الجمعة، 27 يوليو 2018

President Trump Delivers a Stronger Economy as Promised

Source CBNNews.com https://ift.tt/2uVq8m1

Save money using recyclable coffee cups

News of Starbucks’ new 5p disposable cup fee may spark a groan among coffee connoisseurs and frappe fanatics alike.

Edmund Greaves and Francesca Bloor

Despite the government’s proposed ‘latte levy’ proving unsuccessful, many coffee shops have voluntarily decided to introduce a charge on disposable cups in an attempt to reduce waste.

There are, however, some money-saving schemes that have also been introduced in order to reward environmentally-friendly customers who bring their own reusable cups. Here are the details for some of the big coffee chains:

Caffe Nero recyclable cup discount: Double reward stamps towards a free coffee

Caffe Nero doesn’t have a discount per se, but it will give you two loyalty stamps for each coffee you get in a reusable cup instead of the normal one per coffee.

A spokesperson for Caffe Nero says: “Caffè Nero is a signatory of the 2016 Paper Cup Manifesto, a cross industry public commitment recognised by the Department for Environment and Rural Affairs (DEFRA) to increase the sustainable recovery and recycling of paper cups. We will continue to work with fellow members of the Paper Cups Recovery & Recycling Group (PCRRG) to understand and address the current issues which prevent the widespread recycling of paper cups.”

- Flat white price with a recycled cup: Buy five flat whites with a reusable cup for an overall cost of £13.75 (£2.75 each) to get your sixth free, meaning each one effectively costs £2.30 – a 45p per-cup saving.*

Costa recyclable cup discount: 25p

Costa offers a 25p discount on all hot drinks if you provide your own cup. It states: “Through our nationwide in-store recycling scheme we have recovered over 12 million cups for recycling since February 2017.

“To encourage our customers to use reusable cups we already offer a 25p discount, which we will be further promoting this year.”

- Flat white saving: £2.45 discounted from £2.70.*

Department of Coffee and Social Affairs recyclable cup discount: 10%

Department of Coffee is a small chain with shops based in several major UK cities. Typically its prices are higher than those of the big chains as it serves ‘speciality coffee’ – or coffee with a higher quality grade than is typical for bigger competitors.

It gives customers a 10% discount if they bring in their own cup.

- Flat white price with a recycled cup: £2.70 discounted from £3.*

Pret a Manger recyclable cup discount: 50p

Pret offers a 50p discount on hot drinks for those who bring in a reusable cup. This came about after Pret’s chief executive, Clive Schlee, tweeted in November 2017: “How do we encourage customers to bring reusable coffee cups to @Pret? We’re thinking of increasing the discount for bringing your own cup from 25p to 50p. Our organic filter coffee would cost just 49p. I’d love to hear your thoughts.” Based on the feedback he got, Pret boosted its discount.

- Flat white price with a recycled cup: £1.95 discounted from £2.45.*

Starbucks recyclable cup discount: 25p

Way back in 1998 Starbucks introduced a 10p discount for those bringing reusable cups, which was raised to 25p in 2008. In 2016, it trialled a 50p discount but a spokesperson for Starbucks says the scheme wasn’t a success: “We found that this did not move the needle in the way we thought it might.”

As of July 2018, Starbucks has introduced a 5p charge for customers who buy their drink in a disposable takeaway cup, instead of bringing in a reusable one. The decision followed a trial in 35 London stores, which saw a 126% increase in customers bringing their reusable cups and claiming the 25p discount.

- Flat white price with a recycled cup: £2.40 discounted from £2.70.

*Prices based on visiting a central London branch.

Section

Free Tag

Related stories

Source Moneywise https://ift.tt/2LqXinG

Cheesecake Factory Is Doubling Up With 50% Off Slices This Monday

It’s thick. It’s rich. And frankly, it’s amazing!

There are two kinds of people in this world: those who love cheesecake and weirdos.

For the first group, this Monday could be magical. To honor National Cheesecake Day, everyone’s favorite purveyor of this decadent dessert, The Cheesecake Factory, will offer half-priced cheesecake slices on July 30! To make the deal even sweeter, the chain will also be unveiling two new cheesecakes: Very Cherry Ghirardelli Chocolate and Cinnabon Cinnamon Swirl.

Standard menu pricing for a slice of cheesecake at The Cheesecake Factory is $8, which may seem pretty steep before you taste it. But the slices are huge, and their flavor combinations are a steal at $4.

The offer is good for one slice per guest and dine-in only. But before you groan at the rules, check this out: I called my local Cheesecake Factory to ask about the rules, and learned you don’t even have to order a meal. You can stop in just to have dessert!

Though you don’t have to order a meal, I do recommend a nice glass of wine to pair with the cheesecake. It’s OK. You deserve it.

Think of the possibilities. You could go classic with a slice of original cheesecake. You could feed your chocolate cravings with the Godiva chocolate cheesecake. You can even go guilt-free with a slice of low-carb original or low-carb original with strawberries. You have nearly 40 options to choose from on its tantalizing cheesecake menu.

Call your friends, make a date with your spouse or significant other, or just treat yourself to a solo date. It’s a treat we all deserve.

Tyler Omoth is a senior writer at The Penny Hoarder who loves soaking up the sun and finding creative ways to help others. Catch him on Twitter at @Tyomoth or snarfing down a slice of cheesecake around Tampa, Florida, this weekend!

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder https://ift.tt/2LrqyuC

How to Turn Your Business Idea Into a Startup Company

Ideas are a dime a dozen. Everyone has them.

Some ideas are great, and others could be improved.

As an online marketer, I’ve heard countless business pitches from prospective entrepreneurs over the years. While I admire their creativity, just coming up with an idea alone is far from having a viable business concept.

If you are ready to put your idea to the test and launch a startup company, I encourage you to read this guide.

Your idea needs validation.

The last thing you want to do is launch a new business and realize six months down the road that it wasn’t a good idea. By this point, you’ve already sunk too much time and money into the venture.

Don’t skip any steps in the startup process.

Here’s what I’ve done. I’ve outlined how you can take an idea and turn it into an actual business. I’ve tried to keep this guide as general as possible so that it can speak to the widest audience of entrepreneurs.

For example, some businesses will need to buy or lease retail space. Other brands will need production equipment or partnerships with manufacturing facilities.

Some of you may even need permits and have to meet certain legal obligations before your launch. I stayed away from going into depth on these types of details.

That said, this is an excellent reference for anyone with a business idea and no experience launching a startup.

Even if you’ve been part of startup launches before, this guide can help you avoid some mistakes you may have made in the past.

Write a business plan

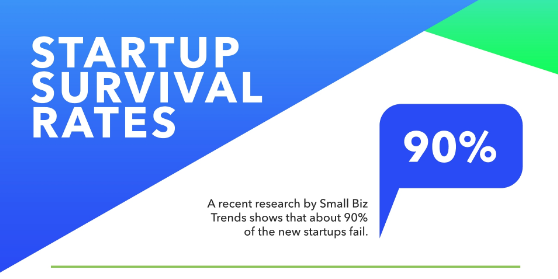

When you approach your new business venture without a plan, you increase your chances of failure.

The odds are already working against you since such a large percentage of new startup companies fail.

You need to do everything possible to try to give yourself an advantage and increase your chances of success.

Here’s a pretty common conversation I have with entrepreneurs. They pitch me an idea and follow up with something like, “Wouldn’t that be a great business?”

My honest answer is I truly don’t know. And they don’t know either.

Many ideas sound good when they’re verbalized. But when it comes to the logistics, finances, and other important details, the idea may not be as good as you initially thought.

That’s why you need to learn how to write a business plan for your startup company.

Your business plan will help you tremendously and ultimately increase your chances of succeeding.

Startups with a business plan have a 29% greater chance of securing funding, which we’ll discuss in greater detail shortly. Writing a plan also increases the chances of business growth by 50%.

These are the common components of a business plan:

- executive summary

- description of the company

- market analysis

- competitor analysis

- organizational structure

- details about products and services

- marketing plan

- sales approach

- budget and funding

- finances

Your plan will outline everything you need to do, even if your idea is very simple. For example, let’s say you’re planning to sell shirts.

How are you going to sell them? Where will you sell them? Whom will you sell them to? At what price will they be sold?

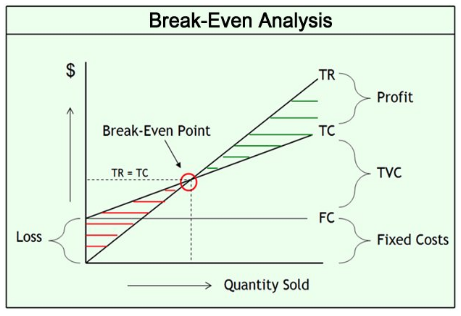

You’ll explain in detail your costs to produce the shirts. The business plan will even outline when you plan to break even on your investment.

The financial projections section is arguably the most important part of the entire plan.

You need to come up with realistic numbers. In addition to listing all your expenses, you need to project your sales.

This information will help you determine if your new business can generate money. You’ll be able to come up with price points so you can turn a profit.

Again, you must figure all this out before you open the doors of a new business. It starts with proper planning.

Define your target audience

The idea for your new business might sound good, but for whom is it a good idea?

Whether you have a product, service, invention, or modification to an existing product, you need to clearly define whom you’re selling to.

I hear people say all the time:

“Everyone will like this idea.”

This is simply not true. Plus, from a marketing perspective, it’s unreasonable to try to launch a brand intended for everyone.

Imagine trying to come up with promotions that appeal to men, women, and children of all ages from every corner of the world. It’s not a realistic approach.

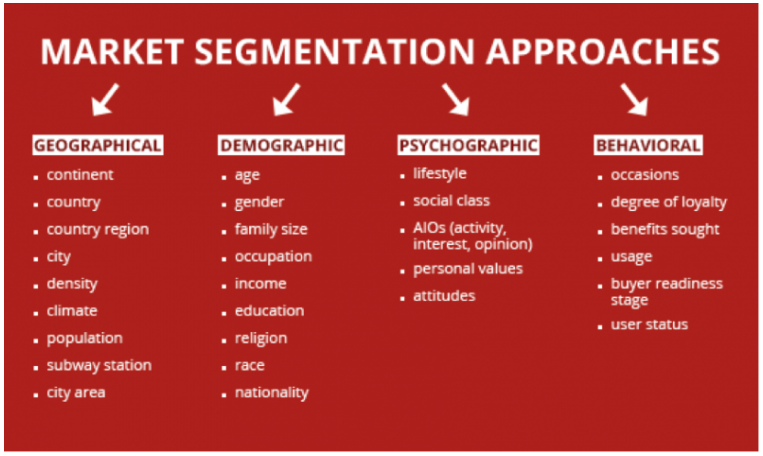

You need to learn how to identify the target market of your startup.

Start with broad assumptions about your prospective customers, and narrow it down even more.

Begin with factors such as their ages, genders, and physical locations. Then get more specific, and identify their interests and lifestyle habits.

Here are some ways for you to segment your audience based on geographic, demographic, psychographic, and behavioral categories.

For example, let’s say your product is intended for males between the ages of 25 and 40. That’s still a broad audience.

You can make it more specific by saying you’re targeting males between the ages of 25 and 40, who live in the United States, make more than $60,000 per year, and are interested in fitness.

Do you see the difference? That’s much more detailed. You can develop a customer persona to help you with this process.

Also, you need to look at your target audience from different perspectives. Let’s say you’re launching a startup that sells toys for young children.

That’s not necessarily your target market.

Three-year-old kids don’t buy stuff. You need to target their parents instead. Make sense?

Conduct market research

Now that you have an idea of whom you want to target, it’s time to test that theory. Just because you think your idea is great for a specific market doesn’t mean this is true. You can use:

- surveys

- interviews

- focus groups

- beta testers

- product samples

You need to get out there and talk to people. Validate your idea.

It’s also necessary to figure out who else is offering the same thing you are. Today, it isn’t easy to come up with an idea that’s 100% unique.

Don’t get me wrong: it doesn’t mean you can’t make money by having the same idea as someone else. But if the market is oversaturated, it might not be in your best interest to proceed.

I’ll give you a simple example to explain what I mean. Let’s say you want to open a pizza shop in your city.

You’ve scouted out a location that can fit your ovens and tables. You can rent it at a reasonable rate. Your pizza recipe is outstanding. Plus, everyone likes pizza, and more than 100,000 people live in the city.

This idea must be a homerun, right? Not if there are 20 other pizza shops within a few blocks of your prospective location.

It’s going to be too difficult for you to compete with a market that’s so saturated.

This is an example on a small level, but you can scale it to any industry. Look at the ecommerce space. There is a huge competition globally.

In addition to niche brands, you’ll also be competing with giants such as Walmart and Amazon.

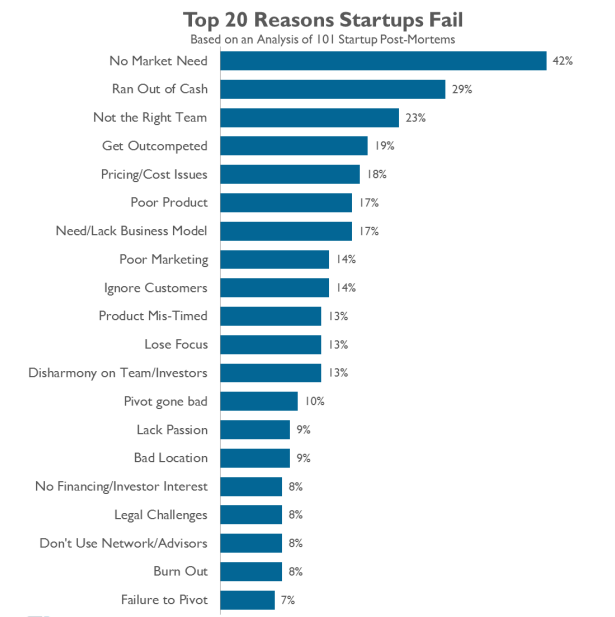

The number one reason why startups fail is that there is no market need.

While your idea might be cool, there may not be a need for your product or service.

Or even if the market needs what you’re offering, it could be getting it from someone else already.

Market research will also require you to analyze your competition.

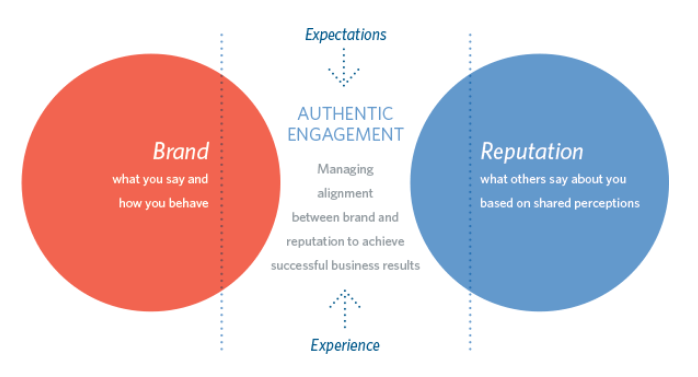

Establish your brand

Your startup company needs to have a differentiation strategy that separates you from your competitors.

What’s your identity?

Your brand may be cool, edgy, and trendy. Or maybe you’re going for a brand identity that is conservative and family-oriented instead.

Some startups launch with a mission to help a greater cause, such as a nonprofit organization.

No matter what your brand identity is, it needs to be clear to your audience. All of your branding campaigns will reflect the image you’re trying to portray.

Your website colors, marketing campaigns, and promotions will speak to your brand identity. This even relates to your logo and the name of your startup.

Come up with a name that doesn’t restrict your growth. Even if you’re focusing on something specific right now, you don’t want the name of your brand to put you in a box, preventing your expansion in the future.

Your brand needs to speak to your target audience, which was already defined. A proper branding strategy will nurture your brand reputation.

In a perfect world, your brand image and brand reputation will be the same. You want people to see your company in a positive light.

So it’s important to get your branding strategy right the first time because your reputation is going to stick with you for years to come.

It’ll be hard to rebrand yourself in the future if you make a mistake during the launch stages, so don’t rush into anything.

Surround yourself with the right people

It’s time to assemble your team.

The size of your team will vary based on the type of business you’re launching.

You want to find people strong in areas where you are weak. For example, if you’re extremely creative but don’t have managerial skills, it doesn’t make sense to bring another creative mind on board without hiring someone who can manage employees.

Or let’s say you’re building a mobile app but don’t have any experience with coding or design. You’ll need to hire a developer and designer.

Surround yourself with people whom you are compatible with. You want to build strong working relationships with your team.

Here’s another problem I see all the time. People launch a startup and just start hiring their friends and family.

Don’t get me wrong — this can work. But you need to think long and hard about this decision. Do you want your personal relationships to be impacted by the business?

Can these people take directions from you? What if you need to fire your best friend?

These are all sticky situations, so tread carefully. You also need to make sure every member of your team can bring something to the table.

Just because you were bouncing ideas off a friend a few months ago doesn’t mean they’re part of the business.

I’m not saying you need to be selfish or stingy, but ultimately, you need to do what’s best for you and your business.

Secure funding

Your startup will need some money to get off the ground. Depending on what you’re doing, this can range anywhere from a few thousand dollars to millions of dollars.

Everyone’s situation is different. You’ll need to recognize all your business costs. Here are some examples to consider:

- research and development

- equipment

- cost of property to buy or lease

- website and server

- inventory

- insurance

- legal fees

- payroll

- startup costs

- operating costs

You need to realize you won’t have any income when you first launch, but you’ll still need to cover all your expenses.

Based on this information, you’ll be able to determine how much money you need. Learn how to get your startup funded.

Use your business plan and financial projections when you’re speaking with prospective lenders or investors.

You may consider getting a bank loan and pay interest fees for the funds you borrow. But big banks may not be your best bet. Just look at these approval rates for small business loans:

For your startup company, you may want to consider some alternative options:

- venture capitalists

- angel investors

- personal savings accounts

- friends and family

- crowdfunding

These are all reasonable sources to raise capital to launch your startup. You’ll just have to consider these options and decide which ones are the best for your scenario.

Figure out if it’s worth giving up equity in your company. Will your investors bring anything else to the table besides cash?

While it may be nice to have other opinions, you want to make sure you have the final say in all decisions. There is nothing wrong with giving up some equity, but just don’t lose control of your company.

Build hype before you launch

Everything is falling into place.

Your business plan looks good. The target market is clearly defined. All your market research is complete.

The team you assembled is qualified. All of your funds have been secured.

Now it’s time to put your company branding strategy to work.

Buy a domain name. Launch your website. Create social media profiles.

Start to market your brand. Even if you’re not officially launched or selling anything just yet, you can still take pre-orders.

Create a blog. Try to get featured on press releases or news articles. Send free samples to influencers.

Do anything that will make your presence known. Get creative with guerilla marketing and content marketing strategies.

Be prepared to work

Before you officially launch, you need to ask yourself if you’re ready to work.

Sure, you know your idea is great and it’s been validated through your research. But are you ready to take the plunge into entrepreneurship?

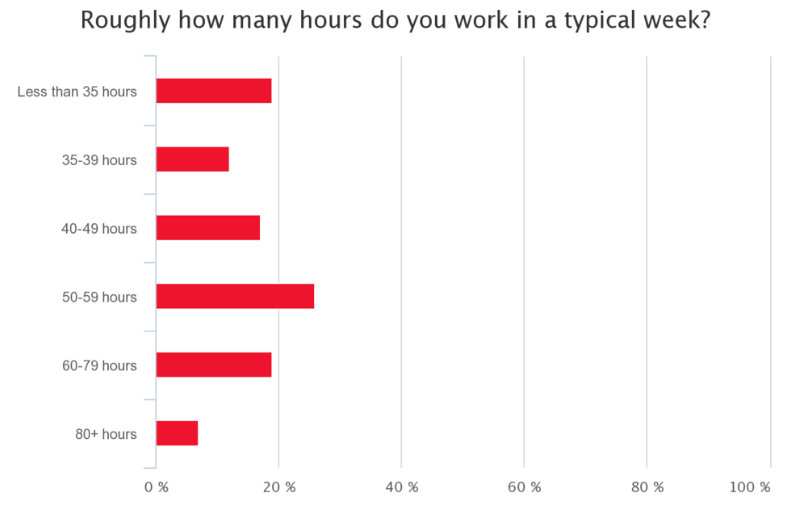

Just look at how many hours the average entrepreneur works per week:

In order to launch your startup, you might be leaving a job with a steady paycheck to work twice as hard on your new business, without being able to pay yourself for years.

Is this something you can handle mentally and financially?

Research shows 41% of entrepreneurs say they feel stressed almost every day. An additional 33% say they feel stressed a couple of times per week.

But only 7% of entrepreneurs say they never feel stressed.

Unlike with a regular job, there’s no quitting on your own business. You can’t call in sick when you don’t feel like working.

You’re the boss. You set the tone for the entire culture of the company.

While being your own boss definitely has lots of benefits, it also comes with added responsibility and plenty of sleepless nights. You need to recognize that your startup can still fail.

I’m not saying all of this to discourage you from following through with your plan, but you need to accept this reality.

But if you’re willing to take these risks and get to work, proceed with your business plan, and make it happen.

Conclusion

There is a big difference between an idea and an established business. You need to take steps to validate that idea before you launch a startup company.

Write a business plan. Identify your target market. Conduct market research.

Then you’ll need to come up with a branding strategy.

Assemble your team. Surround yourself with people who can contribute to the success of your new business.

Recognize your costs and outline your financial projections. This will give you a better idea of how much money you need to launch your company.

Being an entrepreneur can be rewarding, but it’s no walk in the park. You need to ask yourself if you’re capable of being a business owner.

But if you’re ready to work and you’ve taken the steps I’ve described in this guide, you can turn your business idea into a reality.

What steps have you taken to turn your concept into a startup company?

Source Quick Sprout https://ift.tt/2LQDeHA

Why It’s Crucial to Start Saving for Retirement Now

One of the main reasons that people choose not to start up their 401(k) (or 403(b) or TSP or other such plan) at work is because they’re simply overwhelmed by all of the options available to them and they’re worried about not choosing the “best” one and losing money. This was a concern I had at my first job when signing up for my retirement plan for the first time, and it was voiced by others in the room during the orientation session. It’s also been a concern noted by many readers over the years. They didn’t sign up because of option overload – they partially filled out the form, then felt overwhelmed by the options, then just sat it aside and took no action on it.

This is a bad move. You are better off choosing almost any investment option and starting to save now rather than putting it off.

Let’s look at two case studies.

Jane is 25 years old. She has her first “real” job and plans to retire at 65. On the first day, she goes in to sign up for her retirement plan and chooses an investment that offers a 7% average annual return on her contributions. She starts contributing $2,600 a year and her employer matches that, also contributing $2,600 a year.

After 40 years of this, when Jane is 65, she’ll have $1.15 million set aside for retirement.

Now, let’s look at Robert. He’s also 25, at his first “real” job, and also plans to retire at 65. On his first day, he goes in to sign up for retirement and balks at the options. He stuffs the forms in his desk and forgets about them. At age 30, he is finally nudged by his parents and wife into contributing to his retirement account, so he carefully studies the options and chooses that same 7% option that Jane chose. He starts contributing $2,600 a year and his employer matches that, also contributing $2,600 a year.

After 35 years of this, when Robert is 65, he’ll have only $800,000 set aside for retirement. Waiting just five years cost Robert $250,000. Another way of looking at it: waiting for 12.5% of his working years cost Robert around 22% of his total retirement savings. That’s a big loss.

There’s almost no doubt that starting now is better than starting later, but what about the fear of choosing a bad investment? Wouldn’t you be better off waiting and doing the research and choosing a much better investment in a year?

Here’s the issue with that: you can do that regardless of whether you’re contributing right now or not. If you start contributing right now and put it in a money market fund – meaning there’s virtually no risk and something around a 2% annual return – you can still make your investment decision a year from now and already have a year’s worth of contributions sitting there. If you don’t do that, you have nothing a year from now. In the case of Jane and Robert, that means they’d have about $5,250 or so ready to invest in something at the end of the first year if they just chose a money market account (with basically no risk) instead of choosing no contribution at all.

So, starting now and contributing to something extremely safe, then choosing a better investment and moving later is better than contributing nothing now, choosing a better investment, and starting later.

Let’s address another common issue that comes up in these discussions: the “market timing” scenario. You’re about to sign up for your 401(k) but you’re simultaneously afraid that the stock market is about to have a 1929 or a 2008 year and drop 40% in value, so you don’t sign up.

In this scenario, the same thing holds true: Just start contributing now and put it into something safe, then move it over when you feel the time is right. By not signing up, you simply miss out on those years of contributions.

However, the idea that you can time the market is a fallacy. As I wrote late last year in Why You Can’t Time the Market: Thoughts on Investing in Stocks:

Do you have a time machine? No? Then market timing isn’t worth it.

You can’t guess day to day where the peaks and valleys of the market are, and if you miss it by much, you’re going to cut enormously into any advantage you might get from market timing. Add into that the fact that you’ll be paying brokerage fees and you’re devoting a lot of time to study, and the disadvantage grows.

The much better approach is to do things passively. Only invest in stocks if you have a goal that’s more than a decade in the future. Buy a broad based index fund (like the Vanguard Total Stock Market Fund) and reinvest the dividends. Then ignore it until you actually need the money. The market will go up. The market will go down. It doesn’t matter.

If you’re not able to actually predict the day to day peaks and valleys of the stock market – and even large scale investors who do this for a living can’t do it really well over a large period of time – then market timing isn’t going to help you. In fact, if you’re very much off the peaks and valleys at all – and as a casual investor, you will be – you’re likely going to do worse than if you just put money in there and didn’t think about it at all.

In other words, for people just signing up for a 401(k), timing the market is a fool’s game that will probably result in losing money.

What about the worry of a “lemon investment”? This is another concern that people often bring up in these situations. They’re concerned that the retirement investment option they choose is a “lemon” with poor returns and high fees.

That’s true – you might wind up in an investment that doesn’t have great returns or might have high fees. That’s still better than contributing nothing. A 6% return on your money when you could have had 7% (by picking a better investment) is still way better than a 0% return on your money when you could have had 6% (by contributing to the lemon).

Furthermore, with almost every retirement account out there, you have the ability to change your investments at any time. If you keep researching and realize you’re in a lemon, you can move your money to a better investment within that account with no tax consequence. Just log in and change it.

In short, if you end up making a bad choice, you can always correct it later, and whatever reduced amount you earned in that investment is better than earning nothing by not contributing at all.

Okay, one final question. What if you literally have no idea what to choose, and that fear keeps you from making a choice?

The first thing I’d do is simply ask the human resources officer or other employee that is helping you sign up for retirement for their recommendation. They’re typically given some basic guidance to help people find a retirement option that’s right for them. Follow that advice for now. Often, this advice will lead you to a “target retirement” fund, which is a solid default choice.

Later on, as you learn more about investing (or you have someone advising you), you (and/or your advisor) can research the investment you’ve chosen as well as the other options available within your retirement account and, again, if you find something that seems to be a better option, you can move at that time.

The moral of the story is this: You are better off saving for retirement right now rather than later, regardless of how you choose to invest that money. If you choose to leave it in cash for a year or two within your 401(k), you’re still better off in the long run than doing nothing at all. If you put it all into stocks and the stock market bottoms out next year, you’re still better off in the long run than doing nothing at all. If you put it into an awful investment and don’t figure it out for a few years, you’re still better off than doing nothing at all.

Why? Because even after all of those potential issues, you still can’t beat the sheer power of saving for retirement early and letting the power of compound interest work in your favor for as long as possible. The only way to do that is to start now.

If you have a retirement plan at work that you haven’t signed up for, do it today. Don’t wait. Start the contributions now, even if you can afford very little. If you don’t have a retirement plan at work, sign up for a Roth IRA and start contributing, even if you can afford very little. Make moves in your life (like adopting frugality or paying off debts) that will allow you to bump up those contributions as soon as possible. That way, you’ll be as ready for retirement as you can possibly be, and that’s one less little piece of background stress on your shoulders as you move through the many years of your life.

Good luck!

Related Reading:

- The Snowball Effect of Retirement Savings

- The ‘Perfect’ Investment

- How Do I Even Start With Saving for Retirement?

- Don’t Let These Fears Stop You From Investing

The post Why It’s Crucial to Start Saving for Retirement Now appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/2NRAYRc

Compare broadband, phone & TV packages

- Lowest Prices

- Compare & save £200 +

- See deals in your area

Image

CTA

Legal

Section

Source Moneywise https://ift.tt/2LFDOLy

8 Tips for Anyone Who’s Counting the Minutes Until Their Next Paycheck

And people with low incomes aren’t the only ones struggling. About 1 in 10 workers surveyed who said they earn six figures or more reported living paycheck to paycheck.

Breaking the paycheck-to-paycheck cycle is never easy; if you plan to try, you’ll have to take a hard look at your mindset and habits.

8 Ways to Break the Paycheck-to-Paycheck Lifestyle

“Money Girl” host Laura Adams outlines tactics for breaking the paycheck-to-paycheck cycle in the episode “8 Tactics to Stop Living Paycheck to Paycheck.” By saving even a small amount each month, you can achieve greater financial security and finally feel less stressed about money.

1. Acknowledge the Problem

If you’re not saving money, you’re one emergency away from financial disaster. Your first step is to figure out why it’s so hard for you to save. Maybe you’re overspending, or perhaps you need a side hustle because your paycheck barely covers your bills. Once you figure out the “why,” you can change your habits to start saving money.

2. Stop Worrying About Your Self-Image

When you obsess about looking successful, you risk living a lifestyle you can’t afford. No amount of material goods will make you happy. Focus on yourself and your goals, and find ways to fill emotional voids that don’t require spending.

Another pro tip: Learn to say “no.” Repeat it whenever someone pressures you to overspend or distracts you from your goals.

3. Track Your Spending

If you want to have cash left over from your paycheck, you need to track everything you spend. There are tons of tools that you can use to track your spending, including budgeting apps, Google Sheets and Excel. Or you could take the old-school approach to budgeting by documenting each transaction in a paper notebook.

4. Focus on Your Biggest Expenses First

If you’re living in a home you can’t afford or drive a car that’s beyond your budget, you’ll probably never stop living paycheck to paycheck, no matter how much you cut the smaller stuff.

Try to avoid spending more than 20-25% of your gross income on rent or your mortgage, even if that means you need to downsize by finding a smaller place, get a roommate or move in with family. Your car payment shouldn’t eat up more than 10% of your gross budget, so consider a cheaper ride or alternative transportation if you’re paying too much.

5. Re-evaluate Your Debt

By refinancing your home or consolidating your credit card debt, you could save big bucks on interest. Adams’ Online Loan Comparison Chart can help you compare your lending options.

6. Set Up Automated Savings

Automation is your friend when it comes to saving money. You’ll be less tempted to spend money when you save it before you have the chance to touch it.

If you contribute to a workplace retirement account like a 401(k), you’ve already automated savings because contributions can only be taken out of your paycheck. Consider setting up automated transfers to an individual retirement account (IRA), 529 savings plan for your child’s education or a savings account.

7. Find Ways to Earn More Money

Sometimes cutting expenses isn’t enough. If you need to make more money, consider getting a second job, working extra hours at your primary job or taking on a side hustle. There are tons of ways to earn extra money, such as driving for Uber or Lyft, grocery delivery, taking online surveys, and more. Or, perhaps it’s time to make the case to your employer that you deserve a raise or promotion.

8. Focus on Future You

It’s frustrating when you feel like your paycheck never goes far enough, but change takes time. Focus on where you want to be in the long term — think five, 10 or even 20 years down the line. By thinking about the big picture, you can set smaller goals that will help you get there someday.

Listen to the full podcast for the full eight tips on breaking the paycheck-to-paycheck cycle, plus find bonus tips for saving on your electric bill from The Penny Hoarder’s Lisa Rowan.

Robin Hartill is a senior editor at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder https://ift.tt/2JZ2ZUx

US Economy Surges to 4.1 Percent Growth Rate in Q2, Best Showing Since 2014

Source CBNNews.com https://ift.tt/2mLLC05

We’re in College. We’re Newlyweds. We’re So Broke. Where Can We Turn?

Getting married is challenging. Being young and newly married — even more so.

I got married three weeks into my freshman year of college. Not long after, I sauntered into my old high school feeling pretty invincible. Look at me: I am an adult, married lady. I swung by my favorite biology teacher’s room to chat, and when he asked how we were doing, I made an offhand comment about being broke.

He stopped sorting student papers and looked at me squarely. “The money will be tight for a while,” he said. He told me a few details from when he and his wife were starting out, when their kids were young. He didn’t make any comments about how old I was or why I had gotten married so soon after high school. He just leveled with me about how hard it can be to make ends meet in a young marriage.

So if everything feels impossible for you right now, it’s probably because it kind of is. So many of us are not prepared to be fully functioning adults when we leave home. And then you have to be a functioning adult in the same house as another newly functional adult? It’s ripe for conflict.

Filing for bankruptcy at 20 is probably not a viable option. But applying for government assistance can be a huge help for you during this time when you’re juggling health issues along with the pressure to earn as much money as possible.

You may be eligible for SNAP, the benefit formerly known as food stamps. The government assistance program is designed for working adults with limited assets. You can even apply for SNAP online in many states, so you don’t even need to talk to someone to ask for help.

You could also consider dropping down to half-time status at school. You can usually retain financial aid if you’re taking at least six credits each semester, although school rules vary. It may take longer to complete your degree, but reducing your course load for a semester or two could bring extra peace of mind while you determine the best way to figure out work schedules and medical needs with your husband.

Asking for help is hard, but asking for help now can set you up for greater stability in the future. This is not a time to hide your fears about your finances from family members, friends, and most importantly, each other.

If you don’t talk about what’s worrying you, it’ll eat away at you both.

Lisa Rowan is a senior writer at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder https://ift.tt/2mNJsNK