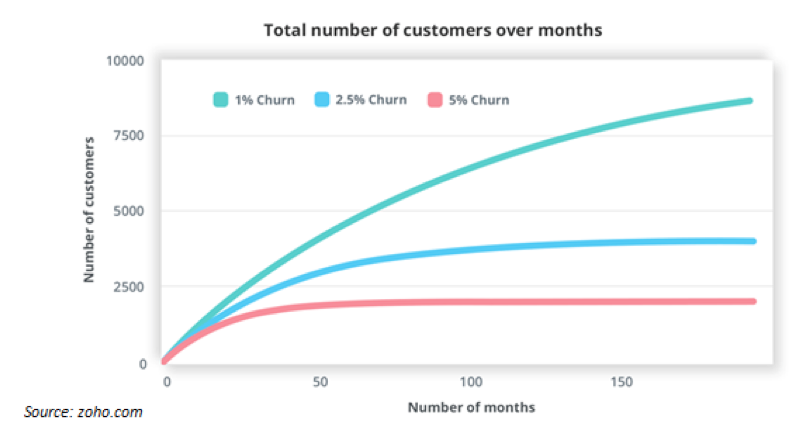

But even customers who have been with you for a while may eventually churn. What are your current churn rates?

We know that 70% of SaaS companies have an annual churn rate of about 10%.

Don’t think that’s a problem? I think that’s way too high.

Those of you with a high churn rate are missing out on much potential income.

If you can reduce your churn, you’ll have more money in your company’s bank account.

Predictive analysis can help show you when a customer will churn based on their behavior. Then, you can have targeted and automated responses in place to prevent that from happening. This will give them an incentive to stay.

You may not realize it today, but your churn rates can be detrimental to your company over time. Just look at this graph:

Notice the difference between the churn rates of 1% and 5%. That’s huge.

Check out the difference between 1% and 2.5%. I’m sure that’s not what you expected, given the small percentage number.

As you can see, improving your churn rate even by a percentage point or two will be a huge advantage for your company. This is especially true as you continue to acquire new customers over time.

Make decisions in real time

With predictive analysis tools, your company can benefit from speeding up the decision-making process.

That’s because you’ll get predictive results in real time.

The longer it takes for you to make a decision based on the information you’re given, the less effective that decision becomes.

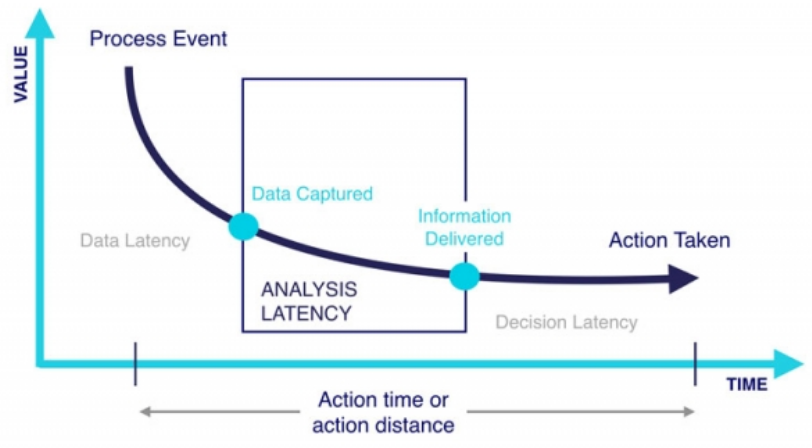

Here’s a great visual illustrating my point:

The graph shows the way the value of something changes over time.

Without predictive analysis software, the gap in the analysis latency section is much larger. The gap is the time between when the data is captured and the information is delivered.

Obviously, this delay will make it more difficult for you to act in a timely manner.

Let’s revisit the customer churn problem. If you don’t get that data delivered right away, by the time you attempt to prevent a customer from churning, you might be too late. They already switched to a competitor.

But that’s not the only application for real-time decision-making.

Predictive analysis algorithms could determine when one of your customers might need a specific product you’re selling.

Let’s say they are going on vacation in two weeks. They need that specific product before they go.

If you wait too long to take an action to try to get that sale, you’ll be too late even if you did everything else right.

You identified their need and sent them a personalized, highly targeted campaign. But if that was not done in a timely fashion, it’s useless.

Create advanced regression models

Some of you might be currently using regression models in your marketing strategy.

Predictive analysis will improve this strategy.

Even if you’re not doing this, you can start to do so once you implement predictive analysis software. Regressions can help you measure and compare different variables.

For example, you could try to determine how social engagement relates to your website traffic. Or you could compare email open rates to conversions. And you can relate your page authority to the source of your leads.

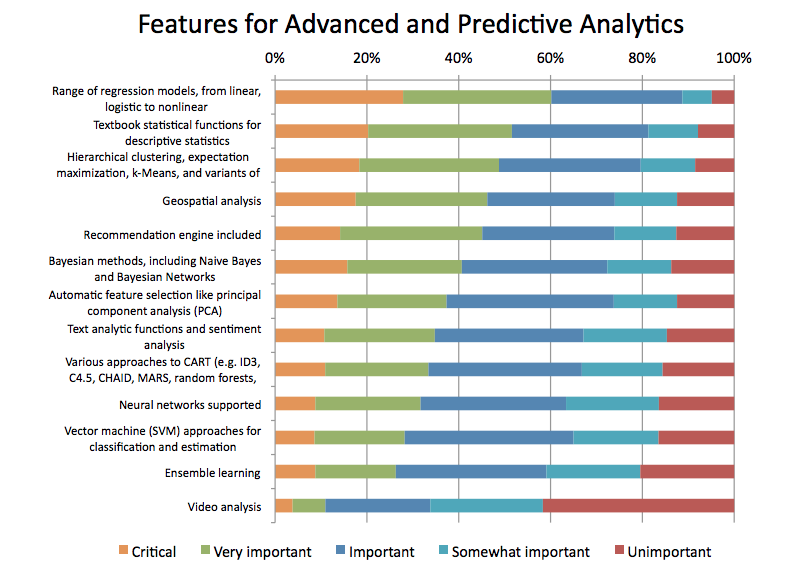

Improving the range of regression models was the most important feature according to a recent survey on the use of predictive analysis:

The information gathered from a regression model can help you validate your marketing campaigns.

You’ll have a much better understanding of what’s working and what needs improvement.

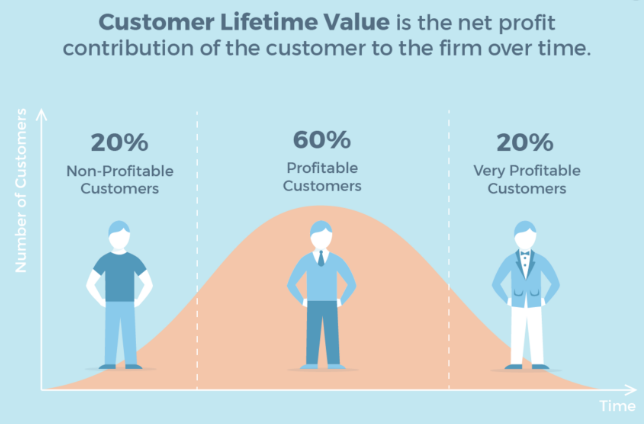

Predict lifetime value (LTV)

In addition to calculating when and if a customer would churn, predictive analysis software can estimate their lifetime value.

Although this value is often overlooked, it’s one of the most important metrics for marketers to track:

Simply put, lifetime value will show you how much a customer is worth over time.

From the very beginning stages of the customer journey, predictive analysis can help identify which customers will be the most profitable.

Segmenting those people accordingly will improve your targeting strategies. Now, you’ll be able to make even more money from your most profitable customers.

Furthermore, LTV will also help you calculate a more accurate ROI of your marketing campaigns.

I see companies make this mistake all the time. They stay away from certain acquisition strategies because they can’t justify the cost.

But that’s because they don’t measure LTV, or at least they’re not doing it accurately.

You need to look beyond the customer’s initial first purchase. Here’s a very simple example.

Let’s say it costs you $50 to acquire a customer based on the campaigns you’re running, but their average purchase is $20. It doesn’t mean you need to abandon those strategies—not if the lifetime value of that customer is $1,000.

Predictive analysis will make these figures much more accurate.

Prioritize qualified leads

You might be getting a ton of leads right now, but not all of them are qualified.

Qualified leads are more likely to convert, and you need to prioritize them.

But if you allow those leads to get lost in the shuffle, you won’t capitalize on them.

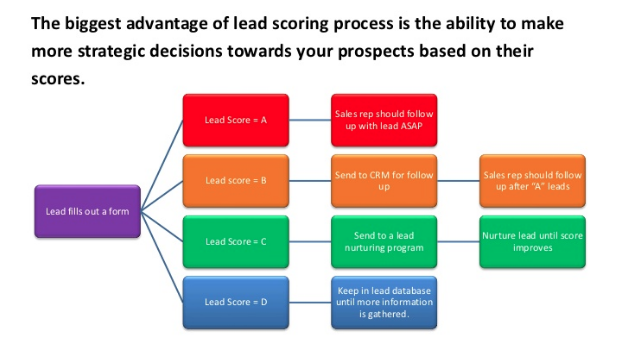

I mentioned lead scoring earlier. Based on your predictive analysis, you can improve your lead scoring system. If you don’t currently have a lead scoring system in place, this will be a great opportunity for you to create one.

Here’s a basic example of what a lead scoring system may look like:

Prospective customers with the highest lead scores get the most attention.

You can even target them with more expensive campaigns and acquisition strategies because they are more likely to convert.

Remember I said not all your customers are the same? Not all your prospects are the same either.

Predictive analysis will take this strategy to new heights.

You’ll get more insight into how to keep these people engaged. You can even learn predictions on their preferred price points and the types of products that will get new leads to convert.

This will help you generate more profits by focusing on your pricing strategy.

By applying predictive analysis to your lead scoring system and qualifying your leads, you will accelerate new leads through the conversion funnel. Ultimately, more conversions translate to more money.

Conclusion

Predictive analysis technology can drastically improve your marketing strategy.

Many businesses haven’t adapted to this yet even though they recognize its importance. This is a great opportunity for you to jump on board now to gain an advantage over your competition.

Your predictive analysis models will help with your customer segmentation strategy.

This software will improve your automation tactics and help you prevent customer churn by identifying it before it’s too late. You’ll also be able to make other important decisions in real time.

Predictive analysis is great for advanced regression models.

Use this technology to help you predict lifetime value of a customer and prioritize qualified leads.

Once you’re ready to start using predictive analysis to improve your marketing strategy, I suggest you apply the concepts I’ve outlined in this guide.

How is your business using predictive analysis to enhance your current marketing strategies?

Source Quick Sprout https://ift.tt/2KeVhr5