POCONO PINES — Tobyhanna Township as you know it, may soon be a thing of the past.Township officials announced Wednesday afternoon plans to create a massive $350 million development project dubbed Pocono Springs Entertainment Village that they hope will become one of the country’s premier destinations.“We’re announcing a beginning and not an end,” said John J. Jablowski Jr., Tobyhanna Township manager. “This is the beginning of a [...]

Source Business - poconorecord.com https://ift.tt/2JC6Ibs

الأربعاء، 11 أبريل 2018

Understanding the Tax Benefits Of A Mortgage: Homeowners are eligible for several Tax Deductions from Their Mortgage Interest

As the tax filing deadline looms, many Americans continue to prepare and file their annual income taxes. Learn about several different tax deductions homeowners can take advantage of.

Source CBNNews.com https://ift.tt/2qoVlff

Source CBNNews.com https://ift.tt/2qoVlff

This Remote Gig Offers Good Benefits, Including Discounts on Top Brands

Sitel, a provider of outsourced customer service to global companies, is hiring customer service representatives in 25 states.

So what are these sweet benefits, you ask?

Paid training? Check. Medical and dental? You betcha. A 401(k) plan? Yes again!

On top of that, Sitel employees also get discounts from the company’s partners. Some of the big brand names include L’Oreal, Under Armour, Lexus and General Mills. Score!

The positions are available in Alabama, Delaware, Florida, Georgia, Idaho, Illinois, Iowa, Kansas, Kentucky, Louisiana, Maine, Mississippi, Missouri, Nevada, New Jersey, New Mexico, North Carolina, Oklahoma, Pennsylvania, South Carolina, Tennessee, Texas, Utah, Virginia and Wisconsin.

Don’t see your state? Here’s why companies sometimes restrict the location for work-from-home jobs.

As a remote customer service rep for Sitel, you’ll work 31-40 hours per week (pay is not specified), with opportunities to earn incentive-based bonuses.

If customer service jobs aren’t your thing — or you really don’t want discounts on Cheerios — no worries. You can check out our jobs page on Facebook. We’re always posting new, work-from-home opportunities.

Remote Customer Service Representative at Sitel

Pay: Not specified

Responsibilities include:

- Providing stellar customer service to Sitel’s partners

- Navigating multiple systems simultaneously

Applicants for this position must have:

- A high school diploma or equivalent

- Previous customer service and sales experience

- Excellent verbal and listening skills

- A distraction-free home office space

- Ability to work remotely, with good time-management skills

Technical requirements include:

- Desktop or laptop — Mac, Tablets, Winbooks, Smart devices, Windows Mini PCs, Chromebook and Android systems are not compatible

- A separate 19” Monitor with 1280×1024 minimum resolution

- Windows 7, 8 or 10

- Wired keyboard, mouse and USB headset — wireless not allowed

- Wired DSL or broadband high-speed internet — WiFi, WiMax, Satellite, dial-up, and/or Hotspots are not allowed

Benefits include:

- Paid training

- Medical and dental for full-time employees

- 401(k) retirement match

- Vacation and holiday pay

- Incentive opportunities

- Employee discounts with Sitel’s partners

Apply here for the customer service representative job at Sitel. Make sure to choose your home state when applying.

Kaitlyn Blount is a junior staff writer at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder https://ift.tt/2JCdkql

How to Guide People’s Emotions to Drive Sales

Successful marketers know how to go the extra mile when promoting their brands, products, and services.

You need to understand what role psychology plays in the buying process. For example, different color schemes can impact sales on your website.

Those of you who want to take your marketing strategy to the next level need to understand the way your customers think. Use this information to your advantage.

People behave a certain way when specific emotions are triggered. I’m sure you can see this in your life as well.

Have you ever punched a wall or broken something when you’re upset? You wouldn’t normally do that, but you might behave that way as a result of a strong emotional response.

Don’t worry, we won’t to try to get your customers angry or play a game of psychological warfare with them.

Instead, I’m going to show you how you can trigger a variety of emotions with different marketing campaigns. As a result, you’ll be able to drive more sales.

Here’s what you need to know about guiding the emotions of your customers.

Leverage the power of fear

Fear is one of the most powerful emotions, which is why I want to use it to start our discussion. You can use fear as a sale tactic in many different ways.

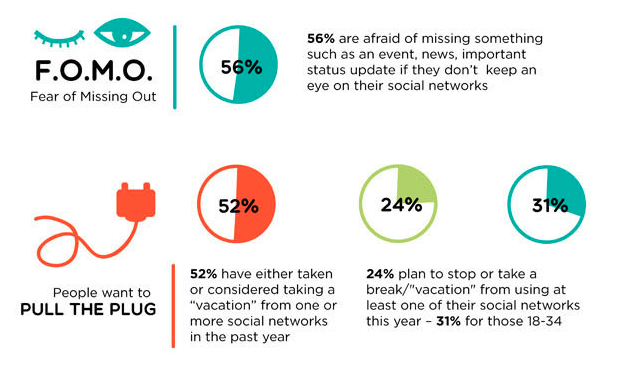

For starters, try to create the fear of missing out on something, better known as FOMO.

In today’s age of social media, people feel FOMO more than ever. Take a look at these statistics from a recent study:

More than half of social media users believe they need to constantly monitor their social profiles because they’re afraid they’ll miss out on something.

It’s becoming such a problem that people recognize the fear is affecting their behaviors. That’s why so many social media users consider taking a break from these platforms.

How can you leverage this emotion from a marketing perspective? Create ads for your website, email campaigns, and social profiles that are time-sensitive.

For example, you could run a flash sale offering 40% off everything on your website for the next six hours. This type of marketing strategy will cause users to act fast for the fear that they’ll miss out on the sale.

They are already interested in your products and have some items in mind they want to purchase. Taking advantage of a flash sale is the perfect time for them to act.

Depending on what kind of products or services you’re offering, there are other ways to create fear in the minds of your customers.

For example, let’s say your company sells home security systems. You could create an advertisement that shows how your products help prevent a burglary or home invasion.

This can create fear in the minds of prospective customers. They may think to themselves that their current security system wouldn’t protect them in the event of an emergency.

Don’t get me wrong, we’re not trying to traumatize your customers here. There are more subtle ways to approach this.

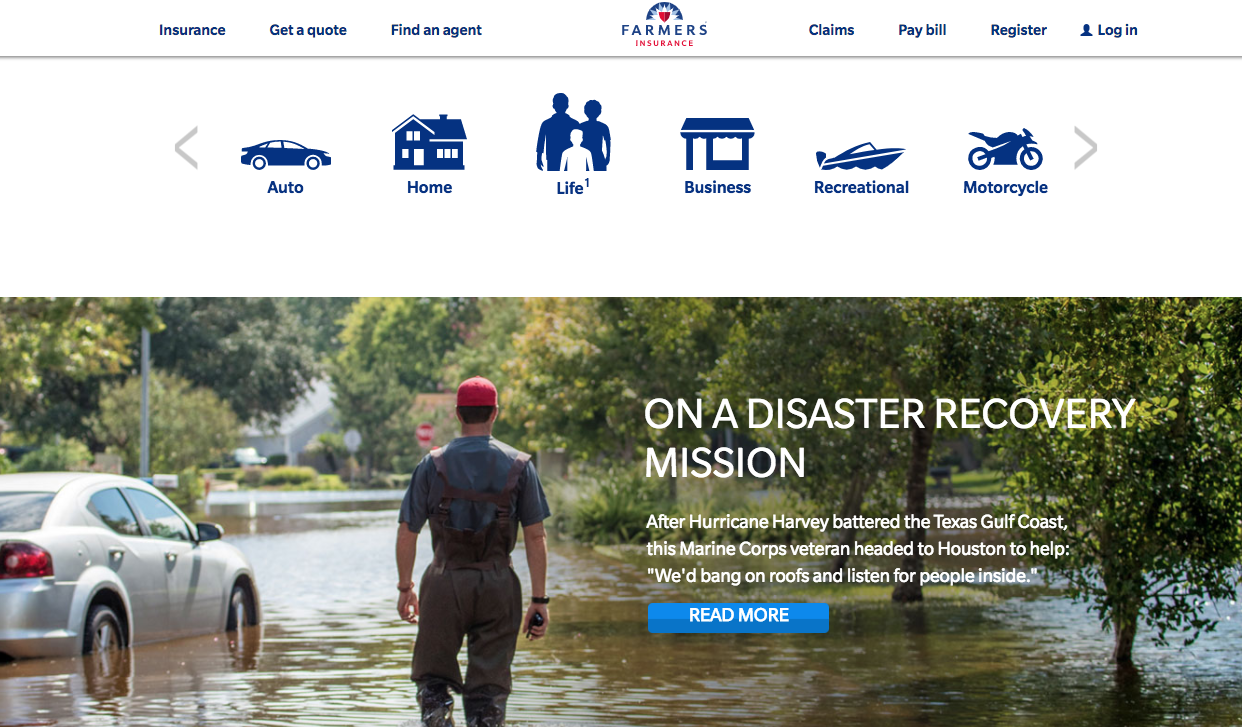

Check out this example of fear-based copy used on the Farmers Insurance website:

Someone shopping for home insurance can see why it’s important to have flood coverage. In the event of a natural disaster, the right insurance is there to protect you.

Come up with ways to market your product the same way. It’s applicable in nearly any industry, even if your company just sells clothes.

It’s going to be a cold winter, so you need to buy a sweatshirt.

Although this type of fear isn’t as powerful as a threat of burglary or natural disaster, it’s still effective.

Take advantage of greed

People are greedy by nature. Don’t think so?

Think about the first day of spring. Ice cream parlors all over the country offer promotions like a free cone or scoop.

Customers line up around the block waiting for an hour to get something free that would normally cost them only a couple of dollars. Why? They’re greedy.

There’s nothing wrong with this. But as a marketer, you can use this concept to your advantage when coming up with new promotions.

Offer items at a discounted rate, and then try to upsell to your customers.

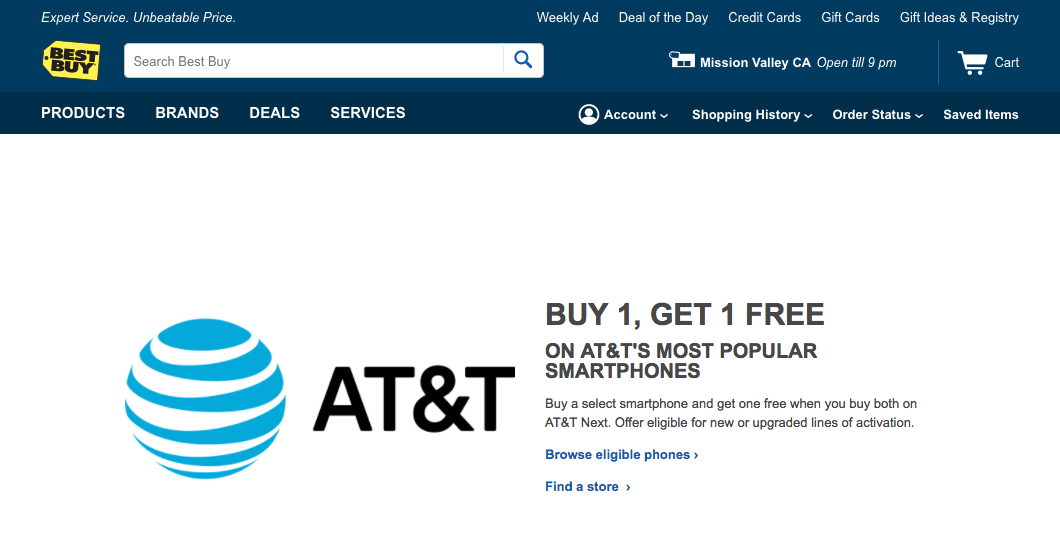

Here’s a great example from the Best Buy website:

BOGO. Buy one, get one.

If someone is shopping for a new smartphone, how can they turn down this offer? If they buy one smartphone, they’ll get another one free.

But this is a great marketing plan because the money isn’t made on the actual devices. Wireless providers make all their profits from their plans.

It’s worth it to give away something that’s worth a few hundred dollars. Now, instead of adding one device to the contract, the customer will add two and pay for two plans.

Try to come up with a way to apply the same concept to your marketing strategy.

Build trust

Typically, words such as fear and greed don’t have a positive connotation. But not every emotion needs to be negative.

Establishing trust with your customers is another powerful way to encourage sales. A great way to create trust is by implementing a customer loyalty program.

Loyal customers will spend more money. But you need to make sure all your offers are transparent if you want to be perceived as trustworthy.

Don’t surprise your customers with any hidden costs or fees when they’re making a transaction.

Anytime someone buys something from you, they trust you with their personal information, such as their credit card numbers.

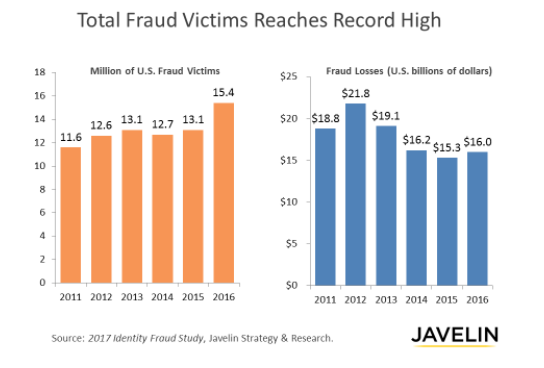

Recent studies show that credit card fraud has become a growing concern in the United States.

If one of your customers hasn’t been affected by fraud personally, I’m sure they know at least a few people close to them who have.

Customers won’t trust you with sensitive information if you can’t convince them your company is trustworthy. You need to take the proper steps to protect your customers’ information and understand the elements that add credibility to your website.

Offering a secure checkout process, free returns, and easy access to customer service will get you started in the right direction.

Add customer testimonials to your website as well.

Once people trust your brand, it will be much easier for you to get higher sales.

Create a sense of belonging

Use your brand to establish a community among your customers. There is a reason why people are buying from your company. All these people have something in common.

It’s your job to figure out what those commonalities are to establish a community based on them.

As a result, you’ll be able to trigger emotions that drive sales.

Here’s what I mean. Let’s say your company sells boxing equipment. Because it’s a niche industry, all your customers obviously have something in common.

They know what it’s like to get punched in the face, and they like to stay in great physical shape. You could create a forum or devote a section of your website to some other user-generated content.

Your customers can share stories with each other about their workout routines and even talk about recent victories or defeats in the boxing ring.

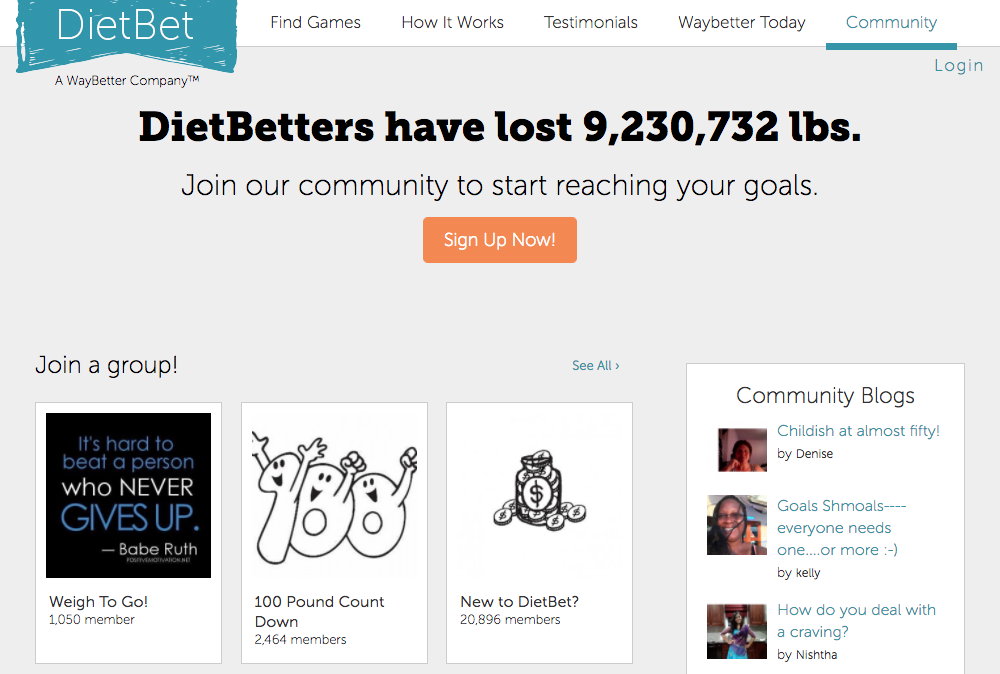

Here’s another example of this concept from Diet Bet:

This website hosts a community of people who all share the common goal of losing weight.

Once you set up a place where your customers feel a sense of belonging, it will ultimately lead to more conversions and higher sales.

That’s because people will have a reason to visit your website more often. They may initially go online to write on a forum but might end up buying something as well.

Eliminate frustration

Frustration is not an emotion you want to have associated with your brand.

Let me quickly tell you a recent frustrating experience I had while trying to buy something online. I don’t want to call out the company, so I’ll leave their name out of this.

I saw something in a physical store location last week when I was walking around. I was interested but didn’t want to carry the product with me for the rest of the day, so I planned to order it online.

The sales associate took my name and email address and sent me the product information, which was supposed to make my life easier.

Well, a few days later I went to the email, clicked on the product, and attempted to check out online. I filled in all my billing and shipping information, and then I was told I needed to create an account to proceed.

Bummer. But I still created an account. Then the site prompted me to enter all my information again.

After entering my name, address, and billing info three different times on the website, I decided to pick up the phone and try to order that way. An automated system told me that all representatives were busy and then hung up the call.

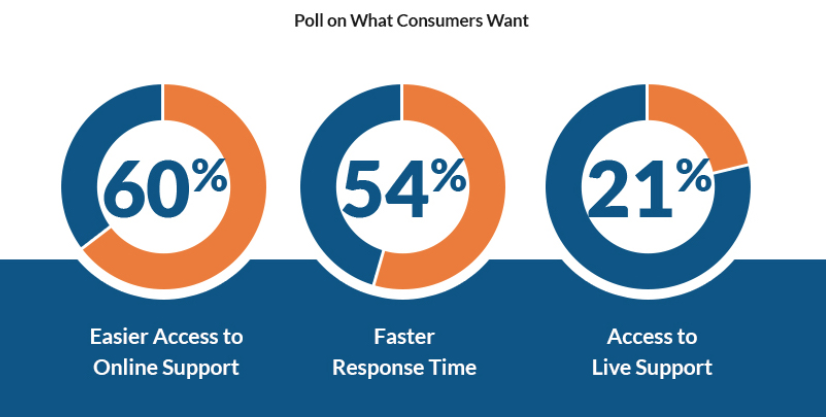

Needless to say, I was so frustrated that I didn’t end up buying the product. This isn’t surprising since the majority of consumers want easy access to online support.

Don’t be like the company I had this awful experience with.

Make sure you have easy navigation on your website and a smooth checkout process. The less friction your customers experience as they go through the process, the less frustrated they will be.

Share your core values

Obviously, every company wants to make high profits. But that’s not the only reason why everyone is in business.

There are certain brands that have other missions that act as the driving force behind their goals. If this sounds like you, make sure you share these values and beliefs with your customers.

For example, are you affiliated with any charities?

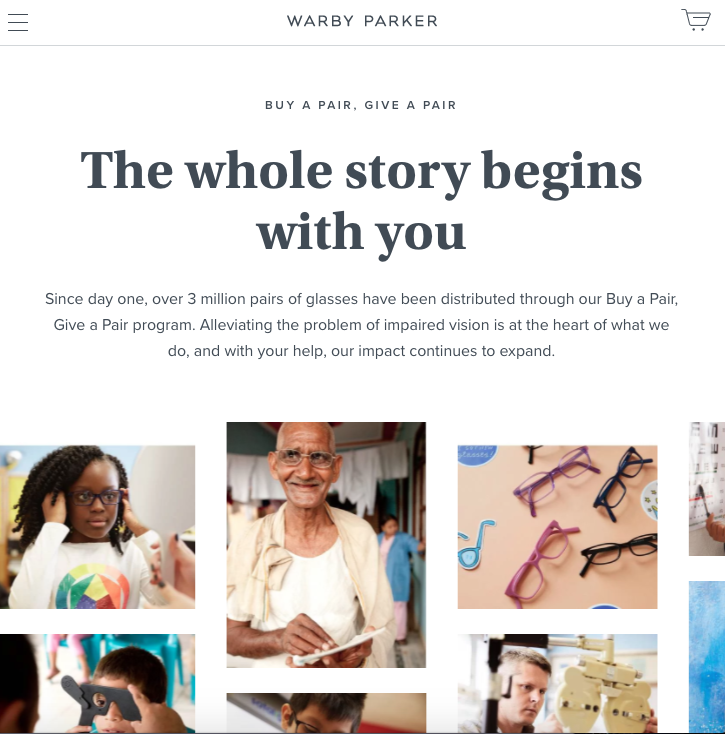

These types of core values can stimulate emotions within customers and ultimately lead to more sales. Here’s an example from the Warby Parker website:

Warby Parker sells glasses. But that’s not all they do. Through their buy a pair, give a pair program, they have been able to donate more than three million pairs of glasses to people all over the world.

Not everyone can afford glasses. So this company does their part by helping those who don’t have the resources or access to eye care professionals.

This type of story can definitely help drive sales because of the emotional attachment to a purchase.

If their customers know their purchases will help someone in need, they will be more likely to buy from the company.

Stimulate desires

What do people desire?

Sex. Food. Sports cars, big houses, and beach vacations.

Incorporate these ideas into your marketing strategy. I’m not saying you need to tell people your product will help them get a new car. But you can still throw a fancy convertible into your ads to help grab someone’s attention.

Think about the last time you saw an advertisement for food on television. The camera zooms in on a cheeseburger and shows juices pouring down the bun.

Everything looks perfect, and it’s supposed to make you hungry. Your mouth might even start watering. Why? Because they are stimulating your desires.

Now you’re craving a cheeseburger, so you go out and buy one.

That’s how emotions of desires lead to sales.

Drive competitive energy

People are also competitive by nature. They are competing with their co-workers and friends, and are trying to “keep up with the Joneses” at home.

Apply this concept to your marketing campaigns.

For example, let’s say you’re selling lawn care products. You could create an ad that says something along the lines of, “Have a better lawn than your neighbor’s.”

Or if you’re selling sports equipment, you could explain how your products will give your customers an edge over the competition.

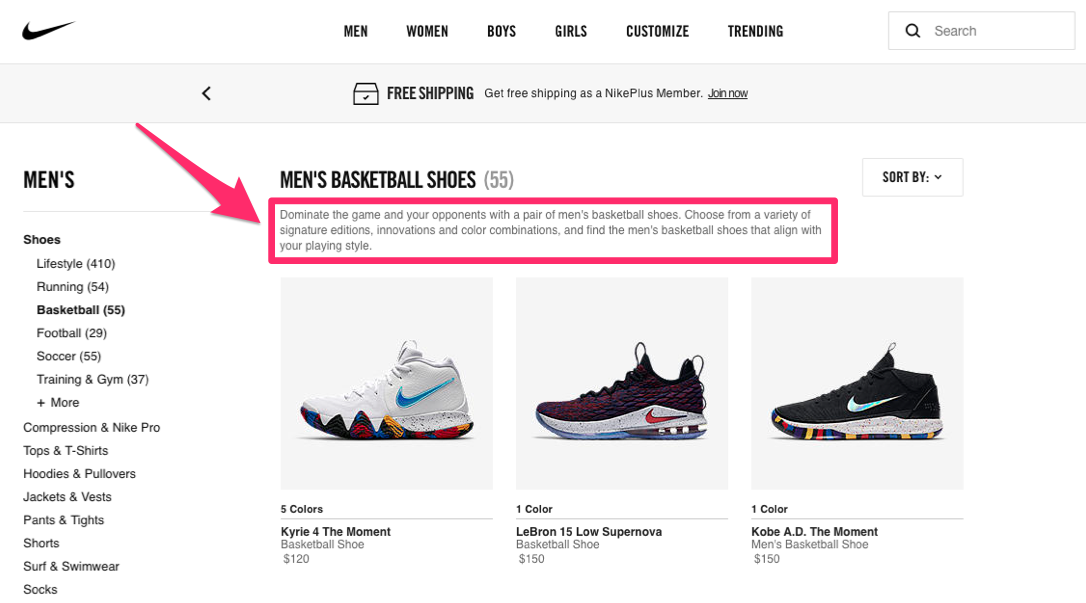

Here’s an example of how Nike uses this strategy to promote basketball sneakers on its website.

They say these sneakers will help you dominate your opponents.

Such phrases can tap into the competitive nature of a customer. This emotional response can lead them to complete the purchase process.

Conclusion

Emotions are powerful.

As a marketer, you need to learn how to effectively stimulate emotions to encourage sales.

Use fear and greed to make your customers behave a certain way. Build trust with your customers, and create a community that establishes a sense of belonging.

Simplify the buying process to eliminate frustration. Share your core values, and proudly display any charitable donations.

Stimulate desires, and focus on the competitive nature of your customers.

If you follow these tips, you’ll be an expert at guiding people’s emotions to increase your sales revenue.

What emotional response does your marketing strategy generate?

Source Quick Sprout https://ift.tt/2IK5kSR

Defeating the Most Common Life Regret

A few years ago, Bronnie Ware, after spending several years working as a palliative nurse who helped people who were dying to enjoy their final days in minimal pain and discomfort, wrote a really powerful book called The Top Five Regrets of the Dying. In it, she collected together the biggest regrets that she heard people consistently share. Here they are, in summary:

1. I wish I’d had the courage to live a life true to myself, not the life others expected of me.

2. I wish I hadn’t worked so hard.

3. I wish I’d had the courage to express my feelings.

4. I wish I had stayed in touch with my friends.

5. I wish that I had let myself be happier.

There are a lot of financial threads running through these regrets, but today I want to really focus on that first one, about which Ware said the following: “This was the most common regret of all. When people realise that their life is almost over and look back clearly on it, it is easy to see how many dreams have gone unfulfilled. Most people had not honoured even a half of their dreams and had to die knowing that it was due to choices they had made, or not made. Health brings a freedom very few realise, until they no longer have it.”

So, let’s look at that chief regret and the financial implications of it.

I wish I’d had the courage to live a life true to myself, not the life others expected of me.

When I read that sentence and reflect on my own life, what I see is all of the things I’ve done and the things I’ve bought that have been done with the primary intent of impressing other people or fulfilling what they expected of me, rather than truly pleasing myself and fulfilling what I expected of myself.

I think of times in my life where I’ve bought things primarily to impress others – the latest gadget, nice clothes, a nice car, a nice house, an impressive career, and so on.

What will people think of how I’m dressed? What will my parents think of my house? What will people think of me if I spring for drinks? What will my coworkers think if I whip out this brand new phone?

First of all, considerations of what other people think of you in terms of financial and personal choices are almost entirely useless unless you can directly tie them to career success. Obviously, there are situations where there is a professional dress code, and there are situations where you need to “dress for success” to influence clients. However, in normal day to day life, most people don’t think about you enough to draw a real judgment about you until your words or actions directly impact them.

Your neighbors barely think about your house, nor do your friends or family. If they do, they’re not making much of a judgment about you, but evaluating whether they want those things in their own life. The same is true for your gadgets or your car or your clothing or anything else.

We mistakenly overinflate how much people think about us, and we do it constantly. This is known as the spotlight effect and it has been established over and over and over again. Most people simply don’t notice you as much as you think they do, particularly when your words or actions aren’t directed toward them or involve them.

So, what can you do to have a good social presence? My strategy is to follow the golden rule in terms of everything I do with other people – do unto others as you would have them do unto you. I don’t care what house people live in or what clothes they wear or what car they drive. I’ll hang out with someone who lives in a trailer or in a mansion if I like the person. I do care that they’re clean and practice good hygiene because that does actually affect me. I want people to be friendly, so I try to be friendly. I don’t want people to backstab me, so I don’t backstab people. I basically act with other people how I would like them to act with me.

The people I enjoy and respect the most in the world often dress in sweatshirts and flannel shirts, blue jeans and beat-up tennis shoes. They drive older cars. They live in modest houses decorated in ways that reflect their own interests, often with things like art done by family members on the walls.

If you carry that philosophy through to your spending and realize that the opinions of others means almost nothing in terms of how you spend your money, then a lot of purchases become far less important. If you’re not worried about impressing others at all (beyond the basics that you would expect from others, like basic cleanliness and politeness), then you’ve eliminated a big reason for spending money.

One of my mentors used to constantly ask the question, “What would you do if you were completely invisible to the rest of the world except for your family?” His philosophy was that if you do those things as much as possible, you’ll have a pretty good life. You could do things that help others, of course, but no one noticed you at all and you knew it. What would you do with your time, once you got bored with the obvious unwinding that most people would do?

How would you spend your days? What would you work on? What would you think about? What is it that you keep inside that you would no longer keep inside? What potential interests do you think of as “dorky” that you’d dabble in if no one saw you or cared about it? How would you dress? What would you use to get around from place to place?

What if you didn’t have to impress people any more, or live up to what you believe to be their standards?

Fill your life with those things and treat others as you would like to be treated and you’ll find that you actually have a pretty happy life, one that doesn’t have many regrets.

You’ll find that the more you commit to that, you begin to realize that there’s actually much less negative consequence from it than you expected, and the pressure to act and spend money to impress others and live up to what you think their standards are goes away. People are very much focused on themselves and their part of their interactions with you, so being who you feel most natural being and doing things you feel natural doing (provided they don’t get in the way of career success) is almost always going to be the best path to personal and financial success.

When I committed to making a financial turnaround in my own life, I was worried that there would be a lot of negative pushback from my social circle at the time. They were very much committed to going out for drinks, one-upping each other with spending, and so on.

What ended up happening? In truth, I got almost no negative pushback from any of them. We didn’t do as much together any more because most of their social choices were really expensive, but there wasn’t any animosity or blowback. A few friends from that group stuck with me; I’d still count a couple of them among my friends even today. Instead, I gradually began to find some new friends and I naturally gravitated toward doing things with them. I started being more true to who I actually was, and there wasn’t a bunch of negative response. Instead, I just strengthened my friendship with those who were friends with me because of me and the others who were merely acquaintances moved on pretty quickly. While some of those people were fun to hang around with, my life became better because I was around people who were more in line with the person I actually am. There was less need to worry about things that weren’t important to me.

Be the person you want to be, not the person you think everyone else expects you to be. As you do that, you’ll come to realize you were spending a lot of money and effort and thought on keeping up that appearance, and as you let that go away, not only are you happier with yourself, most of the people whose perspectives you worried about won’t even care in the least.

Don’t live your life in accordance with the expectations of others. Stop worrying about what other people think, especially since they don’t think about you nearly as much as you think they do. You’ll be in a better place with a lot more money in your pocket to boot.

The post Defeating the Most Common Life Regret appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/2Hus61W

What Is a Line of Credit Anyway? And When Do You Need One?

Here’s one that comes to mind: line of credit.

Of course we’ve all heard of this, but let’s be honest: A lot of us don’t know the exact definition.

And that’s OK. We’ve got your not-too-intimidating explainer — so you don’t feel silly next time someone throws these three little words around.

What Is a Line of Credit, and How Does It Work?

A line of credit is simply a way to borrow money. You can take out a line of credit to pay off a medical bill, consolidate your debt, start a small business or make house payments.

In practice, it’s similar to a credit card, says Bruce McClary, vice president of communications at the National Foundation for Credit Counseling.

Here’s how: You’re approved for a line of credit limit, then you borrow against that credit limit as needed and repay it through monthly payments (plus a variable interest rate). The repayment periods tend to be more flexible than other types of loans, and your monthly payment will depend on your lender. Once you pay off what you’ve borrowed, you can continue to borrow against that line of credit for the amount of the term.

Depending on the type of line of credit you need, you’d go to a bank or credit union — or for a home-equity line of credit (HELOC), you’d go to a mortgage lender. More on that later.

Lines of credit fall into two main categories: secured and unsecured.

Secured Line of Credit

This simply means your loan is collateralized. Translated: You offer up personal property to guarantee the repayment of the money you’ve borrowed.

One of the most popular types of a secured line of credit is a HELOC.

“A lot of people who are homeowners will apply for a line of credit,” McClary says.

Their house, then, acts as collateral, so if they don’t pay what they’ve borrowed back, their house is on the line. (No pun intended… seriously.) Thanks to the collateral, McClary points out, secured lines of credit typically come with lower interest rates.

Unsecured Line of Credit

An unsecured line of credit, on the other hand, typically has a higher interest rate because the lender is taking a bigger risk on you. You might feel less accountable without your collateralized property.

Those who aren’t interested in a large line of credit or who don’t want to offer up collateral might take out an unsecured line of credit.

How’s a Line of Credit Different From a Loan or Credit Card?

If you’re still scratching your head, one of the easiest ways to understand a line of credit is to compare it to a loan and a credit card.

Line of Credit vs. Loan

The biggest difference between a line of credit and a loan is how you’re borrowing the money.

When you apply for a loan, you’re applying for a fixed sum. With the most popular types of loans — home, auto and student loans — you apply for a specific amount, and if you’re approved, you’ll receive that entire lump of money.

With a line of credit, on the other hand, there’s more flexibility. You’re granted a maximum amount you can borrow, but you don’t have to use or accept the entire sum. You’ll simply borrow against it.

For example, if you take out a $10,000 line of credit, it’s possible you only use $8,000 of it. Pro tip: Make sure you can pay off what you use.

Again, with a loan, you’re accepting the entire sum of money and promising to pay it all back.

For that reason, a line of credit could be a better option when you need to borrow an uncertain amount of money, like for home renovations or starting a business, McClary says. Then, you’re not stuck paying off an entire loan — you pay off only what you’ve used.

With both loans and lines of credit, though, you’ll want to shop around and compare rates. For loans, an online loan-comparison marketplace can help you search for lenders offering the best rates.

With a line of credit, you’ll want to look to banks or, for a HELOC, mortgage lenders.

For both, your rates will depend on your creditworthiness.

Line of Credit vs. Credit Card

A credit card and a line of credit share a few more similarities.

“A line of credit is very similar to a credit card, at least in how it works,” says McClary. “The big difference is [a credit card] is designed for maximum convenience. So you’re getting a card… and you take your line of credit with you.”

Both methods of borrowing have limits, but neither requires you to borrow a certain amount. Both are revolving credit: You can borrow and pay back as needed, then borrow more again, during the term of the line of credit.

And with both, you have to keep an eye on how much you’re borrowing to make sure you can pay it off.

It’s worth noting one key difference: With a credit card, you’re paying for convenience, so oftentimes, your interest rates will be higher than that of a line of credit or another loan. The convenience and ease of swiping a card poses a higher risk to the lender.

For context, in 2017, the national average credit card interest rate hovered around 16.15%, according to CreditCards.com. The average line of credit interest rate from Wells Fargo, for example, is about 15%. Your actual rate will depend on your creditworthiness, your type of line of credit and how much you want to borrow.

One other difference: Credit cards can offer cash back and other rewards, like sign-up bonuses, to entice you to use them.

Line of Credit (The More You Know)

There’s no reason to feel silly if you didn’t know how to define a line of credit. Now you’ve got the basics down.

But here’s one final tip from McClary:

“Borrowing is a great way to build your credit score and to achieve the highest credit rating you can. But only if you’re managing your debt responsibly. If you manage it responsibly… that’ll help you finance other things you may want to do later in life.”

If you’re curious about your credit score, you can check it for free online. Tap into your credit report to break down what’s going well (and what isn’t). Taking care of your credit score, like McClary said, can help increase your future purchasing power.

If you find yourself in a scramble trying to pay off your line of credit, McClary encourages you to reach out to your lender for options or to contact a local nonprofit, like a credit counseling program, that can help you get your payments back on track ASAP.

The single most important thing you can do, whether you’re borrowing through a line of credit, loan or credit card?

Keep your spending in line. (Get it?)

Carson Kohler (carson@thepennyhoarder.com) is a staff writer at The Penny Hoarder. She apologizes for that last pun.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder https://ift.tt/2HsdDn1

Can a Travel Agent Get You a Better Deal Than Booking Online?

Direct vacation booking and online travel agencies haven’t killed the old-school travel agent… yet.

When my wife and I planned our honeymoon roughly seven years ago, we went to a travel agent in Newton, Mass., to help us along. We wanted to travel to Paris, Nice, and Barcelona over a 14-day span, wanted to stay in hotels in each location, and wanted to travel by train between cities. The travel agent we used was able to give us hotel recommendations, but couldn’t book a Eurail pass for that time of year (without telling us why), could not find us flights on the dates we wanted, and basically couldn’t put together a package for us.

We left his office, and began searching travel sites for hotel recommendations and airfare comparison sites for flights. We also ended up booking first-class rail travel from Paris to Nice to Barcelona. We didn’t have a price to compare it to, since the travel agent couldn’t even put together a quote — but the convenience made direct hotel and airfare booking staples of our vacation planning from that point on.

But did we sell travel agents short? Is there ever an upside to using a travel agent over an online source?

Naturally, the travel agents think so. The American Society of Travel Agents released a study two years ago noting that nearly half of consumers (47%) booked their travel directly through supplier websites. Another 25% used online travel agency websites including Expedia, Priceline, and others. While the 23% who used travel agents was the highest share in the past three years, it was also less than a quarter of all travel bookings.

“At this point, consumers have tried it all, said ASTA president and CEO Zane Kirby. “They’ve booked online, they’ve gone direct, and they’ve used a travel agent.”

However, Kirby went further by saying the study found that online booking didn’t provide a better deal or save time. According to the ASTA study, almost two-thirds of travel-agent users said using one makes the overall trip experience better. It also asserts that consumers who used a travel agent saved an average of $452 and four hours of work.

Travel agent backers like Host Agency Reviews argue that the hours travelers put into research and booking should be charged at the Bureau of Labor Statistics’ average hourly rate of $26.75. At 22 hours of preparation, they argue, that’s $588 saved by using a travel agent. They also argue that online travel agents’ inventory is limited (though our real-life travel agent said the same about his), that they steered certain clients to higher prices, that their reported prices didn’t include fees, and that travel agents can get better group deals.

Yet the number of travel agents dwindled from 124,000 in 2000 to 74,000 by 2014. According to BLS projections, those numbers are going to shrink another 9% by 2026. And in 2015, Business Insider found that the prices quoted by four out of five travel agents were higher than what they found on their own online.

However, they described travel agents who were the exact opposite of the one my wife and I consulted — attentive agents who put together personal recommendations for cafes and restaurants and bounced different hotel, tour, museum, and ticket prices off of them. These agents even walked them through Eurail and multi-flight combinations for connecting flights. Also, as Business Insider noted, while travel agents will charge fees for specific services like airline booking (ASTA quotes an average rate of $36), they generally don’t charge for the work they’re doing and can serve as a liaison for travelers should something go wrong.

And while traditional travel agents may still have exclusive access to certain discounts, events, and attractions, online bookings are closing that gap. As hotel technology company SoftInn points out, hotel chains including Hilton and Marriott now offer benefits to customers who book directly, including lower prices, free Wi-Fi, and loyalty program points. A Piper Jaffray study reported by Skift notes that 13% of hotel bookings (not including loyalty member rates) were offered at a lower price to those who booked directly, while 21% were cheaper when booked through an online travel agent, and 66% were the same price when booked by either.

“In the end, there remains a strong argument in favor of checking both the hotel sites and the OTA sites, at least for travelers who are not loyalty-program participants,” says Tim Winship, travel industry expert at TripAdvisor-owned travel site SmarterTravel. “For those who are loyalty-program members, when the points and discounted rates are factored in, the case for OTA booking is much weaker.”

Rick Seaney, founder and CEO of travel site FareCompare, has advised that booking packages that combine a hotel stay with airfare and a rental car can typically bring down prices — even during the holidays — simply because it’s easier to squeeze a deal out of hotel or rental car pricing than it is to get a discount on airfare. While online travel agents offer these kinds of packages, companies that lend their services to other travel agents have become adept at this as well.

Only after we booked our honeymoon did we come across Monograms, an offshoot of Swiss travel company Globus. Monograms cobbles together travel packages that include airfare, hotels, certain meals, tours, transport, local guides, and VIP access to attractions. Granted, the prices fluctuate with airfare depending on your departure city, but it gives you at least some idea of what you’ll be paying for the entire experience and leaves flights and other details to either you or a travel agent.

This isn’t exactly a new concept, as my grandparents in New Jersey used Perillo Tours and the ill-fated Club ABC Tours for years. But looking back on some of the trips my wife and I have taken, both the price and perks offered in packages to Ireland, the Benelux countries, and elsewhere were awfully close to what we were looking for.

In conclusion, taking planning out of the equation, we’ve found that direct booking tends to be the cheapest option more often than not. While online travel agents do a fine job of sifting through airfare and hotel options, other cost-cutting measures like vacation rentals and Airbnb are still a rarity on most booking sites. (Though Airbnb listings do come up in Hipmunk‘s hotel search, allowing to compare vacation rentals and hotel rooms side by side.)

However, if you want a hands-off experience that largely requires you to pay and show up, a travel agent or connected tour service can be a great and even cost-efficient option. Just do your homework and shop around before contacting an agent or walking into an office. Also, take the same precautions with any tour company they may suggest. While you don’t have to book online, it still pays to research ratings and complaints there.

Related Articles:

- Here’s How We Took a $20,000 European Vacation for $3,500 Last Summer

- The Disney Hangover: Are Brand-Name Vacations Worth the Price?

- Why I’ll Never Feel Bad About My Vacation Spending

- Three Times Travel Deals Are Actually More Expensive

The post Can a Travel Agent Get You a Better Deal Than Booking Online? appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/2qkIBVY

الاشتراك في:

التعليقات (Atom)