Camelback Resort’s receives Platinum International Aquatic Safety AwardCamelback Resort, Tannersville, has been awarded the prestigious “Platinum International Aquatic Safety Award.” Earning this award demonstrates that the aquatic facilities they operate — Aquatopia Indoor Waterpark and the outdoor Camelbeach Mountain Waterpark — consistently exceed industry standards in risk management and epitomize aquatic safety [...]

Source Business - poconorecord.com http://ift.tt/2DMfyjP

الاثنين، 29 يناير 2018

A Place for Mom Is Filling Multiple Work-From-Home Customer Service Jobs

If talking on the phone and solving problems are two of your favorite pastimes, we’ve got some jobs for you.

A Place for Mom, the largest senior-living referral service in the U.S., is looking for an onboarding coordinator and a customer service coordinator. Both jobs require communicating over the phone and through email with A Place for Mom customers and partners.

These jobs with A Place for Mom are totally remote, so you have the freedom to work from the comfort of your home office (or couch).

But if these jobs aren’t calling your name, no worries. Check out our Jobs page on Facebook, where we’re always posting new work-from-home opportunities!

Onboarding Coordinator at A Place for Mom

A Place for Mom is looking for a work-from-home onboarding coordinator. In this position, you would be working with senior living communities that are new partners.

Pay: Hourly, not specified

Responsibilities include:

- Developing relationships with new partners

- Assisting new partners to ensure they have a proper onboarding experience

- Scheduling meetings with new partners to establish expectations

- Organizing and delivering orientation webinars to educate on best practices

- Following up with new partners regularly

- Preparing weekly reports for the senior manager and partner development teams

Applicants for this position must have:

- Two to three years of experience in customer service

- Ability to properly communicate with executives via phone or email

- Excellent organization skills

- An enthusiasm for building and maintaining relationships

- The ability to prioritize responsibilities while meeting work expectations

- Microsoft Office Suite proficiency

Nice to haves:

- A bachelor’s degree

- Previous experience with A Place for Mom or another senior living service

Apply here for the work-from-home onboarding coordinator job.

Customer Experience Coordinator at A Place for Mom

A Place for Mom is also looking for a work-from-home customer experience coordinator.

You would be in charge of answering questions and concerns from partner senior living communities and affiliate brands.

Pay: Hourly, not specified

Responsibilities include:

- Answering calls and emails from communities

- Verifying accuracy of data used by the Senior Living Advisors team

- Contacting communities that submitted cancellation notices

- Taking part in team meetings/calls

- Handling any concerns from partners

Applicants for this position must have:

- An enthusiasm for customer care and building relationships

- Ability to use customer relationship management software and tools

- The focus to work independently while meeting deadlines

- Microsoft and Google Suites skills

- A designated work-from-home office space that is free from distractions

- The ability to work a 40-hour week

Nice to haves:

- A bachelor’s degree

Apply here for the Customer Experience Coordinator Job at A Place for Mom.

Kaitlyn Blount is a junior staff writer at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2DLEIz3

You Don’t Need Dough to Get a Chocolate Croissant at Au Bon Pain on Jan. 30

Tuesday, Jan. 30 is probably one of the best days of the year.

Why, you ask? Because it’s National Croissant Day, silly goose.

To honor such a holy day, the saints over at Au Bon Pain will offer a free mini chocolate croissant.

How to Get Your Free Croissant at Au Bon Pain

The deal runs from 2-5 p.m. local time at participating locations. All you have to do is show up.

Some locations have shared Facebook events, but you’ll want to call the one nearest you just to make it’s participating.

Not much tops croissants in my book, except for free croissants. So don’t flake on this deal, or you’ll feel pretty crumby.

Until our paths croissant again.

Stephanie Bolling is a staff writer at The Penny Hoarder. She has a slight penchant for croissant puns.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2GviRO2

This Airline’s Hiring Work-From-Home Sales Agents And Includes Free Travel

Ready to soar to new heights with a career in aviation?

OK, maybe they’re not exactly as glamorous as Dylan McDermott’s gig as a fictional pilot, but these Alaska Airlines jobs let you work from home full time as a reservations sales agent.

The jobs pay $12.33 an hour and offers the standard benefits, as well as a generous employee travel program that lets you enjoy unlimited, free standby flights.

You must live within 100 miles of the company’s call center in Boise, Idaho, where you’ll need to go for training and occasional in-office work. And during training, you’ll have to pass weekly exams before you can earn your reservation agent wings.

The airline has previously sought reservation agents in Arizona.

The call center is open 24/7/365, so you’ll need the flexibility to work weekends, holidays and late nights, answering incoming calls and assisting customers.

You’ll also be part of a union, which requires initiation fees and monthly dues.

And like any good pre-flight instruction, Alaska Airlines’ post reminds you that smoking is prohibited throughout the cabin: You must be nicotine-free for the past six months — that includes nicotine patches and gum.

If this job doesn’t engage you in a flight of fancy, just check out our Jobs page on Facebook. We post new opportunities there all the time.

Reservations Sales Agent at Alaska Airlines

Pay: $12.33/hour

Responsibilities include:

- Answering calls, assisting customers with new and existing reservations

- Dealing with questions, complaints and other issues in a professional and courteous manner

- Helping customers resolve technical issues with the website and on their mobile devices

Applicants for this position must have:

- A high school diploma or equivalent

- The ability to use changing technologies and applications

- Authorization to work in the United States

- Fluency in Spanish (a plus)

- A dedicated phone line

- A hard-wired, high-speed internet connection

Benefits include:

- Health insurance, including medical, dental and vision

- 401(k) retirement plans

- Potential monthly and annual incentive bonuses; most employees just received a bonus of about 7% of their annual pay for 2017.

Apply here for the reservations sales agent job at Alaska Airlines.

Tiffany Wendeln Connors is a staff writer at The Penny Hoarder. Her seat is perpetually in the upright position.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2nht9ta

Elite Daily Wants a Travel Junkie to Fill This Work-From-Home Writing Gig

If you have wanderlust and are looking for travel writer jobs, we may have found the perfect opportunity.

Elite Daily is looking for a writer to cover all aspects of travel — from cool, up-and-coming destinations to the finest hotels and interesting Airbnbs to advice for traveling on a budget.

The part-time, work-from-home position includes work during normal business hours, and three or four shifts per week. The women-focused digital news site is specifically looking for someone with a millennial’s point of view.

If this doesn’t sound like a fit for you, check out The Penny Hoarder Jobs page on Facebook for tons of other opportunities.

How to Become a Travel Writer for Elite Daily

Responsibilities include:

- Writing three or four articles per day

- Pitching original angles and article ideas

Applicants for this position must have:

- Experience writing for a travel website or personal blog

- Ability to cultivate a list of expert sources

- Search engine optimization experience

- Ability to remain flexible while hitting deadlines

- A deep understanding of traveling the world as a millennial

- Ability to discover trending travel topics and deliver clever, authentic angles

- Fluency with images, GIFs, video and other multimedia formats

Apply here for the travel writer job at Elite Daily.

Alex Mahadevan is a data journalist at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2rMNBH1

All You Non-Procrastinators Can Start Filing Your Tax Returns Today

For all the early birds out there itching to put the last of 2017 to bed, the IRS announced it will start accepting tax filings Monday, Jan. 29.

Some tax professionals may have allowed you to complete your taxes even sooner, but they weren’t able to submit your information to the IRS until Jan. 29.

The earliest online tax filers can expect to see their refunds beginning late February, the IRS said.

Those who file paper returns should expect to wait a bit longer. According to the IRS, paper returns won’t begin processing until mid-February. If you expect a return and want it sooner rather than later, file online.

If you are not as excited to deal with accountants and filing software or that box of receipts in the back of your closet, you can put it off a bit longer. The deadline to file this year is Tuesday, April 17.

Desiree Stennett (@desi_stennett) is a staff writer at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2Eqxwbd

How Tax Deductions Work

You've probably heard the phrase "tax deductions" a hundred times. But what does it mean? What are tax deductions and how do they work? And why are tax deductions so important?

Source Business & Money | HowStuffWorks http://ift.tt/2DPjR1u

Source Business & Money | HowStuffWorks http://ift.tt/2DPjR1u

How Tax Deductions Work

You've probably heard the phrase "tax deductions" a hundred times. But what does it mean? What are tax deductions and how do they work? And why are tax deductions so important?

Source Business & Money | HowStuffWorks http://ift.tt/2DPjR1u

Source Business & Money | HowStuffWorks http://ift.tt/2DPjR1u

17 Ridiculous Ways to Make $10,000 You Definitely Haven’t Thought of Yet

The entire cost of tuition at these colleges.

A healthy starting point for investing in your future.

Depending on your location, it could even be a downpayment on a new home for your family to live in or rent out for profit (see #6).

No matter how you slice it, having $10,000 to spend would be nice. But it’s a lot of money to save!

So we’ve gathered 17 weird ways you could earn that extra cash… and how much effort you’d need to put into each to do so.

-

1. Start a Cricket Farm

Not afraid of things that hop, crawl and scuttle?

You could try cricket farming. No, follow me here for a second.

It’s pretty easy to get started, and there’s actually more demand for them than you might think.

You basically just need a fish tank, some egg cartons and dirt to get your habitat set up, and once you start breeding them, they can sell for up to $12 for 250. By the way, the females lay five to 10 eggs… per day.

Check out our full-blown guide to cricket farming to get started. Reptile owners have to feed their pets, and hey, if the business falls through, you’ve got a home-grown source of protein for yourself!

You said you were brave, right?

How many crickets you’d have to sell: 208,333 1/3 crickets. Wonder which third of the last one you’ll get…

-

2.Help a Business Professional Organize Their Day

If you have a knack for organization and communication, there are people who will pay you to help organize their day!

You don’t have to be the busy corporate assistant you see in old movies or TV — now you can be a virtual assistant right from your couch. VA gigs vary in pay, hours and workload.

You might help people and businesses with data entry, social media management, website maintenance, research and customer service. And you could earn up to $60 an hour doing it!

Find virtual assistant jobs through these sites:

How many hours you’d have to work: 167 hours at $60 an hour.

-

3. Test Websites Drunk

Like surfing the Internet? Like drinking?You could take a page out of Richard Littauer’s book and charge website owners to browse their sites… while tipsy.

Why, you may ask?

Well, by testing how navigable a website is while you’re drunk, you can give the creator valuable information about how to make the interface foolproof and the experience so user-friendly.

The idea is a site should be so easy to navigate, someone should be able to use it while drunk. And flask-proof.

Littauer’s a user experience professional and an engineer — what you might call a professional web-surfer. So your mileage in this business may vary… but man, what a sweet gig if you can land it.

How many beers you’d have to drink: To make $10,000, you’d have to test 200 websites at Littauer’s original price of $50. If it takes you three beers to work up a sufficient buzz, that’s 600 beers!

-

4. Tell Companies How You Really Feel About Their Products

If you don’t mind filling out surveys while you’re vegging out on the couch, you could reap rewards for your efforts.

Plus, you get a chance to make your voice heard. It’s like writing a Yelp review… that might win you a free vacation!

Check out Vip Voice. This company will reward you for sharing your opinion to help marketers figure out how to make their products better.

Surveys range in how — and how much — is rewarded, and you’ll have to be part of an eligible demographic.

But if you’re just hanging out in front of Netflix… why not?

How many opinions you’d have to share: If you only made $1 per survey — a lowball estimate — you’d have to tell 10,000 companies how you feel about their goods!

-

6. Drive for Uber

If you find solace on the road and enjoy finding the best route across town, driving with Uber is a great way to do it.

As an Uber contractor, you’re responsible for setting your schedule and motivating yourself to work.

Your earnings will be calculated by adding a base fare, plus time and distance traveled after your pickup, and Uber charges a service fee.

If you want to give it a try here are a few of the things to keep in mind: You must be at least 21 years old, have at least one year of licensed driving experience in the U.S. (three years if you are under 23 years old), have a valid US driver’s license and pass a background check.

Finally, your car must be a four-door, seat at least four passengers (excluding the driver), be registered in-state and be covered by in-state insurance.

Here’s a link to apply with Uber.

6. Open Credit Cards

If you’ve been following The Penny Hoarder for a while, you know we love making our credit cards work for us.Not only do we take advantage of their awesome rewards, we also go in for sweet signup bonuses.

Heck, this guy’s accumulated 1,500 credit cards over the years. He started collecting them after making a bet with a friend… but if he picked the right cards, that could be a lot of extra cash in his pocket!

As long as you’re responsible, cash-back credit cards are an easy way to make some extra money without ever having to think about it.

Here’s an option we like: It’s the Chase Freedom Unlimited card. Its claim to fame? You’ll earn an unlimited 1.5% cash back on all your purchases. Plus, if you spend $500 in your first three months of opening the card (hi, groceries), you’ll pocket a $150 bonus.

There’s no annual fee, and the cash-back rewards don’t expire. We checked Credible’s annual rewards calculator, and it estimates $417 in annual rewards based on our spending habits.* (You can enter your unique spending habits and see what you’d earn, too.)

Get signed up — and 0% intro APR for 15 months — here.

Our advice is to set your rewards card to automatically pay your monthly bills: You’ll earn rewards and keep everything paid on time, without giving either a second thought.

How many points you’d have to earn: 1,000,000. That’s just over $660,000 in groceries, gas, utilities and more.

-

7. Cook Dinner in Your Own Kitchen

Can’t get enough of shows like Chopped or Cutthroat Kitchen? Itching to recreate some of the inventive meals you see chefs whip up?Well, don’t just sit there.

Get in the kitchen, grab a knife, and start cooking! You could make those meals into money with foodshare programs like EatWith.

How many meals you’d have to prepare: If you charged $10 per meal, you’d have to make 1,000 meals to earn $10,000.

-

8. Sell Pine Cones

Yes, seriously.

Yes, seriously.Or K-Cups. Or instruction manuals. Or the cartons your eggs come in. People buy so much random stuff on eBay.

How many pine cones you’d have to sell: 16,667.

-

9. Scare Your Friends and Family

Obsessed with Halloween?If you regularly pull out all the stops on your costume and decorations, you might be a good candidate to start your very own haunted house.

This team of brothers made not just $10,000, but $200,000 — in one month.

Granted, if you had the $200,000 startup cost handy, you might not be reading this post. But if you do, it’s a scary smart way to double your money.

How many people you’d have to scare: 400. Totally doable. You might even have more Facebook friends than that!

-

10. Shovel Your Driveway

Hurry, before winter’s out!

Although you may not have quite as much supply as Kyle Waring did in the famous Boston snowstorm of 2015, it turns out people in sunny locales will actually buy boxes of snow.

Because it’s exotic or they’re masochists or something.

How many boxes of snow you’d have to sell: 112 ? six-pound boxes — or 500 ½ 16.9-ouncers!

-

11. Pour Drinks

If you can open a bottle and your spill rate is less than, say, 15%, you can land a sweet gig as a brand ambassador (read: the smiling girl pouring the samples of Malibu coconut rum at the liquor store).

One of our writers earned between $20-$30 per hour for this kind of work (and wrote us a sweet article about it, along with 20 other ways to make money at the bar). Not bad!

How many shots you’d have to pour: Say you do one a minute. To get to $10,000, you’d have to pour 24,000 shots and make $25 an hour!

-

12. Sell Your Poop

No, that’s not a typo.In fact, some people earn up to $13,000 a year for their… deposits.

There is one catch: You have to live in the vicinity of Medford, Massachusetts, where OpenBiome uses the poop to help physicians around the country treat infections of a nasty bacterial infection.

And you also have to be OK with the fact you’re selling your poop.

How many “samples” you’d have to provide: 250. Hope you’re regular!

-

13. Find a Red Paperclip

I mean, it worked for Montreal’sKyle MacDonald.Although he was never handed $10,000 in cash, he was able to barter his way up from a humble red paper clip until he owned a house.

Significant stops along the way included a snowmobile, a recording-studio contract and an afternoon hanging out with Alice Cooper.

But he traded all of these items until he was offered a home in Kipling, Saskatchewan. His home is almost definitely worth more than $10,000.

How’s that for a weird way to make money?

How many red paperclips you’d need: if you’re as lucky as MacDonald, just one!

-

14. Give Fluffy a Massage

Your faithful companion needs spa days, too.If you adore animals and have strong hands, consider becoming a pet massage therapist. You could earn up to $120 an hour

How many pets you’d need to massage: 286 half-hour pet massages at $35 each.

-

15. Play Video Games

Yep, it’s actually possible.But you have to really like video games. I’m not talking about your Candy Crush “obsession.”

Team Liquid is a group of five LA men who play League of Legends for a living. They each make more than $60,000 a year.

How many hours you’d need to play: A lot.

To keep on top of their game — literally — the men play up to 14 hours per day… and they had to invest the time to get that good in the first place.

-

16. Get in Shape

Picture this: You step on the scale and finally see your goal weight.Congratulations! But it gets even better.

You’re about to receive a generous check to spend on a celebratory dress in your new size, stock up on household necessities, or to wisely stick into savings — all just for losing weight!

It’s not a fantasy. If you wager on your own commitment with HealthyWage, this could very well happen for you… if you stick to your guns and lose the weight.

It’s simple. Sign up for HealthyWage, and then define a goal weight and the amount of time you’ll give yourself to achieve it. Place a monetary bet on yourself ranging from $20 to $500 a month.

Depending on how much you have to lose, how long you give yourself to do it and how much money you put on the table, you could win up to $10,000!

How many pounds you’d need to lose: This will vary based on your wager. Check out their calculator to find out!

-

17. Share Stories About Your Kids on Scary Mommy

If you’ve got kids, you’ve got automatic story generators.From pregnancy fashion choices to dealing with finding your tween daughter’s dating profile, there’s lots to say about parenthood. And on Scary Mommy, it’s “real talk” only — no sanitized, TV-commercial family frolicking in a white-picket-fenced yard.

As long as you have a way with words, you can generate some cash off those face-palm parenting snafus. Here are eight parenting magazines and blogs that pay contributors, averaging about $100 per submission.

How many stories you’d have to share: 100. Good thing your kid’s full of antics — and young…

*Annual Rewards amounts will change based on the amounts you enter. The monthly spending category names and definitions may vary among issuers, and categories may not align one-to-one.

The information for the Chase Freedom Unlimited card has been collected independently by The Penny Hoarder. Opinions expressed here are the author’s alone, not those of the credit card issuer, and have not been reviewed, approved or otherwise endorsed by the credit card issuer. The Penny Hoarder is a partner of Credible.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2BCZfni

The Ultimate Guide to Generation Z Marketing

Businesses need to look toward the future to survive and thrive.

I’m sure you’ve got an effective strategy in place that targets Millennials or Baby Boomers.

But it’s time to shift your focus to a younger generation.

The term Generation Z describes people born after Millennials.

They may also be referred to as:

- Post-Millennials

- Homeland Generation

- iGeneration

Although there isn’t an exact date range, it typically refers to anyone born after the mid to late 1990s.

That means the oldest members of this generation are in college or just graduating.

The reason why this information is so important is because they are starting to enter the workforce.

With a steady annual salary, Gen Z will now have more buying power.

Extra money in their pockets means marketing experts need to target this group.

There’s a big opportunity here for increased and sustainable growth for your company, regardless of the industry.

That’s why Generation Z marketing made my list of the top marketing trends for 2018.

If you’ve never targeted Gen Z before and you’re not sure how to get started, I can help you out.

I’ve used research-backed data to identify some of the top characteristics and habits of this generation.

I’ll also explain in detail how you can use this information to your advantage as a marketer.

Here’s what you need to know.

Understand the key differences between Generation Z and Millennials

First, you need to be able to distinguish the difference between Gen Z and Millennials.

While on the surface these two groups may have some similarities, they needed to be targeted differently from a marketing perspective.

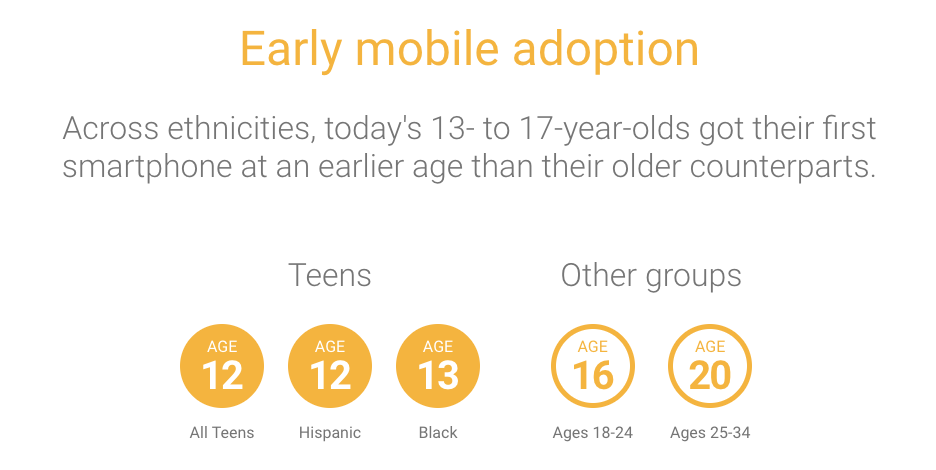

For example, look at how much younger an average Gen Z person was when they got their first smartphone compared to Millennials:

It’s no secret that our world is trending in a mobile direction. Marketers need to accommodate the needs of mobile users.

But Gen Z are the first group to have a smartphone throughout their entire teenage years.

This means they are reliant on these devices more than anyone else, including Millennials.

Generation Z are impatient, and their attention span reflects this.

The average attention span of a Millennial is 12 seconds, but it’s only 8 seconds for Gen Z.

That’s why they use more digital platforms simultaneously.

Millennials typically use three screens at the same time, while generation Z bounces between five screens at the same time.

Gen Z also doesn’t care about customer loyalty programs the same way Millennials do.

I’ll go into greater detail about this concept later on.

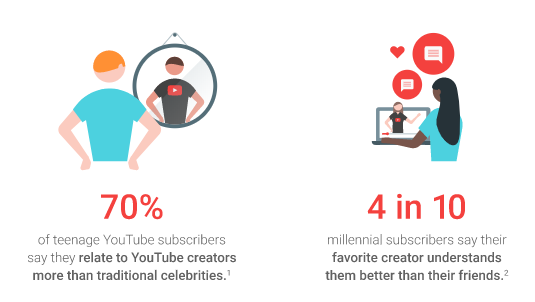

Generation Z also embraces influencer marketing more than Millennials do:

Their engagement with YouTube creators shows how much they value the opinions of regular people as opposed to celebrities.

Your company may want to consider working with more micro-influencers on social media to promote your brand.

Learn how to market your business on Snapchat

If you want to target Gen Z, you can’t afford to ignore Snapchat anymore.

About 71% of Gen Z use Snapchat on a daily basis.

Furthermore, 51% of this group use it about 11 times per day.

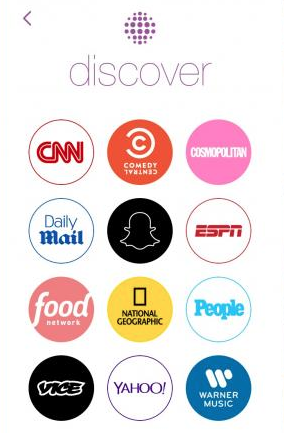

Take a look at some of the top companies that promote sponsored content on Snapchat’s discover page:

I’m sure you recognize these logos.

The fact that these major companies have already identified and adapted to this trend should show you how the market has shifted to this platform.

You can use Snapchat for brand exposure.

As we saw earlier, Gen Z don’t have a long attention span.

Just seeing your company’s logo could be enough to remind them of your brand.

In addition to using sponsored ads, your company should also have an account.

Add pictures and videos to your story on a daily basis.

Here’s an example.

Sour Patch Kids came up with a Snapchat campaign after partnering with Logan Paul, a YouTube personality.

The campaign delivered:

- 120,000 new followers

- 26,000 screenshots

- 583,000 impressions on the first day

- 6.8 million impressions for the last story of the week

Once you gain those initial followers, continue to promote your brand using Snapchat as a platform.

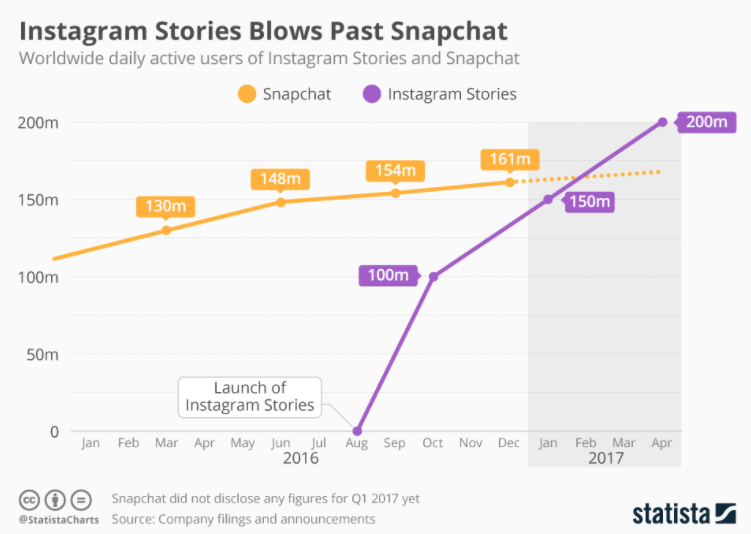

Use Instagram stories

One of the reasons why Instagram stories are so popular is because of their similarity to Snapchat.

Instagram realized how successful the idea of “disappearing content” was and added it to their platform.

You can add photos and videos to your Instagram story, and they will disappear after 24 hours.

In less than two years, Instagram stories have blown Snapchat out of the water:

Use your Instagram story to share exclusive content with your followers.

Even if you’re not posting a picture or video on your Instagram profile each day, you should at least be utilizing your story.

As I said earlier, Gen Z love micro-influencers.

Try to get those influencers to take over your account.

Alternatively, you can ask them to promote your brand on their personal stories.

Take your followers behind the scenes of your daily operations.

Showcase your production facilities, and introduce your staff.

This connects with people and shows them the human side of your company.

The marketing opportunities are endless with Instagram stories.

You just need to get creative and think outside the box to gain exposure.

Encourage entrepreneurship

Part of being a great marketer means you need to understand how your target audience thinks.

Generation Z have an entrepreneurial spirit.

In fact, 72% of teens in the United States say they want to start their own business one day.

If this group follows through with their goals, it will drastically change the future of our country’s workforce.

That’s because 61% of this group want to start a business directly out of college.

But Gen Z don’t value education as much as other generations do.

Only 64% of Generation Z plan to pursue a college degree compared to 71% of Millennials—a seven-percent difference.

It’s possible they don’t think they need college education to be successful.

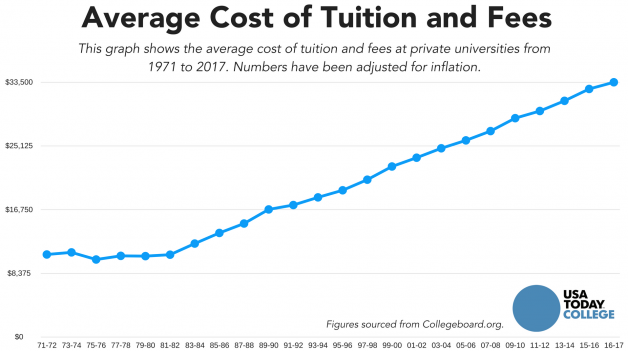

This might be based on the rising cost of college tuition.

These numbers are rising higher than the country’s inflation rate.

The high costs could have an impact on Gen Z’s attitude towards higher education.

But with so many resources available on the Internet, Gen Z feel like they don’t need college to be successful or start their own business.

What does this mean for your company?

Try to come up with clever ways to engage those entrepreneurial minds.

Consider partnering with successful entrepreneurs who didn’t go to college as brand ambassadors for your company.

You could also try to create a value proposition that speaks to young entrepreneurs.

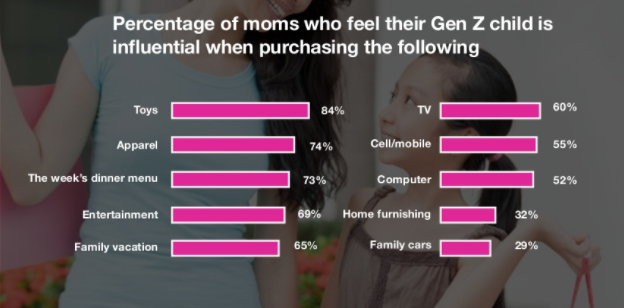

Generation Z has an influence on purchases their parents make

Market products and services to Generation Z even if they are not consumed by teens.

Here’s a graph to show you what I mean:

Most marketers wouldn’t think to pitch a family vacation, cell phone, or car to an 11-year-old.

But research shows that Generation Z has an influence on household purchases.

This generation is resourceful.

They may be more likely to research products and read reviews than their parents.

Just because they may not have the personal funds or resources to buy home furnishings or a plane ticket doesn’t mean your company can’t target these kids.

Their opinions may be the deciding factor between a purchase from your company or your competitor.

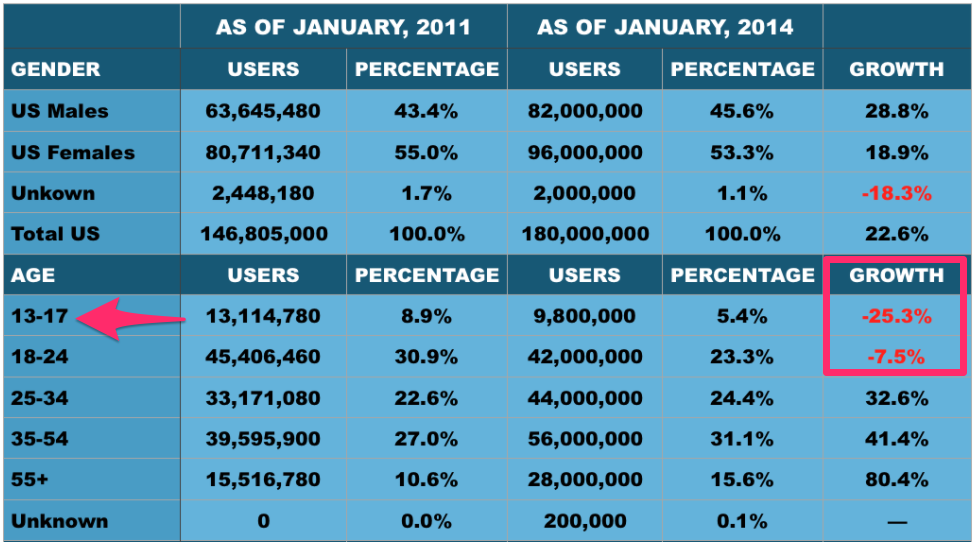

Facebook shouldn’t be your top priority

Facebook always tends to be the king in terms of social media marketing platforms.

But Generation Z don’t feel the same way about Facebook as other generations.

In fact, Facebook lost over 25% of users between the ages of 13 and 17 on their platform over a three-year stretch.

Don’t get me wrong.

I’m not saying you need to abandon your Facebook marketing strategy.

As you can see from this graph, the growth rate is rising for every other age group.

There’s still a ton of users out there for you.

But with that said, this shouldn’t be your primary strategy if you’re targeting just Generation Z.

Campaigns solely designed for Gen Z should be used on other social media platforms such as Snapchat, Instagram, and YouTube.

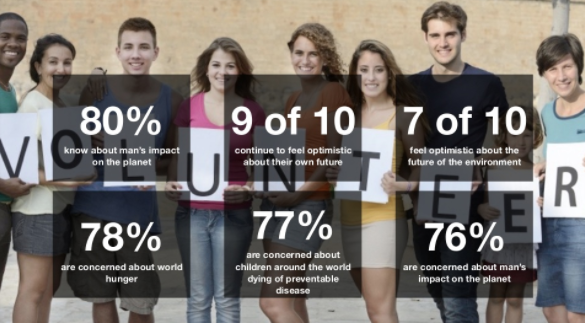

Generation Z want to make a positive impact on the world

Your company needs to be conscious of the environment, planet, and society.

According to a recent study, 60% of Gen Z want to positively change the future of our world.

Only 39% of Millennials feel the same way.

Furthermore, about 25% of teens today are already involved in volunteer work.

This is great news for the future of our world.

It seems like every time you turn on the TV or read the paper, all you hear is negative stories.

But Gen Z want to make a difference:

Take a look at these numbers.

To stay engaged with this group, your company needs to do its part as well.

Talk about any positive impact you are making in the community.

Are you working with charities?

Do your employees volunteer?

Come up with a mission that contributes to the greater good of the society.

Embrace it.

TOMS Shoes is a great example of this marketing strategy.

For every pair of shoes bought on their website, TOMS donates a pair of shoes to a child in need.

It’s a powerful campaign that speaks to generations who care about the future of our world.

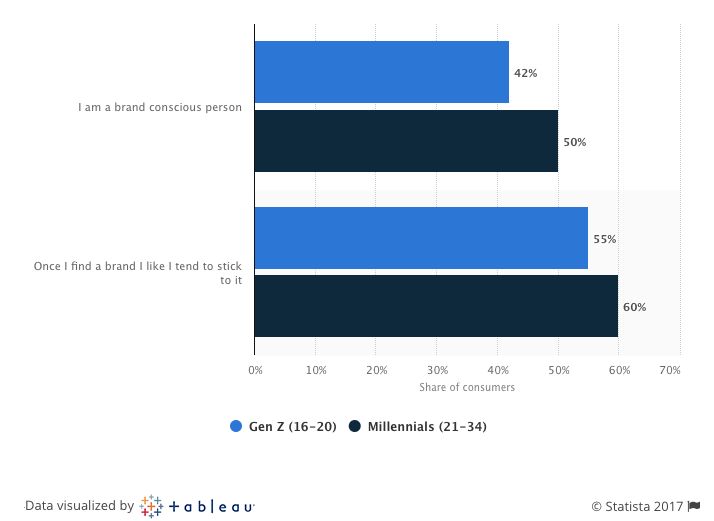

Quality is more important than brand loyalty

Does this sound like your current marketing strategy?

Acquire new customers for as cheap as possible and retain them through customer loyalty programs.

It’s not a bad idea, and it’s probably been working for a while.

Once a customer becomes loyal to your brand, they’ll continue to support you for years to come.

They may start buying different product lines within your company, spend more money with each purchase, and even be willing to pay for more expensive products.

But you may not have as much luck with this strategy if you’re targeting Generation Z.

Look at how Gen Z view brand loyalty compared to Millennials:

This means you may have to put more effort into your current retention strategies for Gen Z.

Find ways to make them loyal.

There’s another way to interpret this information.

You could save your marketing dollars and not dump money on loyalty reward programs for Gen Z.

This decision is totally up to you.

It depends on your current retention and acquisition rates.

One of the best ways to retain Gen Z customers is through meaningful interactions.

A recent study showed that 44% of Gen Z are interested in contributing ideas to products and designs for their favorite brands.

Take advantage of this.

Use surveys, interviews, and focus groups with your customers to come up with new ideas.

If your customers contributed to the design, they are more likely to feel a connection with your brand and stay loyal.

Another statistic of interest is that 61% of Generation Z consumers are drawn to new brands.

Startup companies need to start targeting this generation right away in an effort to build brand loyalty.

Upload content to your YouTube channel

Generation Z love YouTube.

I discussed this earlier when I talked about micro-influencers.

I also showed you the success that Sour Patch Kids had using a YouTube creator in one of their marketing campaigns.

On average, Gen Z watch two to four hours of YouTube content each day.

They enjoy this much more than cable TV, which only accounts for about 30 minutes of their daily video consumption.

So if you’re relying on TV commercials to reach Gen Z, you’re wasting your money.

Instead, you need to increase your YouTube presence.

I love using YouTube as a promotional channel because it’s so easy to repurpose those videos.

It’s easy to add YouTube videos to your website or emails and incorporate them into your overall content marketing strategy.

Focus on their love of video games

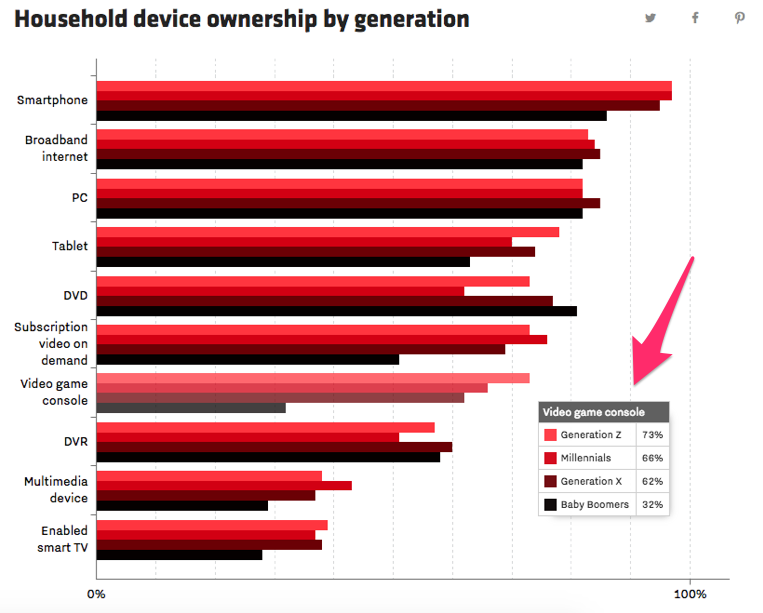

Sixty-six percent of kids between the ages of 6 and 11 say that gaming is their primary source of entertainment.

Furthermore, Gen Z own more video game systems than every other generation.

But your company doesn’t make video games.

You may not even be in the technology or entertainment industry.

What does this mean for you?

Get creative.

That’s the fun part of marketing.

Come up with clever ways to use this information to your advantage.

For example, you could try to use product placement in video games.

You could also partner with specific games or gaming systems.

Sponsor an event or release of a new game.

If you sell certain electronics, advertise them for video game usage.

Things like microphones, headsets, routers, Wi-Fi extenders are all important to young gamers.

Conclusion

Right now, Generation Z are still an untapped market.

While companies have started targeting this group, there is still a huge opportunity for your brand to get a piece of the action.

You just need to understand how this new generation behaves, thinks, and consumes.

Don’t approach them the same way you have Millennials. As we saw, these two groups are different.

Use Snapchat and Instagram story to promote your brand.

Recognize that Generation Z value entrepreneurship and want to have a positive impact on the world.

They even have an influence over purchases made by their parents.

Gen Z are less active on Facebook, and they care about the quality of interactions with companies more than brand loyalty.

They love watching content on YouTube and playing video games.

If you follow this guide, your company can benefit from a new income stream.

What marketing platforms are you using to target Generation Z?

Source Quick Sprout http://ift.tt/2GroWep

Questions About Rice Cookers, Government Shutdown, Toys R Us, Lasagna and More!

What’s inside? Here are the questions answered in today’s reader mailbag, boiled down to summaries of five or fewer words. Click on the number to jump straight down to the question.

1. Handling increase in income

2. Comparing pre-tax and post-tax contributions

3. Putting a windfall into stocks

4. Filing jointly or separately?

5. Retirement savings in up market

6. Low end rice cooker recommendation

7. Tired of fear, uncertainty & doubt

8. Cheap version good enough?

9. Going out of business sale?

10. Training my replacement at work

11. Oven ready lasagna noodles

12. Government shutdown panic

One of the most important things that I’ve found for my own work is the use of ambient noise and ambient music to help me focus on what I’m doing. It’s really amazing how much of a difference that it makes in terms of keeping me focused.

I’ve become so used to using ambient noise and music over the last few years that I began to actually doubt how much of an impact that it had, so as an experiment, I went for a week without using it. What I found was that I felt like I was working at half speed on every intellectual or creative task I was doing, from reading and learning to writing and brainstorming and outlining. I got about 40% less work done over the course of an entire week from working in silence or listening to pop music or podcasts versus listening to ambient noise or ambient music. Seriously. I measured it by finished word count, potential ideas produced, articles read, and a few other ways that I track things. I just worked at a much slower pace without it.

I use two different tools for ambient noise and music, and I alternate between the two to mix it up. For ambient noise, I just turn on this Youtube video, which consists of ten hours of the audio of an icebreaker ship. When I want ambient music, I use Brain.fm, which I also sometimes use while meditating, too.

I hope these resources help you out when you’re trying to study or do creative work! They certainly help me out!

On with this week’s questions!

Q1: Handling increase in income

With the implementation of the new tax law, between my husband and I we are bringing home an extra $200/month. Woo hoo! We both have WI pension plans. I have a pension from the state of MN as well, a 403b which I currently contribute 3%. I plan on taking my state raise this year (4% increase) and applying it all towards my 403b so I will be contributing 7% total. My husband is planning on opening a deferred comp plan within the next month as well. We have no credit card debt. We have a mortgage, 2 car loans ( one is almost paid off), and about $13,000 in student loans. We are 35 and have one kid and no plans for more children. Should we take this extra money and contribute more for retirement or use it pay down debt?

– Dana

If you have any high interest debt, I’d pay that off first and foremost.

Once that’s out of the way, I would sit down and think about what your plans are and how stable your life is right now. Are your jobs strong and stable? Are you spending less than you earn even as you pay down those remaining debts? If so, I’d put it into retirement.

If you’re struggling to make ends meet as it is, then I’d lean more toward using that money to get rid of a few of the debts for now. Treat them as extra debt payments and aim for the one with the highest interest rate.

Q2: Comparing pre-tax and post-tax contributions

Hey Trent, was hoping to get your opinion on my way of looking at retirement savings percentages. I believe that the most common montra out there now is to save at least 10-15% of your income towards retirement. If you are using a Traditional 401K or IRA that is a fairly simple calculation because it’s based on pre-tax dollars. So essentially if you make $50K per years, then 10% towards a Traditional account would be $5K. But my question is what if you are contributing to a Roth IRA or 401K where you are using after-tax dollars to fund the account. Do you look at your contributions as a percent of your gross salary like you do with a Traditional account or do you look at your contributions based on actual taxable/take home dollars? Same $50K salary with 20% taxes removed means take home pay is $40K. I’m maxing out a Roth with $5500 a year. Am I contributing 11% based on gross or am I contributing 14% based on after-tax?

– Jim

In general, the safe way to calculate this is to use gross income and gross contributions. You’ve already paid the taxes on Roth contributions and won’t have to pay them later, so that is, in effect, retirement savings as well.

However, that means you’re looking at ALL contributions through the filter of gross income. This means that you calculate it as gross income, but you also count the taxes you paid on any after-tax contributions you paid. So, you’d add the $5,500 to the 401(k) contributions plus the income tax you paid on that $5,500.

Again, all of this is just for guidance. If you’re at 14% one way or 11% another way, you’re fine. I think the goal should be that you’re saving at least 10% no matter how you calculate it and you’re doing that.

Q3: Putting a windfall into stocks

Normally, we put money into our Vanguard account (all stock index) on paydays when we have extra to deposit, regardless of what the market is doing. However, we happen to have a pretty large lump sum to put in right now (money set aside for something it no longer needs to be set aside for), and I’m thinking about waiting until the inevitable recession after all of these constant record highs the last few years.

I’m normally a pretty anti-“play the market” guy, for many of the same reasons you reiterate frequently, but in this case it makes sense to me because this isn’t money I’m going to be taking out and putting in constantly, it’s going to be staying in for the long term; I won’t be worried about hitting right on a true minimum, I just feel a bit odd dumping this much in at once when I can be about 99.9% sure the market will fall noticeably past this point in the future. I don’t necessarily need to wait until it hits a true minimum anyway, Normal bi-weekly/monthly paycheck deposits will continue to dollar-cost-average by going in immediately as normal. Thoughts?

– Donald

I think the absolute first thing you should do is sit down and decide what your goal is with this money. What are you intending to do with it?

If this is purely a “when something comes along” type of fund, it should be in something very low risk, because that “something” could come along tomorrow.

If you have another kind of goal that you’re thinking of, whether it’s retirement or something else, you should invest according to how far out it is. If it’s more than ten years out, you should put it in stocks no matter how the stock market is doing.

If your goal is less than ten years out but not in the super near future, then I’d probably still keep it in something pretty secure, but there’s an argument to be made here about splitting it up a little between safe investments and aggressive ones.

To summarize, figure out what you’re going to be doing with it first. If you’re certain that it’s for something that’s more than ten years out, put it in the market regardless of what it’s doing. If you’re very unsure or using for something that’s less than ten years out, keep it in something safe.

Q4: Filing jointly or separately?

My husband and I were married in September 2017. How do we figure out if we should file our taxes this year as married filing separately or married? Also how do we both go about updating our W-4 withholding, considering each other as dependents?

– Janelle

Without a full picture of your finances, I can’t give you a good answer. What I can tell you to do is either get a good software package for calculating your taxes – my personal preference is TurboTax, but most well-known packages are fine – and let it figure it out for you.

The reason for a software package is that it will automatically do the math on both methods of filing and tell you the right way to do it that’s both legal and saves you the most money, which is the way you want to file.

If you don’t fully trust a tax software package, then you should take your taxes to a tax preparer. Doing them by hand is very time consuming, especially when you’re probably going to want to prepare it both ways to see which has the best results.

Q5: Retirement savings in up market

I retired in 2010 with a nice healthy severance package and about $400K in my 401(k) plan. I was 63 then and 70 now. I have lived off the severance package and proceeds from home sale since then without touching the 401(k) and left it almost entirely in stocks. I was hoping to live out my life off of the savings account and still have 5 years more or so.

Right now I don’t know what to do. My 401(k) is approaching $1 million. I spend about $30K per year and I have about $145K in savings. My 401(k) is very aggressively invested almost all stocks. I am 70 years old. Should I make my 401(k) less aggressive or leave it there?

I am a widow with one child who is just wonderful and I want to leave all assets to him, his wife, and their kids.

– Maryanne

My thinking is that any portion of your 401(k) that you think you may need in the next ten years should be in something conservative, and everything beyond that should be in something aggressive. Assume you’re living forever.

So, what should you do? If I were you, I would move about $150K of the 401(k) into something much safer (that’s five years of living expenses, plus the five years you have in savings, adding up to ten total years of living expenses in something safe), like bonds or cash, and let the rest sit. Each year, move about a year’s worth of living expenses from aggressive investments into something safer. Social Security will definitely help here, but I’m not 100% sure what kinds of benefits you receive from it, so I’m ignoring it. You’re probably safe moving a little less into conservative investments, but this plan will keep you quite safe.

Ignore what the market is doing. The market will go up sometimes and it will go down sometimes. It is very difficult to tell where it is going in the future, especially in a timeframe longer than ten years.

I’m assuming, of course, that any and all dividends from your aggressive investments are being rolled right into more of those investments. I’d leave that in place, too.

You will have to live to an absurdly old age for this plan to ever run dry unless the US economy completely falls apart in an unprecedented way. My belief is that the best thing you can do for your son is to make sure you are never a financial burden to him and his family, and this plan should essentially insure that.

Q6: Low end rice cooker recommendation

I have been following your recent suggestions and watching the local Goodwill and SA for a rice cooker but I haven’t found one yet. I love eating rice but rarely make it because it’s not convenient in my life but a rice cooker would really help with that. I have a $50 Amazon gift card I received for Christmas and have decided to just buy a new one. What do you recommend in that price range?

– Kathleen

So, confession here: we are lucky enough to have an amazing Zojirushi rice cooker, one that does an incredible job on rice of all kinds and oatmeal and we highly recommend, but it is significantly outside of your budget. It’s a few years old and I can’t find an exact match for it on Amazon (it appears to be an older model). Before that, we literally used a Salvation Army rice cooker – I think it was a Panasonic.

Since I don’t have specific experience with rice cookers in your range, I went and looked at a few of the resources that I trust regarding such things – Consumer Reports and Cooks Illustrated. I checked out some of their recommended models, particularly ones they both liked, and sought one that comes in below $50.

My recommendation, then, is the Aroma Housewares ARC-914SBD 8-cup rice cooker. It seems to get good reviews all around and is a nice size for a single person or even a small family. Plus, you’ll still have $20 on that Amazon gift card!

Q7: Tired of fear, uncertainty & doubt

I am getting really tired of reading articles about people panicking because the stock market is “too high.” It’s always the same thing! It’s been going up for X years and that’s just too long! And the advice is either just stay the course or ridiculous panic! I think it’s all politically motivated anyway. Please don’t include questions like this in your mailbag.

– Jerry

Jerry, the reality is that a lot of the mailbag questions I get right now have to do with how high the stock market is. I actually filter out quite a lot of these types of questions because they are kind of repetitious, but if I don’t have one in my last mailbag or two, I’ll get a good half-dozen questions about it in the ensuing week. I try to answer what people ask.

Besides, I think the current stock market is a great illustration of the concern that many people have about investing in the stock market. It’s a scary place. It’s a place where you can ride a run of several years of 15% gains only to see the bottom suddenly fall out like what happened in 2008. That’s scary to a lot of people.

I don’t advocate for market timing, but I do advocate that people not put their money into the stock market if they can’t emotionally handle that kind of a drop and if their investment isn’t a long term investment. A person in their thirties should absolutely have a lot of their retirement in the stock market because it’s a long term investment, for example, but a person in their sixties, particularly a person who is skittish, might not want to do the same depending on their specific situation.

In other words, the decision about whether to invest in stocks shouldn’t have anything to do with the current market, but with the timeframe of your investment and your personal risk tolerance (because poor risk tolerance can lead right to locking in a bunch of losses). This is a moment in time where that point can really be hammered home, and a lot of people are thinking about it.

Q8: Cheap version good enough?

When do you know if the cheap version of something is “good enough”? A friend had a horror story recently about how their cheap baking dish exploded in the oven ruining dinner and making for a big cleanup. That wouldn’t have happened with a good baking dish. But if you buy everything high-end you go bankrupt. How do you know what to do?

– Olivia

For me, if it’s something inexpensive with a relatively low risk involved if it breaks, then I try the cheap version first. I use store brand versions of a lot of household supplies, for example.

If it’s something expensive or something that could cause a real problem if it breaks, I usually invest the time to do some real homework on it. I look at Consumer Reports as my first line of defense and often dig deeper into reputable publications within that specific niche as well. This usually means a trip to the library for me – I almost always have a thing or two to look up in their magazines each time I visit the library!

As a general rule, I tend to trust Consumer Reports‘ “best buys” for a particular product. I’ve found that those items almost always do the job above and beyond what I need with little risk involved, and they tend to save quite a bit off of the highest end items.

Q9: Going out of business sale?

There is a Toys R Us about 1/4 mile from my apartment that’s going out of business. How can I take advantage of this and either save some money or maybe make a little?

– David

Making money off of a Toys R Us going out of business is tricky unless you know the value of toys in your head or are willing to invest a lot of time in there wandering around checking eBay values. Buying random toys at a 30% off rate isn’t going to be a big money maker.

Having said that, a toy store going out of business can save you money in a few easy ways. It might be a great time to do a little bit of super early holiday or birthday shopping for a child in your life. If you have children or nieces or nephews or grandchildren, especially young ones, this can be a great opportunity to snag some gifts for them. (Just be sure to let their parents know what you’ve snagged so you don’t end up with a duplicate non-returnable item.)

Another approach is to talk to any parents/grandparents/aunts/uncles/guardians in your life who may actually have a use for this sale and offer to be their “mule” as a nice favor or for a few bucks. They can give you a list of things to look for and you can go in there and buy them at a nice discount to save them some money. If nothing else, this would be a great appreciated help for some of the busy parents you know.

Q10: Training my replacement at work

My company is downsizing and my position is disappearing. I’m supposed to spend my last three weeks training this guy who is supposed to now do my job and frankly I don’t [care]. What can they do to me if I just show up and sit there and do job searches instead of helping him?

– Charlie

They’ll probably still pay you, but any recommendation you get from them will probably be a bad one, which will make it harder to find your next job. If you’re planning to stay in this field, the reputation hit you’ll take from doing this will probably cost you far more than you’ll gain.

A better approach here is to do your best to train this guy. It’s not his fault he’s in this boat with you. In fact, he’s probably disgruntled that he’s being handed these extra tasks and isn’t thrilled with this either. Rather than hanging this guy out to dry, commiserate with him. Do what you can to get him into a good spot when you’re gone.

Not only will this make you look really good in this person’s eyes, it will also reflect positively in any recommendations you get from the company and might even open doors for you. You may just find that if you’re doing this well, they may end up finding another position for you or else help you find a new one. If nothing else, you won’t have burned bridges here and you’ll definitely have at least one career ally moving forward.

Q11: Oven ready lasagna noodles

I love making lasagna but it is such a time consumer that I don’t make it very often. I thought the no boil noodles would help so I tried them and it made everything gummy. Is there some trick to making them work? Thought you might know as a kitchen efficiency whiz!

– Ella

I wouldn’t remotely call myself a kitchen efficiency whiz, but I do enjoy cooking at home.

I have tried no-boil noodles myself in lasagna and I generally find them to be gummy, too. The rest of my family seems to like them just fine, but I vastly prefer the texture of regular noodles.

Now, I have found that they get a lot better if you just partially boil the no-bake noodles. I did this on accident once and boiled them for just a couple of minutes before realizing what I had done and then decided to use them anyway, and they were just fine. At that point, though, why not just use regular noodles?

I’ve also tried just cooking the lasagna using ordinary noodles that are completely uncooked and just smothering them in sauce on both sides. This seems to work reasonably well – I like the texture better than “no-boil” noodles, anyway. You might want to try this. Just make your normal lasagna, put the dry noodles on top of a layer of sauce, then do another sauce layer right on top of any dry noodle layer. Bake as normal, because the boiling sauce will cook the noodles right inside the pan.

Q12: Government shutdown panic

I currently work for the DoE as a technical assistant. I make a very nice salary that should be more than enough, but when the government shutdown happened I took a look at my money and realized I was going to hit a major problem if things didn’t get back up and running in like two or three days. That’s obviously bad and it set me into kind of a panic. I started reading about money and searching around and came to your site. I don’t know what to do next or where to start.

– David

So, I received three different variations on this question. It appears as though the government shutdown and the specter of more of them in the near future shocked a few people into thinking about their finances.

So, where can you start? The absolute first thing you should do is start building an emergency fund. An emergency fund is simply money stowed aside in a savings account somewhere that you don’t touch until there’s an outright emergency – like, say, a prolonged government shutdown. The easiest way to build this is to get an online savings account from a reputable online bank like Ally and set it up so it does an automatic transfer each week from your main checking account into this emergency fund. $20 is a good number to start with; a little more is nice. Then, just forget about that account entirely until an emergency happens.

That’s a great first step, but it’s just that – a first step. The most important thing that people should be doing with their finances is a much bigger and, often, much harder step. You need to spend less than you earn. Every month, every year. The only time that you shouldn’t be spending less than you earn is when an emergency occurs, at which point your emergency fund is there to help.

If you’re doing this, your credit card balances will no longer be going up – they’ll be going down. As will your other debts. Eventually, they’ll go away, at which point it becomes trivially easy to start saving for big long term goals like retirement.

How do you mechanically do that, though? The most important step in that process is to sit down and really look at your spending. Where is that money going? Get out your most recent credit card bills and bank statements and start looking through them. How many of those transactions do you just not remember at all? Or, you see it and you sort of remember it, but not in any clear memorable way? Most of that spending is a giant waste. You’ve essentially tossed money away on completely forgettable things and because of that found yourself utterly panicking right now. That’s a very, very bad trade.

So, if you’re seeing a lot of transactions where you don’t even remember where the money went or it seems completely dumb in retrospect, start intentionally cutting out most of that stuff. Do you really need to stop at the convenience store? Will you really care about this purchase two days from now? Start asking yourself that about everything you buy.

There are lots and lots and lots of steps you can take to start mopping things up. That’s why the personal finance section of the library and of your local bookstore is loaded with books on getting your money straight. Go to the library and pick out one that speaks to you and check it out. The core advice in most of them is pretty good. If one isn’t clicking, go back and try another one. The one that clicked for me was Your Money or Your Life by Joe Dominguez and Vicki Robin. Avoid any book that talks about unrealistic-sounding results, like “You Too Can Be a Millionaire By Age 30!”

That should be enough to get you started.

Got any questions? The best way to ask is to follow me on Facebook and ask questions directly there. I’ll attempt to answer them in a future mailbag (which, by way of full disclosure, may also get re-posted on other websites that pick up my blog). However, I do receive many, many questions per week, so I may not necessarily be able to answer yours.

The post Questions About Rice Cookers, Government Shutdown, Toys R Us, Lasagna and More! appeared first on The Simple Dollar.

Source The Simple Dollar http://ift.tt/2DYx5bS

3 Smart Things to Try Before You Use Your Credit Card for a Medical Bill

When Tina Ortega started experiencing mouth pain, she headed straight to a dentist. The Mississippi resident ended up needing a root canal. Even with insurance, she had pay $500 out of pocket.

She and her husband didn’t have the money — Ortega was without a job and has children, so funds were tight. To pay the bill, she opened a CareCredit account and took advantage of its deferred-interest period.

She was confident she would pay it off before incurring any interest, so she thought it was the best option for her at the time.

“People who say not to use credit cards –– they don’t understand because they’ve never been there,” she said. “Especially if they’ve never had to live without insurance. You have to do what you have to do.”

Medical Bills Are a Serious Source of Worry

In the HealthFirst Financial Patient Survey, conducted in 2017 by business intelligence firm ORC International, 1,011 adults answered questions about health care pricing and payment options.

The findings? Of the respondents, 42% said they “are very concerned or concerned about their ability to pay out-of-pocket medical bills in the next two years.” That number jumped to 54% among respondents who make less than $35,000 a year.

And they weren’t just worried about expensive surgeries. About 53% of respondents said they were concerned about their ability to pay a medical bill under $1,000, and 35% worried about whether they could pay a bill under $500.

CareCredit, or any credit card with interest-free or deferred-interest periods, might give peace of mind to customers who know that if a big bill from a doctor’s office comes up, they have a bit of breathing room to pay it back.

But with deferred interest, which is what CareCredit offers, if you don’t pay the balance in full by the time promotional period ends, you’ll be charged all the interest you avoided during that period, plus whatever interest you accumulate on the remaining balance.

Ortega’s interest-free period was for nine months — after that, she would have been charged an annual percentage rate, or APR, of 26.99%. If she hadn’t paid the account in full during the promotional period, she would have been charged all the interest she avoided for nine months.

Ruth Linden, founder and president of Tree of Life Health Advocates, says financing medical bills on a credit card –– including CareCredit –– should be a last resort.

Why? Because once the interest-free period is up, you’ll often pay “exorbitant interest rates.”

“The problem is that many people fully intend to pay off their balance during the interest-free window but life (and other health issues) may intervene,” Linden said.

3 Alternatives to Charging Medical Bills to a Credit Card

If Ortega hadn’t charged the bill, what would her options have been since she didn’t have the funds sitting in her bank account?

Here are a few other alternatives to charging medical bills to a credit card:

-

Ask a Provider for Financial Help

Whether your bill is from a hospital, lab or physician, asking for help can go a long way.

“It can’t hurt, and it might make a huge difference,” Linden said. “Lower-income consumers may be eligible for financial assistance from hospitals and individual providers.”

To start the process, USA.gov recommends contacting your hospital’s patient services department. After you explain your situation, the department will ask you a few questions about your income to determine if you’re eligible for assistance. If you are eligible, part of your bill may be forgiven.

If you don’t qualify, USA.gov says you may be able to set up a payment plan through the hospital.

2. Negotiate the Balance

If your income is too high for the provider to offer a discounted rate, consider negotiating your bill. You can negotiate the balance with the provider and your insurance company.

Wondering where to start? First, contact the provider’s billing department. Tell the representative you’re connected with that you’ll pay a percentage of the balance now if the provider will forgive the rest.

If that sounds intimidating to you, consider looking up average retail prices for hospital procedures. You can use these numbers as a point of reference when negotiating, and they might be to your advantage if your balance is much higher than average.

3. Request Assistance From a Patient or Medical Billing Advocate

Linden said a patient or medical billing advocate can review your bills and the insurance company’s explanation of benefits — if you have health insurance. While reviewing them, the advocate will look for billing errors, such as duplicate charges or charges for services you did not receive, and work on your behalf to correct those errors.

If you don’t have help from a trained professional, you can still find these errors yourself. It’s worth the effort, too — it’s estimated that about 80% of medical bills contain errors.

Take a look at your bill and confirm that all of the items are correct. If a prescription is listed, did you actually get it from your provider, or did you pick it up from your pharmacy? Are there any duplicate charges? If you find errors, be sure to contact the provider’s billing services center immediately.

Meanwhile, consider building an emergency fund to cover future medical bills –– you’ll thank yourself later.

Kelly Anne Smith is an email content specialist at The Penny Hoarder. Catch her on Twitter at @keywordkelly.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2Fsgw4P

الاشتراك في:

التعليقات (Atom)