If your business relies on subscriptions to generate revenue, you probably offer a free trial to test your product before you ask your subscribers to pay.

This is a great strategy. People may be hesitant to pay for your subscription initially, but if they can try it first, it gives you an opportunity to win them over and turn them into paying customers.

Some of you may even offer free plans for certain services. The idea behind this strategy is that these people will eventually upgrade to paid plans.

But you can’t assume every free trial or free plan user will become a paying customer.

I see this problem all the time in my consulting work.

Businesses don’t have a problem getting people to sign up for free plans and free trials, but when it comes to getting paid, their conversions are lower than expected.

Even you don’t use this business model yet but plan to generate recurring sales by implementing subscriptions, it’s important for you to get this strategy right from the start.

Certain tactics will help you increase the chances of getting these free trial and free plan users to convert.

I’ll explain what you need to know so you can apply these strategies in your business.

Make the transition as easy as possible

The first thing you need to do is analyze your current process. Go through the steps a user needs to take to become a paying customer.

If you’ve got too much friction, unnecessary form fields to fill out, and anything else that slows down the process, it’ll hurt your conversions.

Everything needs to be as smooth and easy as possible for the user.

For example, let’s say the free trial period is over. Now what? Do they need to pick up the phone and call a customer service representative to give their credit card information over the phone?

That’s way too complex.

If you run subscriptions through a mobile app, you can have the user scan their credit card with their camera. This is even easier than typing the numbers.

To make this transition easy for your users, don’t force them to commit to a long-term plan.

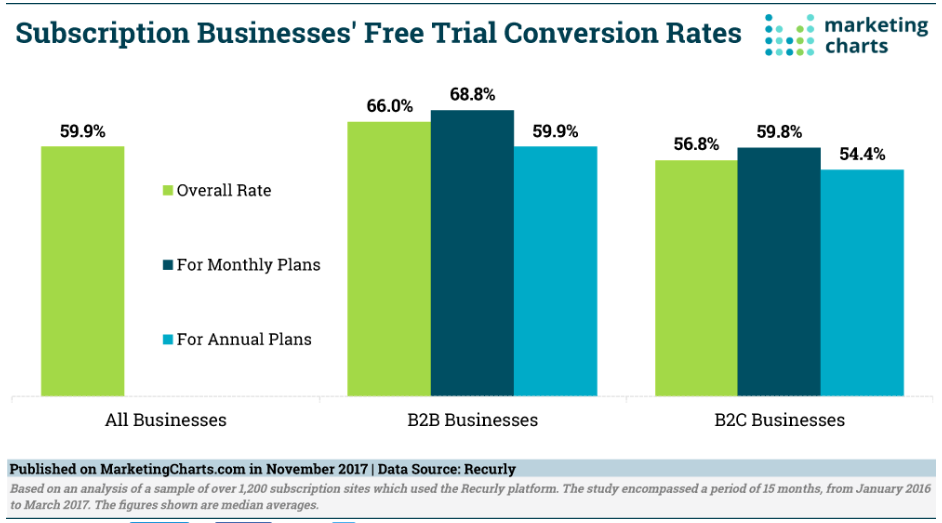

In fact, monthly subscriptions have higher conversion rates from free trials than annual plans do:

If you’re forcing someone to commit to a year, they’ll think much longer and harder about the decision. You don’t want that.

But if they need to pay only for one month at a time with the option to cancel at any moment, it will definitely be an easier decision for them.

I get your thinking behind trying to drive annual plans. But realistically, if your product is good enough, customers will stick with you for long periods even on a monthly plan.

Plus, you’ll likely make more money this way.

You can generate more profits by focusing on your pricing strategy. Customers who commit to a yearly membership or subscription will probably be paying less during that period than those who get billed monthly.

Give users a reason to end their free trials early

Here’s something else I see all too often with subscription businesses. They wait until the trial ends before trying to get users to convert.

By that point, it’s too late.

For example, let’s say you offer a 14-day free trial. Once the trial expires, you give the user some buffer time to decide whether they want to become a paying customer.

A week later, you send an email with a CTA to a paid subscription link.

If this sounds like a strategy you’re currently using, it’s probably why your conversions are so low. Waiting this long is not a good idea. By this point, your service is no longer on the minds of the consumers.

They’ve already gone a week without using it and realized it’s not something they need in their lives.

Instead of waiting until the trial is over, you can give the user an incentive to sign up while their trial is still going on.

But why would anyone want to end their free trial early? You need to make them an offer that’s worth it.

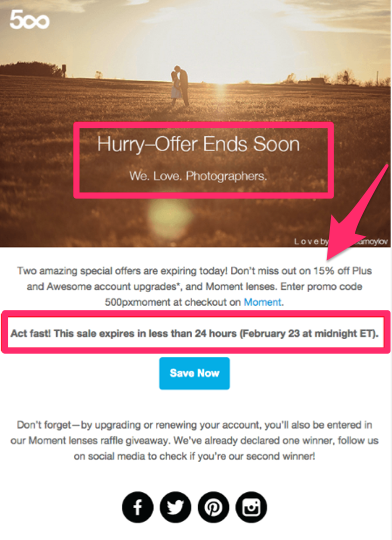

Discounts and other promotions will usually get the job done. Here’s a great example from 500px:

This email uses FOMO—the fear of missing out. You can guide people’s emotions to drive sales with this strategy.

500px is offering 15% off its membership, plus additional account upgrades. However, this promotion won’t last long. As you can see from the highlighted bit, this offer lasted for only 24 hours.

Put yourself in the shoes of the consumer for a minute here. Let’s say they are on day 22 of a 30-day trial.

They like the product and are thinking about upgrading when the trial expires.

But why would they wait and pay the full price when they can get 15% off today? This type of offer gives them a reason to end their trial early and convert.

You want to target these users while they’re still hooked and your brand is fresh in their minds. If you give them an incentive to end the trial early, you’ll increase the chances of them becoming a paying customer.

Offer trial extensions

What happens if a user doesn’t take the bait of the incentive to end their trial early?

Does that mean you should give up on trying to get them to convert? Absolutely not.

Some people may need a bit more time to determine whether they want to use your product. Here’s what I mean.

Let’s say someone signs up for a free trial. The process was simple and hassle-free, so they completed this action without thinking twice about it.

But because of their circumstances, they didn’t get a chance to explore your product in full.

There are a number of different reasons for this. It’s possible they were busy at work, had a medical issue, were traveling, or simply forgot about the trial.

The reason why they need more time isn’t important. What is important is giving them the option to extend their trial.

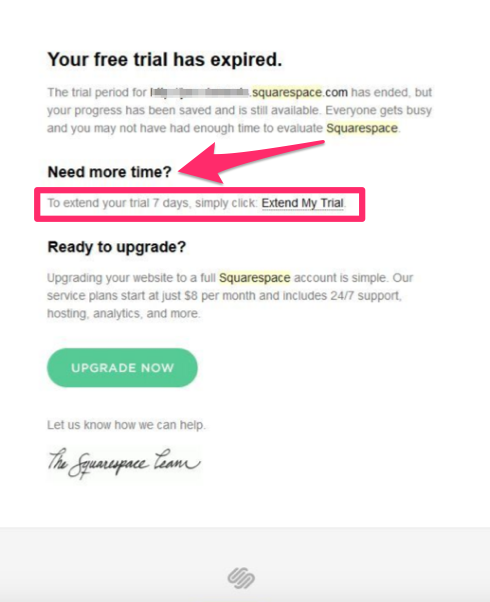

Here’s an example from Squarespace:

Squarespace offers a 14-day free trial to anyone. But the team is willing to work with people who need more time to try its software.

As you can see from the email above, it’s easy for users to add a seven-day extension to their two-week trial.

This is a great way to get users who are on the fence to convert.

I know what some of you are thinking. You don’t want to lower the value of your product by giving it away for longer than necessary.

That’s the wrong mentality. The cost of an extra free week or two is well worth it if you can have this customer for years to come.

It’s bad business to let a prospective customer walk away because you’re unwilling to go the extra mile to acquire them. In this case, these users are already interested in your brand.

They’ve taken the steps to sign up, download your app, or start the process. It’s easier to turn them into paying customers than trying to market to someone else from scratch.

Furthermore, take another look at the email above from Squarespace.

To extend the trial, all the user needs to do is click on the link sent to them, making it super easy—one of the factors to aid conversions I discussed above.

If the user had to send an email or call a customer service representative to extend the trial, they would be less inclined to do so.

Run personalized promotions for the lowest tier plan users

Depending on the type of business you have, you may offer a free version of your product.

This version is free for anyone to use for an unlimited amount of time. Obviously, this is different from a free trial, which has an expiration date.

You should be coming up with marketing campaigns specifically designed to get these freemium users to convert.

Again, as in my last point, these people are already familiar with your product and use it on a regular basis. You need to ease their transition from a free membership to a paid service.

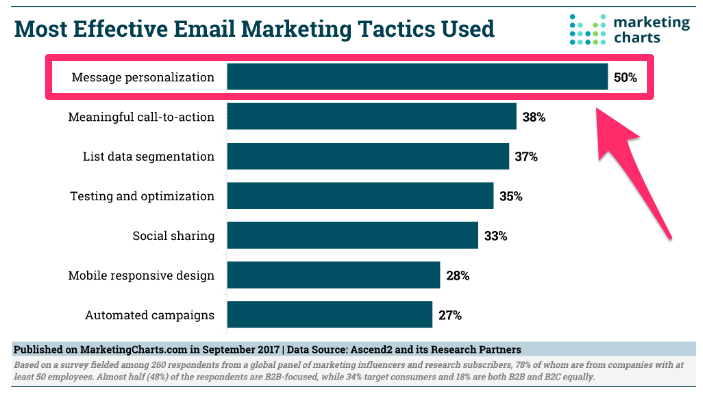

The best way to do this is with personalized content:

Personalizing email messages is the most effective tactic used by marketers. Take that into consideration when targeting freemium users.

Send them a personalized email about the type of content they’re currently consuming free.

Then, give them an incentive to convert.

Just because someone is using your lowest tier membership free doesn’t mean you can’t offer them a free trial of a premium membership. Let them see what features and benefits your other options have.

Once they try these upgrades, it may be difficult for them to go back to the freemium version now that they know what they’re missing out on.

Encourage inactive users to use your product

If you haven’t realized it yet, there is a pattern here with these strategies.

It’s much easier for you to market your paid subscription to people already familiar with your brand, products, services, and software. That’s because there is no learning curve.

You don’t have to explain yourself to people who have used your services in the past.

This holds true for people who used a free trial that expired or had a free membership plan they haven’t been taking advantage of lately. Don’t let that user churn.

Send them an email giving them an incentive to use your service again.

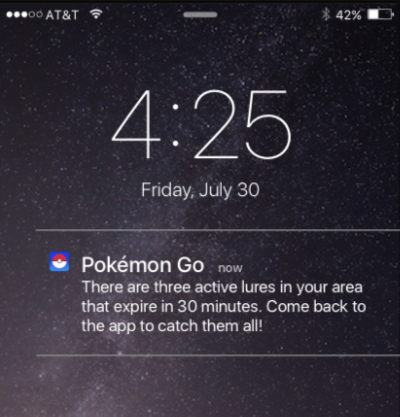

If you have a mobile app, send a push notification to their device. Here’s a great example of how Pokemon Go used this strategy to bring an old user back to life:

As you can see, they are enticing this user with a gameplay incentive to come back to the app.

If the user opens the app within the next 30 minutes, they’ll have access to three active lures. Pokemon characters are drawn to these lures, making it easier to catch them.

If any inactive user stopped playing this game because they were struggling to catch more characters, this type of push notification can bring them back.

Contact customers with failed payments

Your business is likely on your mind 24 hours a day, 365 days a year. But that’s not the case for your customers.

The reality is they have other things to worry about.

If their credit card gets lost or stolen or expires, they may not think to update their payment information for their membership with your company.

In some cases, that card may be tied to their utilities, health insurance, car payments, or other recurring charges that will take priority over whatever you’re offering.

That said, you don’t want to do nothing. The user may never update their payment information unless you contact them.

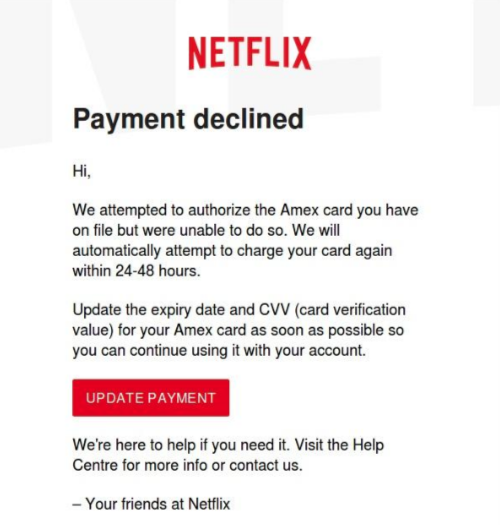

Rather than losing a customer, send automated emails whenever a payment gets declined. It’s easy!

Just look at this example from Netflix:

It’s as simple as that.

By providing a CTA in the email that directs the user to a landing page where they can update their payment information, you will reduce friction in the process.

Without contacting these customers, you run the risk of them going back to the free plan or stopping using your service altogether.

Nurture free trial users with email campaigns

Email marketing is an effective way to communicate with your customers.

If you learn how to create an actionable drip campaign, you can target free trial users and entice them to convert.

This smooth process will help move the customer through the conversion funnel. It all starts with a welcome email.

Research shows that 75% of users expect to receive a welcome email after signing up for something. Give your prospective customers what they expect.

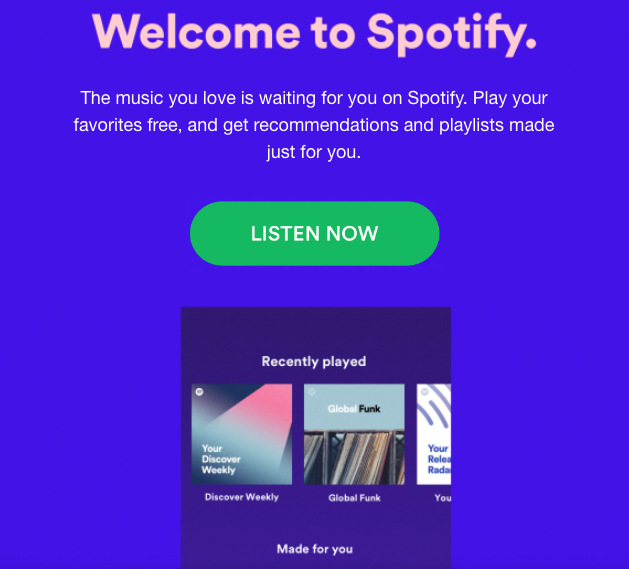

Here’s an example of how Spotify uses this strategy:

As you can see from this message, Spotify is simply confirming that the user has signed up for the service.

There is no pitch for them to upgrade to a paid plan. The message explains the user can play their favorite music free and get personalized recommendations.

Start slow.

Remember, the user just signed up for a free trial or free plan. They’re probably not willing to upgrade their membership within the first hour.

But that doesn’t mean you can’t start to nurture them with an email drip campaign. The subsequent emails will encourage them to upgrade down the road.

Conclusion

Free trials and free plans are both great ways for subscription-based businesses to get as many users as possible to try their products.

But ultimately, those users are useless if they don’t become paying customers.

Rather than focusing your marketing efforts on a new audience, you should be coming up with ways to get the free trial and free plan users to convert.

Make sure the transition process is easy for the user. If they have to jump through hoops to become a paying customer, your conversion rates will be low.

Give them an incentive to end their trials early. On the flip side, if they need more time to test your product, offer a trial extension.

Target your lowest tier membership and inactive users with personalized campaigns.

Don’t forget to contact your current customers when their payment methods don’t work anymore.

Leverage your email marketing strategy to nurture leads and free trial users. If you follow the tips I’ve outlined in this guide, you’ll have a much easier time getting free trial and free plan users to convert.

How are you encouraging free trial and free plan users to upgrade to paid memberships?

Source Quick Sprout https://ift.tt/2FnRWqY

for

for