HARRISBURG (AP) — The Pennsylvania House of Representatives rushed Wednesday night toward a vote on sprawling gambling legislation unveiled just hours earlier to expand casino-style gambling to the internet, airports, bars and elsewhere.The bill was marshaled by Republican majority leaders toward the floor vote, a last-ditch move to raise hundreds of millions of dollars from taxes and license fees to help prop up, if temporarily, Pennsylvania's deficit-riddled finances. The [...]

Source Business - poconorecord.com http://ift.tt/2s5RTbx

الأربعاء، 7 يونيو 2017

7 Tips and Tricks for Finding Great Running Shoes at Discounted Prices

Ah, running.

You either love it or you hate it — or you love it and you hate it. (Or you refuse to run and you love to hate it, if you’re here for that.)

But whether you’re the passionate, endorphin-fueled marathoner, the “ugh, fine, I’ll run the family 5k at Thanksgiving” curmudgeon or the “lay down in someone’s yard half a mile into your route” type, there’s a reason we do it.

The thing is, running is one of the cheapest forms of exercise you can do — no pricy gym membership needed!

Just you, the great outdoors and — really expensive running shoes.

*Cue the sad trombone*

OK, so the actual act of running is free. But the gear that goes along with it can get really expensive, really quickly — especially if you’re serious about running (and about your general health and safety, but we’ll get to that in a minute).

For beginning and casual runners, it’s easy to skip the $500 GPS wristwatch and the $89 high-tech, engineered performance leggings in favor of the free run-tracking phone app and the $8 sale rack running shorts.

But, one thing that all runners — of all ages and at all levels — need to invest in is a good pair of running shoes.

So, in honor of Global Running Day, I talked to one of our editors (and six-time marathoner and triathlete), Caitlin Constantine (that’s her crushing it in the photos here), to get the inside scoop on how to score running shoes at a reasonable price.

But First…

Before she would share her awesome, expert tips with me, Constantine asked me to pass on a word of caution to anyone shopping for running shoes:

“If you are looking at getting running shoes for the first time, I recommend going to a specialty running shop and working with the staff to find shoes that will work for your needs, then buying your shoes from that store,” Constantine said. “Consider the full cost of the shoes as payment for services rendered when finding shoes that will work for you.

“Once you’ve been able to use their expertise to identify the type of shoes that work for you — whether that’s a stability shoe or a neutral shoe or one with more or less cushioning — then you’ll be better equipped to find running shoes that work for you without paying full price.”

Got that?

Good.

Now we can move on to the list of tips, tricks and hacks we’ve compiled!

(OK, just kidding, one more time: If you’re thinking about skipping out on Constantine’s advice — don’t. I’ve been fitted, and it actually meant the difference between loathing running and actually enjoying it. But to this day, I deal with injuries sustained from running with the wrong footwear for too long because a younger me thought one particular trendy brand was ~cooler~ than the rest. Painful lesson learned.)

7 Tips for Finding Good, Cheap Running Shoes

I would say without further ado, but we’ve had a lot of ado here — so let’s dive right in.

1. Know When to Shop

The best months out of year to find deals on running shoes (and most athletic gear, really) are January and April.

In January, stores take advantage of the fact that everyone has really good intentions for the year and offer pretty good sales to draw people in.

In April, people are getting restless after being cooped up all winter and are ready to get outside; they want to do it in fresh gear and bright colors, prompting them to hit the stores again in droves — which makes the stores compete for their attention with deep discounts.

2. Shop the Right Stores

Two places I always check first when I’m shopping for running shoes: department stores and outlet malls.

Department stores like to move product quickly, so they often discount the slow-sellers (such as running shoes) during those monthly and have semi-annual sales they’re always advertising.

Outlet malls are sometimes thought to be, well, a little less than upfront about pricing and quality when it comes to high-end luxury brands. But with most shoe stores and athletic brands, the savings are real because they’re just trying to get rid of last year’s models.

Sports- and adventure-gear stores will also regularly have sales on running shoes, so be sure to pop in once in awhile to check them out. (Just be sure to put on your blinders while you’re walking past the workout clothes — you’re here for shoes, remember?)

3. Take Your Search Online

This method only works if you’ve done the fitting process that Constantine talked us through earlier — you have to know what brand and style works for you and which features to look for. (Pop quiz! Do you know if you need a neutral shoe or a stability shoe? No? Get fitted.)

Athletic- and outdoor-gear sites such as Active GearUp and The Clymb offer deep discounts on running shoes. Just be sure to sign up for their email newsletters so you’re the first to know about big sales and new products. You’ll also score some great coupons this way!

4. Sign Up for Email Lists

Speaking of signing up for emails, be sure to sign up for the email lists for shoe brands that you like, too. You’ll be notified of any sales and the arrival of new models (meaning older products will soon be discounted).

5. Look for Last Year’s Models

Wherever your search takes you, always keep an eye out for last year’s models. You can usually find these in the sale and clearance sections, either in-store or online. Constantine has found good running shoes for as little as $60 to $70 this way.

And sure, last year’s models won’t have the latest, greatest technology — but I promise, up-to-date shoe technology will not make or break a beginning runner’s game.

6. Check Out the Expos

If your city ever holds a major race (like a marathon or high-profile triathlon), go to the expo. Running stores often set up shop at these events, and it can be a great opportunity to score some running shoes at special expo prices.

7. Find Your Local Running Shop

You should have already located your local running shop (for that fitting, remember?), but don’t forget to go back to shop the sales (and support a local business)!

Most local shops even have an email list that you can sign up for as well, so you’ll be the first to know about coupons and sales.

On Your Mark, Get Set, GO

Now that you’ve been fitted for and invested in an initial pair of running shoes with the proper support for your your particular feet which are attached to your particular legs which connect to your particular body, you’ll be able to shop the sales and find the best deals.

It might take a little time, but eventually you’ll be bragging to your running buddies on your 10-miler about how much money you saved on your new running shoes.

Grace Schweizer is a junior writer at The Penny Hoarder.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2sUIBM2

Not Everyone Wants to Own a Home. Here’s What to Know About Renting One

A lot of people look forward to owning their own home and consider it a rite of passage into adulthood (well, maybe not millennials so much).

Even after you’ve considered home ownership from every angle, asked yourself some important questions and weighed the pros and cons, you still might want to hold off on snapping up your dream home.

Housing prices have gotten so out of hand in most parts of the country that many people are better off just renting.

What’s the Deal with Home Ownership?

Home ownership used to be a no-brainer. Adjusting for inflation, home prices were about 33% lower 40 years ago than they are today.

Meanwhile, rental prices are staying steady.

From 2013 to 2017 the national median rent only went up about $200, according to data from Trulia. From 2016 to 2017, it actually dipped about $60.

“While it’s still a better deal to buy, the economic benefit has narrowed to the point that in some places, for some households, the decision to rent or buy a home may be too close to call,” said Trulia economist Cheryl Young.

Recommendations for Renting a House

To find out which option is better for you, run some numbers through a couple of online calculators specifically designed to help you determine if you should buy or rent.

The calculators at Realtor.com and Bankrate are a good place to start.

If it turns out that renting is the direction you want to go, there are some things to keep in mind before you start packing your stuff.

- It may be difficult to rent an apartment if you have bad credit, but there are a few things you can do to up the chances of getting the place you want.

- Make a list of all the questions you should ask a potential landlord. If you aren’t sure what to ask, we’ve got you covered.

- Keep in mind that pretty much everything is negotiable, including your rent. “Lease negotiations are most successful towards the end of the month and during winter when landlords are more desperate for tenants,” recommends Apartment List.

- Before you sign anything or hand over a single dime toward a deposit, make sure you read the lease. You’ll want to make absolutely sure what you’re getting into before you commit to a rental because breaking a lease is a huge headache.

If you can’t afford to buy a home right now or just don’t want to, there’s no shame in your rental game.

There’s a lot to love about renting a place to call home, especially being able to make maintenance and upkeep the landlord’s responsibility.

That leaves you a lot more time for side gigs, beer and pizza (but not all at once).

Lisa McGreevy is a staff writer at The Penny Hoarder. She doesn’t mind be a homeowner but loved renting so mowing the lawn was someone else’s problem.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2r7jV1B

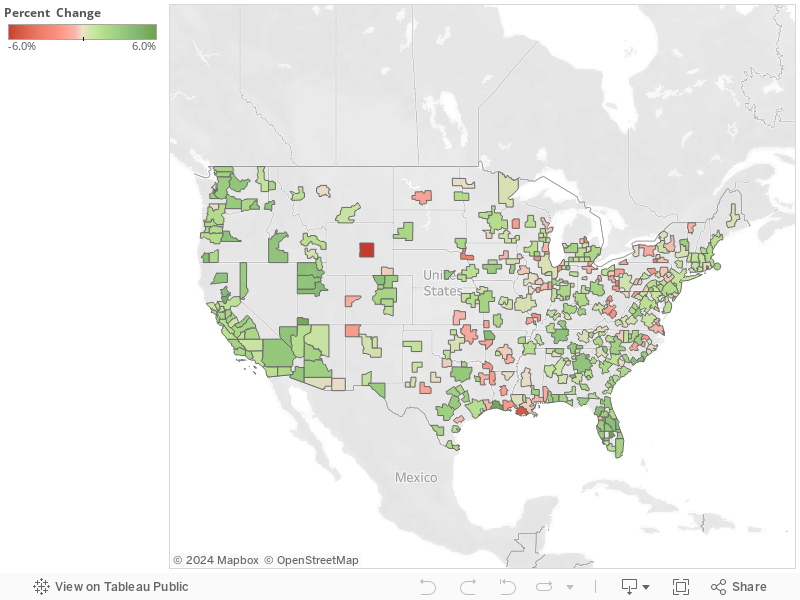

The 10 U.S. Cities That Saw the Most — and Least — Job Growth Last Year

The U.S. economy is in flux when it comes to jobs.

Despite a disappointing jobs report released by the U.S. Bureau of Labor Statistics last week, the national unemployment rate is at the lowest it’s been in more than a decade.

And, according to numbers the Bureau released Monday, 297 of the 387 metro areas in the country had positive job growth over the last year as of the end of April. Good news, right?

But as in most aspects of life, there are winners and losers. The Penny Hoarder looked at the percentage change in new jobs — or lost jobs — to assemble these lists of the triumphs and flops in the latest employment statistics.

The Jobs Report Winners Circle

Sebring, Florida

It may be small, but it sure is mighty — at least when it comes to job growth.

Sebring, a town near Orlando, Florida, topped the list with 5.8% more jobs in April than the same time in 2016. Fifteen hundred more people found employment there in the last year.

Here’s the rest of the top 10, and how much their job market grew since 2016.

- Lake Charles, Louisiana; 5.4%

- St. George, Utah; 5.2%

- Yuba City, California; 5%

- The Villages, Florida; 4.4%

- Provo, Utah; 4%

- New Bedford, Massachusetts; 4%

- Grants Pass, Oregon; 4%

- Auburn, Alabama; 4%

- Gainesville, Florida; 3.9%

Jobs Report Stragglers

These metros were not so lucky over the last 12 months. These regions are spread across the entire U.S., from Alaska to New York.

Casper, Wyoming

Nicknamed Oil City, Casper, Wyoming clearly wasn’t booming over the last year. With the loss of 2,400 jobs — a 6.1% tumble — it came in dead last in employment growth from April 2016 to the same month this year. In fact, since February 2015, the city has shed 6,400 workers.

And here’s the rest of the not-so-lucky regions in the latest report, and the percentage of job decline each saw:

- Houma-Thibodaux, Louisiana; 4.9%

- Sioux City, Iowa; 2.9%

- Weirton-Steubenville, West Virginia; 2.6%

- Anchorage Alaska; 2.4%

- Elmira, New York; 2.4%

- Rockford, Illinois; 2.3%

- Bay City, Michigan; 2.2%

- Carbondale-Marion, Illinois; 2.2%

- Michigan City-La Porte, Indiana; 1.9%

Of course, if you happen to live in one of the bottom 10 areas, or any of the cities that lost jobs over the last year, you’ve come to the right place for advice. The Penny Hoarder Jobs page on Facebook has a bunch of information on careers, along with posts about flexible work-from-home jobs that are available right now.

I mean, where else could you find out how to become an extra in the next Avengers movie, “Avengers: Infinity War”?

Not a comic book fan? While that’s a shame, affordable grocery store darling Aldi is hosting hiring events across the U.S. in anticipation of opening 400 new stores and expanding and remodeling another 1,400.

And we didn’t forget about you teens. The state of your local economy won’t have too much of an effect on the availability of these 100 awesome summer jobs.

As Rihanna would say: “Work, work, work, work, work, work.”

Alex Mahadevan is a Data Journalist at The Penny Hoarder.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2r2Heyk

4 Steps That Will Help Any Millennial Get Control of Their Financial Health

An email arrives. It’s your latest electric bill.

Your phone dings. Your checking account has hit the low-balance threshold you set an alert for.

You glance at the calendar. What day did you mail your rent check?

Managing your finances isn’t a matter of checking the mail after work and opening bills at the kitchen table. It’s easier than ever to keep tabs on your money online, all day, every day.

And that convenience? Well, it can distract you from doing your job.

A new report from Bank of America Merrill Lynch indicates that millennials are significantly more stressed about money than their older colleagues, and they’re bringing that stress to work with them.

Sound familiar?

Everyone You Work With is Stressed About Money

“Employees who are overwhelmed and feeling financially stressed are bringing their worries to work and spending significant time dealing with personal financial matters ‘on the clock,’” the Bank of America Merrill Lynch report explained.

Its survey consulted more than 1,200 employees from around the country last fall. It found that 21% of respondents reported spending five or more working hours each week on personal financial matters, while 22% reported spending three to five hours each week fretting about their finances.

If you consider, as this report did, that an employee spends a median of two hours per week on their personal finances at work, that adds up to 100 hours per person per year.

Millennials: Generation of Worrywarts

Millennials in particular are feeling their financial issues between 9 and 5.

They spend an average of four hours per week on their personal finance issues at work, while Gen X spends an average of two hours on similar tasks. Baby boomers only spend an average one hour per week on personal finance matters, according to the survey.

The survey found that 56% of respondents reported they’re stressed about their financial situation, and 53% of those employees said their stress impacts how well they can focus and be productive at work.

Millennials? They’re twice as likely as boomers to say that stress interferes with their work. That’s probably because we all graduated college during the latest recession with mountains of high-interest student debt, and we’ll never get a leg up on the ruined housing market. Wait, this post isn’t about me?

What to Do if You’re a Financially Stressed Working Millennial

I’m not even going to try to reassure you, fellow millennial type, that you don’t need to worry about your finances all day. But you can make it easier on yourself.

Do a quick check through these four tasks to start breathing a little easier about your finances:

1. Automate Everything

No need for a calendar reminder to move money to your savings account or transfer money to your retirement account. Automate any and all money transfers you anticipate making on a monthly or weekly basis.

Need help keeping your growing nest egg separate from your spending money? Set up an account with an online bank like Chime. It’ll automatically move a portion of each paycheck to make saving a habit, not a chore.

You can also use Chime to choose to round up purchases to the next dollar, so the differences goes into your savings. Chime rewards you with a 10% bonus on round-ups each week.

That’s one to-do off your list just about forever.

2. Get a Handle on Your Student Loans

Your relationship with any student debt you have? Well, it should be pretty intimate. Get to know your student loan servicer, your payment terms and your options for income-based repayment.

If you can automate your payments each month, do it. Otherwise, set a monthly money date (maybe after 5 p.m… hmm?) to get cozy with your student loans.

Don’t worry about how big the tab is. Focus on avoiding student debt surprises.

3. If You’re in a Relationship, Talk About Money

Your relationship with money can get a lot more complicated when you have to manage expenses with a significant other.

Think managing your cash together is a task saved for marriage? Not necessarily. If you’re living together — or thinking about moving in — start talking about each of your money management styles and figure out how to manage your joint household.

If you’re living single and moved back in with your parents to save money, you should talk about money management with them, too. If you’re living at home, you’ll probably have to contribute in some way.

4. Start Investing

Retiring at the stroke of 62? It’s not a guarantee anymore. It’s up to you to invest in your future, so get started with an investment app like Stash.

You can start with just $5 and set up an automatic withdrawal from your checking account each week or month — again, hooray for automating everything!

Choose from more than 30 investment funds organized by your interests or beliefs instead of picking and choosing on some complicated investing site. It costs just $1 per month for accounts under $5,000.

Plus, if you sign up through this link, you’ll get a bonus $5 to invest.

Disclosure: This post contains affiliate links. May we all be a bit richer today.

Lisa Rowan is a writer and producer at The Penny Hoarder. She is a reluctant millennial.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2s4tYta

USDA Seems Totally Cool With This Synthetic Additive in Your ‘Organic’ Milk

You’ve probably seen the big black letters emblazoned on a gold banner on the red cartons of Horizon organic milk: “DHA OMEGA-3 Supports Brain Health.”

I don’t know about you, but I’m all about having healthier brain cells. So when the special milk costs about 30 cents more than the regular organic milk — which is already double the cost of non-organic milk in some cases — I understand.

And clearly, so do most of you. Horizon’s organic milk with DHA raked in about $250 million in sales, which accounts for 14% of all organic milk sold, according to The Washington Post.

But have you ever thought about why this milk is so much better for your brain than the average half-gallon of organic milk?

Maybe you were under the impression that a certain subset of Horizon’s organic farmers were using some special technique to do this naturally. Or maybe you accepted that there were additives but assumed that those additives were also organic.

Either way, you would be wrong.

USDA: Non-Organic Additives Just Fine in ‘Organic’ Milk

That additive that makes your brain so healthy is a synthetic oil with a faintly fishy taste. It’s brewed in huge industrial steel vats that stand five stories tall from an algae called Schizochytrium, which is found along the coast of Southern California.

According to The Washington Post, the U.S. Department of Agriculture isn’t doing much to stop Horizon and other companies from slapping its “USDA Organic” seal on their products despite using the factory-brewed oil, and it’s been that way for at least a decade.

Of course, while Horizon is likely happy about this, consumer advocates on the other side of the spectrum believe a product that contains synthetic ingredients should not be labeled organic.

“We do not think that [the oil] belongs in organic foods,” Charlotte Vallaeys, senior policy analyst at Consumer Reports, told The Washington Post. “When an organic milk carton says it has higher levels of beneficial nutrients, like omega-3 fats, consumers want that to be the result of good farming practices … not from additives made in a factory.”

This a huge debate because the “USDA Organic” seal tends to bring with it a pretty significant bump in pricing as well.

For now, the USDA seems to be siding with the companies, not the consumer groups, when it comes to defining what is and is not organic. That means it will be up to you to decide if the extra cost for organic Horizon milk — and other organic products — is really worth it.

Desiree Stennett (@desi_stennett) is a staff writer at The Penny Hoarder. She is beginning to question whether organic food is worth the extra cost.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2sTePqU

39 Things Every Sales Email Needs to Have

Did you know Gmail alone has more than one billion monthly active users?

That means roughly one in every seven humans on the planet has a Gmail account.

And that’s what I love so much about email marketing: the fact that it’s so universal and allows you to reach such a huge audience.

Just think about it. Not everyone uses Instagram. Not everyone uses Snapchat.

But almost everyone uses email.

I look at email as the great equalizer in marketing. It’s especially helpful if you need to reach an older demographic of baby boomers and beyond.

Of course, there’s a lot that goes into a well run email marketing campaign.

Not only must you get recipients to open your sales email, but you also need to drive conversions.

To accomplish this, you’ve got to cover all the bases.

Here are 39 things every sales email needs to have.

1. A definitive purpose

Before you do anything, you need to have a clear understanding of the specific purpose behind each and every email.

One may promote a new product; another may discuss a major update to your service…

This will dictate the direction you take, the content you feature, the CTA you include, and so on.

Make sure you always know the precise purpose of your message before getting in too deep.

2. Specialized targeting

It’s likely your brand has multiple audience personas.

Effective segmentation is critical for getting the right marketing material in front of each email subscriber.

I recommend creating at least a few different personas and sending out individualized emails based on each group’s needs and preferences.

Here’s a very basic example:

This should ensure no one receives irrelevant content, which should have a noticeable impact on your open rate and conversions.

In fact, “segmented email campaigns have an open rate that is 14.32% higher than [that of] non-segmented campaigns.”

3. A killer subject line

Almost 75% of people don’t open emails.

A big reason for that is lackluster subject lines.

They’re not inspiring enough to motivate subscribers to open the email.

This is why you need to understand the psychology behind a killer subject line.

As a huge proponent of email marketing, I’ve done a considerable amount of experimenting with this process.

Check out this post I wrote on NeilPatel.com to learn the fundamentals of creating better email subject lines.

4. A personalized message

Research from Aberdeen found that “personalized email messages improve click-through rates by an average of 14% and conversions by 10%.”

Other studies have seen a similar trend:

So it’s really important you personalize each email.

Ideally, use each recipient’s first and last name.

5. To be brief

I love long-form content.

Aferall, it’s long-form content that tends to rank the highest in SERPs.

But a sales email isn’t the place for it.

Keep it short, sweet, and to the point for maximum impact.

6. A natural voice

I would wager that the majority of email subscribers don’t want to be addressed in some hyper-corporate, formal fashion.

Instead, most prefer to be spoken to like an actual person.

Use a conversational tone, and approach it as if you’re speaking to your blog readers.

7. Power words

Studies in psychology have shown that people respond better to some words than others.

Utilizing power words is a simple way to connect with readers and pique their interest.

Check out this list from SmartBlogger for examples of power words.

8. The word “you”

At the end of the day, we all want to know what’s in it for us.

If you want someone to read through your email in its entirety, you’d better darn sure appeal to them on a personal basis.

One of the easiest ways to do this is to use “you” when addressing your readers.

“You” is one of the most persuasive words in the English language and should help you connect with your readers.

9. To ask questions

I find asking questions to be a great way to mimic the feel of a face-to-face conversation.

There’s no need to go overboard, but asking a few key questions is an effective way to create rapport and get readers interested.

10. Empathy

People are interested in buying a product or service for a reason.

They have a problem or pain point they’re seeking a solution for.

Make it clear you understand their struggles and that your goal is to help them find a resolution.

11. Trustworthiness

Any semblance of sketchiness is a recipe of disaster.

Be diligent about establishing your brand as a trusted source.

12. To say “thank you”

I find that simply thanking readers for their time and consideration to buy my product is a perfect way to humanize my emails.

Here’s a great quote from The Harvard Business Review:

Saying “thank you” is a great way to close and shows you genuinely appreciate the fact that someone took the time out of their day to read your email.

13. A personalized product recommendation

Keeping with the theme of personalization, I suggest including a personalized product recommendation whenever it makes sense.

Take into consideration the needs, wants, and overall pain points of each targeted demographic.

Then include a link to a particular product they would be interested in.

14. Educational and/or entertaining content

One of the quickest ways to kill your subscriber’s vibe is to blast them with super salesy content.

Of course, you want to be actively promoting your brand, but it shouldn’t come across as obnoxious.

I suggest focusing on the two E’s:

Educating and Entertaining your audience.

Use these as guides for creating your email, and the rest should follow.

15. Eye appeal

Platforms, such as MailChimp and Aweber, offer a boatload of design features to make your emails pop.

Take advantage of these features, and place an emphasis on aesthetics.

This is extremely important for getting readers to browse through your emails and ultimately work their way to your CTA.

16. A branded template

Speaking of visuals, I can’t stress enough how important it is to create your own branded template.

Achieving consistency through this medium is vital for establishing and reinforcing your brand identity.

Once again, most platforms, like MailChimp and Aweber, offer everything you need to create a branded template.

Be sure you’re incorporating your company’s colors, logos, style, etc. so that it sticks with readers and helps them distinguish you from competitors.

17. Standard font

One mistake I see email marketers make is getting too cute with their designs.

More specifically, they get a little crazy with their fonts, making the content difficult to read.

Keep it simple, and stick with tried and true fonts, like Arial and Calibri.

These are easy on readers’ eyes and encourage them to read through the entire email.

18. Font consistency

I also suggest sticking with one font.

Make sure you’re not switching from font to font throughout the body of your email.

This disrupts the flow of your message and can kill conversions.

19. Short paragraphs

White space.

To me (and most readers), it’s a beautiful thing.

One of the easiest ways to maximize the digestibility of your emails is to use short paragraphs.

I recommend shooting for an absolute maximum of four sentences per paragraph.

One to two sentences is even better.

20. Sub-headers

What’s the other key element of digestible content?

Sub-headers to provide breaks and highlight main points.

Never include a large mass of text without breaking it down into individual sections, using sub-headers.

More specifically, it’s smart to use a variety of H1s, H2s, H3s, etc. to prioritize content.

Here’s a good example of how to do this effectively:

21. Bullet lists

Let’s not forget about bullet lists.

They’re ideal for breaking down longer lists into concise and succinct points.

22. Visuals

It’s no secret most people respond overwhelmingly well to visuals.

In 2017, “37% of marketers said visual marketing was the most important form of content for their business, second only to blogging (38%).”

I suggest using at least one image per email to give it some pizzazz and fulfill your reader’s inherent desire for visuals.

Here’s a really nice example of an email from United By Blue:

It’s actually the same image they use on their opt-in page, but it works perfectly.

23. Alt tags for images

In the event an image isn’t properly displayed, you need to have an alt tag for that image.

The alt tag will describe exactly what the image is so there’s no confusion for readers.

24. A video

Okay, you may not necessarily want to use a video in every single email you send.

But they’re definitely an effective way to increase your open rate and click-through rate.

According to Pardot, “Using the word ‘video’ in an email subject line boosts open rates by 19% and click-through rates by 65%.”

This proves people respond favorably to video, and it is something at least worth experimenting with.

25. A clean layout

This should go without saying.

Always be sure to look over each email and eliminate any clutter or unnecessary info that’s not genuinely contributing to its value.

I like to strive for a minimalist feel.

26. An enticing offer

Not only should your offer be relevant to the specific person receiving an email, it should be genuinely enticing.

Ask yourself whether it truly scratches an itch.

If not, tweak it until it hits its mark.

27. Specific benefits

Also be sure to mention the key benefits.

Let readers know exactly how their lives will improve.

28. What they’ll miss out on if they don’t buy

For most humans, “the fear of loss trumps the desire to gain.”

In other words, we’re risk averse by nature.

Briefly touching on the things someone will miss out on by not buying your product or service can provide the extra incentive needed to convert.

Here’s an example:

29. A clear CTA

The CTA is hands down one of the most critical elements of a sales email.

Not only should it be crystal clear which action you want readers to perform, it should be visible.

Netflix crushes it with this email where the readers’ eyeballs instantly gravitate to the red CTA button in the middle of the page:

This one, from Cards Against Humanity, also pulls it off well, incorporating the brand’s signature humor style:

30. Social proof

You’ve probably heard me talk about the importance of social proof in other areas of marketing.

It’s also quite effective in sales emails as well.

Whenever you’re directly promoting a product or service, include a quick little something-something that backs up its legitimacy.

Here’s a great example:

31. A link to your website

You’re obviously going to include a CTA.

But you shouldn’t stop there.

I recommend adding at least one link to your website, but three or four is completely fine.

This is a simple way to increase direct traffic and help people learn more about your brand.

32. A link to your blog

While you’re at it, why not go ahead and link to your blog as well?

It’s an easy way to increase your blog readership and create more buzz around recent posts.

33. Share buttons

Another reason I love email marketing is because it enables you to kill multiple birds with one stone.

Throw in social share buttons to popular networks to increase your following with virtually no extra effort.

34. A forward link

Let’s say a reader loves one of your emails and they want to share it with someone they know.

You can save them time and streamline the process by including a forward link so they can share it with a single click.

This is also a great way to quickly grow the size of your subscriber base without putting in a lot of extra work.

35. Signature

Don’t forget the signature!

This is another way to reinforce your brand identity, and it can drive traffic to other resources you’re trying to promote (e.g., your website).

36. Business info in the footer

People get tons of emails.

Some may literally receive hundreds on any given day.

Be sure to include key business info in the footer (e.g., address, phone number, other contact information) so people know exactly who is sending it and how to contact you if necessary.

It also makes it look more professional and legit in my opinion.

37. An unsubscribe button

Here’s the scenario.

You mistakenly signed up to a newsletter you have zero interest in.

All of a sudden, you’re bombarded with emails and no easy way to stop it.

It’s incredibly annoying and can create feelings of resentment and even hostility toward the brand.

Make sure you’re not doing this to your subscribers.

Give them a clear way to unsubscribe, ideally with only one click.

38. A means of feedback

Say that someone does decide to unsubscribe.

It’s important you know exactly why they decided to do so.

Here’s a good example of the types of questions you can ask to figure this out:

This will provide you with valuable intel so that you can improve your emails moving forward and prevent making the same mistake.

39. Mobile-friendliness

These days, over half (53%) of emails are opened on mobile devices.

Just look at how much email opens on mobile grew between 2010 and 2015:

It’s dramatic!

If your emails aren’t fully optimized for mobile, you’re shooting yourself in the foot.

A mobile-friendly UX is critical, so you should do everything you can to optimize this.

I recommend reading this post from Copyblogger for advice on this topic.

Conclusion

The potential is huge for brands that use email marketing effectively.

Just keep in mind that the average ROI is $44 for every $1 spent.

Not bad!

But to get the most out of your campaign, your sales emails need to hit all the right notes.

By ensuring they have all the elements I covered in this post, you can boost both your open rate and your click-through rate for epic conversions.

What do you think the most important elements of a well-crafted sales email are?

Source Quick Sprout http://ift.tt/2s46rZA

Horoscope: 8 Clever Ways to Make Extra Money With Your Gemini Traits

What do you have in common with Clint Eastwood, Marilyn Monroe, Prince, Venus Williams and JFK?

If your birthday is between May 21 and June 20, it’s that you were born under the sign of the Twins. You’re a Gemini.

People with the zodiac sign Gemini are regarded as independent, flexible and expressive. You’re known as a strong communicator. You’re the life of the party.

These are good traits to have in life — and in Penny Hoarding.

Here are some ways to use your Gemini traits to save money or make some extra cash.

1. Communicative: You’re a Good Talker and Listener

As a Gemini, you’re sociable, expressive and quick-witted. You love to talk. Consider capitalizing on this trait by driving with Uber, the popular ride-sharing app.

Take notes from Naif Bartlett, who has a big personality and earns an extra $300 per week driving with Uber in his college town. He’s even made fast friends with his passengers.

As an Uber contractor, you set your own schedule and work when you want. Your pay is calculated on a base fare, plus time and distance traveled for each pickup. Uber charges a service fee of 20% to 35%, depending on your city.

If you want to give it a try, you must:

- Be at least 21 years old

- Have three years’ driving experience

- Have an in-state driver’s license and a clean driving record

- Be able to pass a criminal background check

Here’s a link to drive with Uber.

2. Impulsive: You’re Not Afraid of Risk

You might welcome risk … a little too much. There’s such a thing as being too spontaneous with your money.

This trait can wreak havoc if you decide to invest in the stock market.

To invest your money without paying someone to make sure you don’t go nuts, try Stash.

This app lets you start investing with as little as $5 for just a $1 monthly fee (but your first month’s free). Stash leaves the complicated stuff out of investing and lets you choose where to put your money based on your beliefs, interests and goals.

If you sign up for Stash here, you’ll get an extra $5 to invest when you open your account.

If you’re looking to make better financial choices, Clarity Money is a free iOS app that helps you see, organize and control all your accounts in one place.

Here’s how it works: You download the app, connect your existing accounts, and get ready to learn more about where your money’s going.

3. Independent: You Set Your Own Course

You may decide you don’t need all the extra stuff cluttering your home and your life. However, you’re also naturally independent — so why not sell it yourself

Without depending on anyone, you can get rid of your clutter with these free apps:

Decluttr: Clear out your old DVDs, Blu-rays, CDs and video games with this app. Scan the barcode with your phone, and Decluttr will make you an offer. It’ll send you a shipping label, so you can ship everything free. Plus, enter PENNY10 at checkout to get an extra 10% for your trade-ins!

Letgo: You can sell nearly anything through this app. Just snap a photo of your item, and set up a listing in about 30 seconds.

Bookscouter: Hoarding old textbooks? Someone will probably pay you for them! Just search the book’s ISBN on Bookscouter, and the site will connect you with more than 25 of the best-paying and most reputable online buyback companies.

4. Energetic: You’re Full of Life

Geminis are known to be energetic. When you set your mind to something, you have enough “go-and-get-it” to achieve your goal.

Did you know you can get paid to get in shape? A company called HealthyWage lets you actually bet on your own weight loss.

Here’s how it works:

- Sign up with HealthyWage.

- Define a goal weight and how much time you’ll give yourself to achieve it. Place a monetary bet on yourself ranging from $20 to $500 a month.

- Meet your goals, and you get paid. Fail, and you lose the money you bet (but it goes toward funding other people’s weight-loss goals.)

5. Clever: You Think Outside the Box

It’s tough to nail your entrepreneurial spirit down to a day job. You like autonomy, and you want to work on something you care about.

But before you say “take this job and shove it,” channel your passion into a side gig.

Use your free morning, evening and/or weekend hours to work part time on your own business. It’s a smart way to earn extra money and a safe way to test the waters of self-employment.

Here are a few simple ways to get started:

Start a bookkeeping business. Want to help other business owners tackle problems and succeed? Read our interview with CPA Ben Robinson, who teaches others to become virtual bookkeepers, and learn how you could earn up to $60 an hour doing this work.

Be a proofreader. If you’ve got a knack for grammar and a good eye for detail, this side gig could easily grow into substantial income. Proofread Anywhere can help you learn the skills you need to become a first-class proofreader, and to get clients and make money.

Deliver food. Sign up with DoorDash to make money helping deliver food to hungry people around your city..

6. Flexible: You Can Adapt to Circumstances

Using a Gemini’s flexibility and adaptability, you can go on secret agent missions.

The survey site QuickThoughts uses your location to send you on top-secret “missions,” and turns your cell phone into private-eye technology.

Was that CVS you just visited clean? How do the lines look at the McDonald’s where you’ve stopped for lunch?

QuickThoughts Missions relies on your input — and sneakily-taken cellphone photography — to give businesses important feedback. And like any respectable secret agent, you get paid for your investigative footwork.

Using your phone’s GPS technology, the app will prompt you for information from places you’ve visited in the past few weeks, as well as places it detects you’re visiting right now.

It also has missions you can accept. For instance, it might prompt you to go to your local Walgreens and snap a photo of the seasonal display. And you’ll earn gift cards for Amazon and iTunes while you’re at it.

7. Persuasive: You Can Bring Others Around to Your Way of Thinking

Use your persuasive Gemini voodoo to try to make the world a better place. There’s no better way to incite political change than to write to members of Congress.

You can actually make money doing this — around $12 to $15 an hour. Before committing to an issue, you’ll be able to brush up on it to see if it aligns with your own views.

Before you start, just make sure you have the appropriate computer gear: a PC running Windows 7 or above, or a Mac running Mavericks or above; a USB headset; and high-speed, wired internet.

8. Objective: You Just Want the Facts, Ma’am

Here’s a fun way to make money harnessing a Gemini’s innate objectivity: Join a mock jury!

Serve as an in-person or online mock juror to help lawyers prepare for real cases. You can earn $10 to $60 for about an hour of your time.

In person, you’ll probably sit through a mini version of a court case, listening to opening and closing arguments from each side. Online, you’ll simply review evidence from one side, including documents, videos and photos.

Like a real juror, once you’ve heard the case, you get to weigh in. In person, you’ll even deliberate with other jurors.

Just remember another Gemini trait is that you’re persuasive.

As a Gemini, you have the gift of gab. You’re an excellent communicator — independent, clever and persuasive.

You have the necessary traits to take control of your career and your life.

All you have to do is harness your sign’s spirit.

Disclosure: We don’t hesitate to pick pennies off the sidewalk when we spot them. But the affiliate links in this post help our earnings grow even quicker. Plus, it’s a lot cleaner than sidewalk money.

Mike Brassfield (mike@thepennyhoarder.com) is a senior writer at The Penny Hoarder. Ladies, he’s a Virgo.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2rB6sT6

10 Smart Ways to Use Leftover Rice (Smart Staple Strategies #1)

For the next few weeks, we’re going to talk about some smart strategies for using leftover staple foods – things like rice, beans, pasta, and so on. Here’s what you do when you cook a bit too much and don’t know what to do with the rest!

Rice is one of those staple foods at our house that shows up in everything. We’ll fill up the rice cooker and use the contents for some arroz con huevos and arroz con pollo … and then we’ll find that we have a ton of leftover rice sitting there in a big storage container. We overestimated how much rice we’d need and now we have a ton left over.

What do we do with it? It’s an absolute waste of time and money to throw out rice, so instead we find some creative uses for it.

Strategy #1: Freeze it in a small container.

This one’s simple. Just measure out the amount of rice you need for a specific recipe that you might make in the future, then freeze that amount of rice in an appropriately labeled container. Let’s say, for example, that we’re going to have etoufee sometime soon, so I’ll dig out our usual etoufee recipe, figure out exactly how much rice will be needed, measure that into a small freezer container or freezer Ziploc bag, label that container, and pop it in the freezer.

Then, the day before or the morning before we’re going to eat that recipe, I’ll just pull the container out of the freezer and pop it in the fridge. It’s thawed by the time we’re going to eat, so then I just need to warm it up a little. It actually rebounds from freezing really well, especially if it wasn’t overcooked to begin with.

Strategy #2: Add it to a soup.

If you’re making almost any kind of soup, just add a cup or so of cooked rice to it near the end of the cooking so that the rice can absorb a little of the flavor and mix in with the soup. We’ll add rice to everything from chili to tortilla soup, from vegetable soups to chicken noodle soups, from lentil soups to broccoli cheese soups. It just bulks up that soup and adds a little flavor.

Quite often, adding a cup or two of cooked rice from the fridge to a pot of soup stretches it from enough soup to feed our family to enough soup to also have a leftover container or two for Sarah and I to use for lunch the following day. In effect, it turns leftover rice into an actual tasty leftover meal. Many of the ideas below function in a similar way – a recipe is expanded by the addition of rice, enabling us to use it as a source for a “leftover lunch,” which is a giant money saver.

Strategy #3: Use it to add bulk to a casserole – or serve as the backbone.

Many casseroles are quite delicious with the addition of a small amount of rice. I’ll add rice to things like our enchilada casserole or even to things that involve pasta sauce without even skipping a beat. Again, that addition just bulks up the recipe almost without notice.

If you have a lot of leftover rice, you can actually use the rice as the backbone for a recipe. One of our favorite family recipes for a very quick and easy meal – often lunch – is the combination of diced cooked chicken and/or mushrooms, cooked broccoli, a cup or two of cheese, and cooked rice in whatever quantities happen to be convenient. It’s delicious and incredibly easy to fix.

Strategy #4: Make rice fritters.

I use something akin to this recipe for the rice fritters, except that I use 2.5 cups of cooked rice rather than the 1 cup uncooked rice that it calls for and I just skip the rice-cooking part and just move right along to making fritters.

This is a great way to turn leftover rice into incredibly tasty finger foods, perfect for a small appetizer or as a side dish for many different meals.

Strategy #5: Or make rice cakes.

Another, very similar strategy for converting rice into finger foods is to make rice cakes with them. All you really have to do is take a bunch of leftover rice – 3 cups works well for the other ingredients here – and season it however you’d like (soy sauce is a good one, but you can use cheese or other things and even use sweet additions), then add a couple of beaten eggs as a binder, add half a teaspoon of oil, mix it up thoroughly, and spread it out until it’s about 3/4″ thick on a piece of parchment paper and cut the mix into three inch squares. Separate the squares a bit, then bake them right on the parchment paper (with a baking sheet under it) in the oven at 350 F for about 10 minutes. Boom – you have square rice cakes.

These make for great after school snacks, and it’s so flexible. You can make savory ones or sweet ones. You can do all kinds of crazy things to it. It’s an easy and convenient snack, too – all you have to do is grab one from the fridge and munch on it. It’s already seasoned and ready to go!

Strategy #6: Make a rice bowl for lunch.

If you have just a cup or so of rice left over, just put it in a bowl and top it with whatever ingredients you have on hand that seem tasty. I’ll often throw whatever leftover vegetables happen to be around on top of it. I might toss on some sauce or some cheese or even some salad dressing – almost anything works. I’ll heat it up when I’ve added everything I want to be hot, and then I might add another cold ingredient or two on top afterwards.

There is no set recipe here – the goal is to flavor that rice into something yummy for a quick lunch. If you’re doing this in the morning before work, you can just put the rice and whatever ingredients you want into a microwave container and take it to work with you. It’s just that flexible.

Strategy #7: Add it to a salad.

If I have half a cup of leftover rice, I’ll add it to almost any kind of salad to change the texture profile of that salad. Yes, anything from a traditional lettuce salad to a chopped salad to a fruit salad. Unseasoned rice is a pretty blank palate upon which you can paint any flavor, and such rice can add bulk to almost anything.

I especially like adding it to salads that contain bits of fruits and nuts bound together by something sweet. Rice seems to disappear into this, only adding a bit of texture and making the salad a bit less over-the-top sweet.

Strategy #8: Make some fried rice.

Take some diced onions and diced green peppers and even a bit of minced garlic. Toss them in a skillet with a bit of oil until it’s sizzling beautifully and the onions have just started to brown. Then, toss in just a bit of water or soy sauce – a teaspoon or two – and follow it with that fully cooked rice, stir it around thoroughly, wait until the rice is hot and coated in the onion and pepper drippings, and serve it.

This stuff is delicious on its own, but it can also be served on the side of lots of different meals. I often eat this kind of simple fried rice as a standalone lunch, to tell the truth, as it’s a great way to use a bit of leftover chopped onion and green pepper (which I always save) and a bit of leftover rice.

Strategy #9: Wrap it in a tortilla.

There are many, many different tortilla-based dishes that are wonderfully accented with plain leftover rice. We’ll take rice and use it as a taco filling or a burrito filling. We’ll add it to our enchilada mix and fill up enchiladas with it. We’ll even use leftover rice in wraps where we’re stuffing a tortilla with lots of vegetables.

Again, rice accentuates everything, so it works well in all of these contexts. My personal favorite is to mix some in with black beans to make a black bean and rice enchilada mix. That’s practically manna from heaven for me.

Strategy #10: Sweeten it and eat it for dessert.

If all else fails, you can use it when you have a sweet tooth. Just put half a cup or so of rice in a bowl, warm it up, and coat it with a teaspoon of sugar and a half-teaspoon of cinnamon. Mix it around and enjoy.

Those two simple additives turn plain leftover rice into a wonderful sweet dessert. You can season it with other flavorings as well, but for me few things beat sugar (or brown sugar) and cinnamon. It’s a great very quick warm sweet treat.

Next time, we’ll look at some slick strategies for using extra beans!

Related Articles:

- The Power of the Spice Rack

- My 10 Favorite Healthy and Inexpensive Foods (and a Recipe for Each)

- Using the $1-Per-Meal Strategy to Save Big on Food Costs

The post 10 Smart Ways to Use Leftover Rice (Smart Staple Strategies #1) appeared first on The Simple Dollar.

Source The Simple Dollar http://ift.tt/2rLZbhW

Do Smartphones Make Us More Impulsive Shoppers – or Less?

When it comes to the way they influence consumer spending, smartphones are double-edged swords. On the one hand, it’s undeniably great to have more computing power in our pockets than the computers used to put the first man on the moon. That power allows us to scan bar codes with our phones, make price comparisons, call our friends to see if we’re getting a good deal before buying something, and even take pictures of items so we can review them later to see if we really want them.

But, smartphones also make it a whole lot easier to buy things on impulse — even when you’re nowhere near a physical store. The mere existence of the Amazon mobile app can be a stumbling block for even the most frugal among us. I would be lying if I said the “Buy it Now” button hadn’t cost me several hundred dollars in regrettable, impulse-driven purchases over the course of my life.

So, which is it? Do phones make us more likely to spend money carelessly — or less? Let’s dig in.

Smartphones Encourage Bad Spending Habits

There’s no denying that smartphones are changing the way we shop. Every year the percentage of online sales via smartphone increases, with holidays seeing particularly strong activity. In 2016, there were $4.61 billion in smartphone purchases from Thanksgiving through Cyber Monday. That’s a whole lot of money to spend in five days.

The obvious reason for the surge in purchases is the convenience that comes with using your phone to shop. There are people who think this lack of friction between the thought I want that and the realization I can buy that right this second can cause serious problems.

They would argue that the supposed convenience of smartphone shopping is a trap. Sure, we can buy things faster, which frees up time for other activities — but faster isn’t always better. Just look at fast-food establishments. They make it easy to get food, but certainly don’t contribute to our health. Mindless shopping, like mindless eating, will cause issues. One notable analyst at a tech research firm thinks that online shopping is “now so embedded in our existence, we don’t even think about the fact that we pulled out our phone and bought things.”

There is evidence to back up the notion that we’re thinking less about what we buy. A survey of over 12,000 shoppers found that 42% of them use their mobile phones to “make frequent purchases on a whim.”

And if those purchases are made on credit, people might be causing themselves to go into debt. Or more accurately, to dig themselves even deeper into debt. The average American adult with a credit card has racked up $5,284 in debt.

Interestingly, consumers are self-aware that the easier it gets to buy things, the more they are likely to spend. Consumers in the U.K. seem especially worried that their phones might encourage them to overspend. A full 38% go so far as to say that they would “like a cap on tap-and-go payments in order to curb their spending.”

Unfortunately for those Brits, such a cap is unlikely to be a main feature of mobile shopping anytime soon. Overall, the trend toward shopping via smartphone shows no signs of slowing down. There are many social media sites, Pinterest chief among them, that are almost perfectly designed to get us to part with our cash on a whim. It feels like we are fighting an uphill battle.

Yet, despite the compelling evidence that our smartphones lead us to spend our money more impulsively, there are still several ways those same devices can help us to become savvier consumers.

How Smartphones Can Save You Money

I was recently helping my little sister get some decorations for her apartment. As we perused the wares at Bed Bath & Beyond, my sister came upon a lamp that she loved. Before she could toss it in her cart, I whipped out my phone and opened up Amazon’s bar code app.

A quick scan revealed that the same lamp could be found at a significantly cheaper price if she made the purchase online. Sure, she’d have to wait a few days, but she was in no rush. She decided to hold off on purchasing the lamp and instead put it on an online wish list. The act of practicing delayed gratification through the use of wishlists is a tried and true ways to reduce impulse buys.

This example shows that smartphones are not necessarily evil little machines that suck money from our bank accounts by overriding our frugal impulses. In fact, used wisely, they can provide a powerful one-two punch: We can use them to search for the the best available price, and as a way of slowing down the purchase process.

The act of slowing down should not be underestimated. Even the small act of taking a deep breath before mindlessly buying something can allow us the space to really consider what we’re doing. We might find that we don’t actually need the thing that, a moment ago, we truly thought we wanted.

Furthermore, despite all the hype about smartphone spending, we are still more likely to make impulse purchases in stores than on a phone — and it’s a wide gap between the two. A 2017 survey found that “68% of U.S. consumers said their primary location for making impulse buys was in person in a store.” If your smartphone shopping habit is keeping you out of a physical store, you may be coming out ahead in terms of total impulse dollars spent.

Even when you do find yourself shopping at a physical store, all hope is not lost. In fact, brick-and-mortar retailers are becoming concerned about consumers who have “mobile blinders” on when they’re in the checkout line. That term refers to our habit of fixating on our phones while we wait in line — which reduces the chance we’ll be seduced by the candy bars, gum, magazines, and other tempting point-of-purchase goodies positioned near the register.

Checkout aisle revenue is a $5.5 billion-a-year business, so you can see why retailers would be concerned about the growing number of people who would rather play “Plants vs. Zombies” on their phones than be enticed by a tabloid magazine. If you’re feeling bad about your Candy Crush addiction, take solace in the fact that it could be saving you money in the long run — as long as you don’t start spending as much money on in-app purchases as you would have on a Snickers bar.

The more interesting version of this scenario is to consider the person who might be standing in line and staring at their phone, but they aren’t playing a game. They’re reading an e-book, or updating their budget on Mint.com, or learning about a new credit card that will earn them a free flight. In those circumstances, they’re not only avoiding temptations, but they’re harnessing the wonders of technology to accomplish things that would have seemed like magic 30 years ago.

Summing Up

There’s no clear answer as to whether smartphones are improving or corroding our spending habits. That being the case, it might be helpful to think of smartphones like any other tool: The degree to which you use a tool properly will determine whether you get the outcome you desire.

For instance, a kitchen knife is a tool. A sharp knife will chop vegetables faster, but it will also do more damage if you cut yourself. If you’re careful and methodical, you’ll be fine. If you’re reckless, you’ll get in trouble.

It comes back to the adage made famous by Spider-Man: “With great power comes great responsibility.” We can ultimately boost our savings rate if we can be mindful about when and how we use our increasingly powerful devices.

Related Articles:

- Time for an Upgrade? Here’s How to Sell (or Recycle) Your Old Phone

- Three Apps for America’s Money-Management Woes

- 11 Strategies to Minimize Shopping or Avoid It Altogether

The post Do Smartphones Make Us More Impulsive Shoppers – or Less? appeared first on The Simple Dollar.

Source The Simple Dollar http://ift.tt/2rULqj0

6 Ways to Keep Your Credit Score Safe When Opening and Closing Credit Cards

You can snag some pretty awesome rewards by taking advantage of credit card signup bonuses. But are the gift cards and travel points really worth it if all that activity on your credit report winds up hurting your credit score?

It doesn’t have to, if you do it wisely. Here’s what you need to know to open and close credit cards without negatively impacting your credit score.

1. How Credit Reporting Agencies Calculate Your Score

To know what affects your credit score and what doesn’t, you need to consider what makes it up. Below are the factors that determine your score and their weight in the scoring process:

- Payment history – Regular on-time payments will boost your score; missed or late payments will lower it. Payment history has the most impact on your score at 35%.

- Debt-to-credit ratio – Also known as your “credit utilization ratio,” this represents how much of your available credit you’ve used. Using up all or most of your available credit will lower your score, while only using a small percentage will raise it. This makes up 30% of your credit score.

- Length of credit history – You also get points for how long your credit accounts have been open and how long since their last activity. The older your accounts, the more responsible you look to potential lenders. This makes up 15% of your credit score.

- Credit inquiries – When you apply for a new card, this counts as a hard credit inquiry or pull. Too many hard pulls in over a period of time can lower your score as it signals you’re trying to obtain too much credit too fast. Soft pulls happen when you (or an employer or landlord) check your credit history. These don’t affect your score because you’re not asking for new credit. The number of recent credit inquiries you’ve had accounts for 15% of your credit score.

- Credit mix – Having a mix of revolving credit (credit cards), retail credit (store-specific cards) and and installment loans (auto loan, mortgage, etc.) works in your favor, as it shows you can be responsible with different types of credit. A good mix is nice, but because it accounts for only 10% of your score, it’s entirely possible to have a good score without it.

Armed with this info, you can better understand whether opening a new card will help or hurt your score. A new card will often have a positive impact on your score because the increased available credit reduces your debt-to-credit ratio, which has the second-largest impact on your score. Just be sure to keep the following guidelines in mind.

2. Pay on Time

Payments made within 30 days of the due date, while technically late, won’t ding your credit score. Once you reach the 30-day-overdue mark, though, the creditor may report the late payment to the credit agencies, which can lower your score. And if you reach the 60- or 90-day-overdue marks, the negative reports will hit your score even harder. The later you are, the more damage it does to your score.

Remember, payment history makes up the largest chunk of your score at 35%. So whatever new cards you open, be sure to stay on top of them when the monthly payments are due.

3. Pay Them Off Each Month (With One Exception)

Paying your balance in full each month keeps your debt-to-credit ratio low, which is good for your credit score. It also keeps you from incurring additional fees that can eat away at any monetary gains of a new card promotion.

That said, you’ll want to make sure you keep making regular small purchases on each card to avoid getting penalized for inactivity. Having a zero balance on all of your cards for an extended period of time can actually bring your score down a few points, as it signals a failure to use your available credit wisely. Charging a small item each month and paying it off the next month shows lenders you can handle your credit and builds a positive track record. As a rule, it’s best to keep your debt-to-credit ratio between 1 and 20% at all times.

4. Keep Your Oldest Account Open

Closing an old account won’t boost your credit score, but it could lower it if it affects the overall length of your credit history or increases your debt-to-credit ratio.

If you have a number of cards and closing one will only affect these two factors by a small percentage, it’s probably safe to close it. That said, there’s generally no good reason to close an old account. Having 10 accounts you’ve paid in full each month for years shows you’re quite good at managing your credit.

5. Become an Authorized User

One trick to maintain a long credit history while opening and closing cards is to have someone list you as an authorized user on their account. Once you’re an authorized user, the account will show on your credit history and impact your score. This keeps your average account age nice and long, even as you open newer, younger accounts.

6. Don’t Open Too Many Cards at Once

In general, each hard pull takes your credit score down 3-5 points. Each inquiry stays on your credit report for two years, though it only affects your credit score for one year. If your score is otherwise high, and a rewards card truly seems worth it to you, it’s your call whether you’re willing to take the short-term points hit.

Keep in mind, opening too many cards at once can be a red flag to creditors, as it looks like you’re scrambling to get your hands on cash. Everything should be all right if you don’t go overboard in any 6- to 12-month period.

Kelly Gurnett is a freelance blogger, writer and editor who runs the blog Cordelia Calls It Quits, where she documents her attempts to rid her life of the things that don’t matter and focus more on the things that do. Follow her on Twitter @CordeliaCallsIt.

This was originally published on The Penny Hoarder, one of the largest personal finance websites. We help millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. In 2016, Inc. 500 ranked The Penny Hoarder as the No. 1 fastest-growing private media company in the U.S.

source The Penny Hoarder http://ift.tt/2sSe7Ky

الاشتراك في:

التعليقات (Atom)