Every business needs to strive for growth.

This isn’t a secret. However, many business owners hear growth and they jump to customer acquisition strategies, new product launches, and ways to increase their conversion rates.

All of these tactics are great for your company growth. But, they’re not the only way to boost revenue and grow your business.

You can also grow when you make more money with your existing products, services, and conversion rates simply by increasing your average order value.

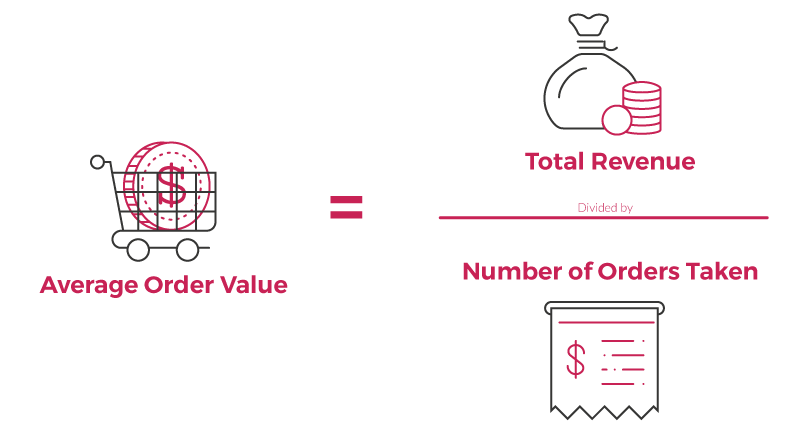

Are you currently tracking this metric? It’s easy to calculate with this formula.

How to calculate your Average Order Value (AOV)

In order to increase your AOV, you need to encourage your customers to spend more in each transaction. Sounds great in theory. We’ll walk you through how to actually accomplish it.

There are tons of ways to get your current customers to spend more each time they shop. One of the best methods for increasing AOV is with product bundling. This marketing tactic employs a combination of upsells, cross-sells, and discounts. It also helps you generate more profit by focusing on your pricing strategy.

Basically, the psychology behind product bundling entices people to spend more with every transaction simply by buying more things at once. As a result, your average order value will rise.

Whether you sell products or services, your company can benefit from a product bundling strategy. But it’s not as simple as lumping any two or three random items together. In fact, that can do more harm than good.

If you’ve never done this before it can be a bit of a challenge to determine which products should be bundled together and how to showcase those options to your customers. So use this guide as a blueprint for increasing your average order value. Here’s what you need to know.

Don’t pair inexpensive items with premium products or services

This is the most common mistake we see when businesses attempt a product bundling strategy for the first time. It makes sense: they’re trying to maximize their profits and someone is buying something cheap, why not try to get them to buy something that’s expensive too.

Product bundling doesn’t mean you should just throw any two or three items together and assume your customers will pay more for them.

Put yourself into the mind of the consumer for a minute here.

For example, let’s say you’re shopping for a new car and your price range is roughly $20,000. If the dealer throws in a free t-shirt and a baseball cap with the purchase of a vehicle, is it going to entice you to buy the car?

Or, on the flip side, let’s say you’re shopping for a t-shirt and a baseball cap with your favorite car company logo on them. Together the two cost about $40. But then, at checkout it’s suggested you buy a car, too. This brings your total to $20,040. Do you do it?

Two items that don’t belong together are not a product bundle. This is especially true if one item is significantly cheaper than the other. But so many brands think two items = a bundle, and it ends up hurting them.

Instead of encouraging your customer to buy more things, a grouping like this actually confuses their initial purchase. Let’s take a closer look.

There’s a study from the Journal of Consumer Research on consumer perception and product bundling called The Presenter’s Paradox.

Here’s what happened. They gave people two options of how to bundle products for prospective customers. The first option was an iPod Touch bundled with a cover. The second option was an iPod Touch bundled with a cover and a free song download. Nearly everyone (92%) chose the second option, which included the free download. However, the study concluded that consumers were willing to pay more money for the first bundle, without the song download.

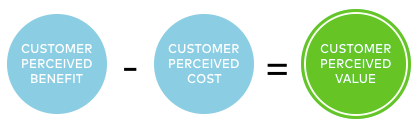

Why? The benefit and cost of that download aren’t enough to enhance the perceived value of the bundle.

In fact, the cheaper item — One song? What am I going to do with one song? — lowers the perceived value of the total package. That’s not what we want to do. Rather than diminish the perceived value of a bundle, we want to increase it. You can charge more for your products by enhancing the perceived value.

A cheap add-on paired with a premium product makes the whole bundle feel less appealing to the consumer.

This Harvard Business Review article discusses a set of similar studies that had the same results. The study showed that consumers were more likely to pay $2,299 for a home gym than they were to pay that very same amount for the same gym was bundled with a workout DVD. Again, that’s because a DVD doesn’t enhance the perceived value. It actually has the opposite effect and lowers that value.

So if you’re currently using a strategy like this, it could be hurting your average order value as opposed to helping you out. You can fix this quickly and easily.

This guide will also you examples of the right types of products and services to bundle.

Emphasize savings

Offering a discount is a great way to make your product bundles more appealing. It’s a very simple strategy.

If a customer buys two or more items together, their total purchase will be cheaper than if they bought each one individually. However, you need to make it obvious that they are saving money. So tell them exactly how much money they can save by buying the bundle.

Here’s a great example of this from Lowe’s.

The product bundle here is a washing machine and a dryer. If customers buy the pair together, they can save $340. The customer might think, That’s getting close to the price as of either the washer or dryer alone! However, people won’t know how good of a deal they’re getting if you don’t tell them.

You shouldn’t be making your customers do the math manually or hunt through your prices. Make it obvious and plaster the savings on your website, just like the example above. In this instance, by bundling the savings together, it’s much more entcicing. The customer isn’t simply saving $170 on each, which doesn’t seem like that much. They’re saving $340, which has a lot more wow factor.

As a result, they will be more likely to buy these together to get the savings.

Bundle items commonly purchased together

Remember the hypothetical scenario earlier: the car bundled with a t-shirt and hat? Those items are not commonly purchased at the same time, and that’s another reason why that bundling strategy won’t work.

You need to figure out what items people will also need when they buy something specific. Refer back to our last example from Lowe’s. If a customer is in the market for a washing machine, there’s a good chance they also need a dryer. Bundling those two items together is a winning strategy. This makes much more sense than bundling a dryer with a dishwasher. Sure, they are both home appliances, but they are completely unrelated to each other.

If your company sells shampoo, you can bundle it with conditioner. If you’re selling a mattress, you can bundle it with a box spring and frame. These are all products that go hand in hand.

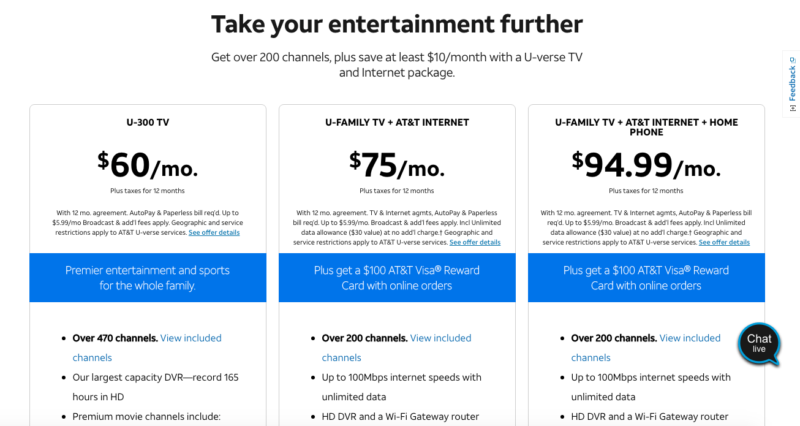

Check out this example from AT&T.

It’s extremely common for people to purchase TV, Internet, and phone services from the same provider. The price bundling strategy here is a well-oiled machine. Just look at the three options above to see what I’m referring to.

It’s $60 per month for just TV. But when you bundle TV and internet together, it’s only $15 more.

This type of product bundle increases the perceived value: Customers are getting something that would normally cost $110, if purchased separately, for $75. That’s a great deal.

This is much better than offering a TV package with free remote batteries, or something cheap that doesn’t add value or entice people to buy. By doing this, AT&T can increase their order value by 25%. Think about that for a second here.

If your company does $1 million in sales annually, you can make an extra $250,000 per year just by increasing the AOV from $60 to $75.

AT&T takes this one step further by adding another bundle option, which includes home phone services. By getting customers to buy this bundle instead of TV alone, the order value is 58% higher.

Use anchor pricing

Anchor pricing is another way to show value in your product bundles.

The idea behind this methodology is that you have different prices on your website that establish a perceived value in the mind of your customers.

It’s an age-old strategy.

How do you sell a $500 watch? Put it next to watch that costs $1,300. The $1,300 item will serve as the anchor, which makes the $500 product seem like a much better deal.

Let’s take a closer look at AT&T’s third option — adding a home phone for an additional $19.99 a month. How many people do you imagine want a phone line? This option may be less about increasing the order value and giving another point of comparison to make the middle option more interesting. Because the $75 package isn’t the most expensive package, the price point seems more reasonable.

The $60 TV package also serves as an anchor. It sets the value of TV alone, so all of the product bundles after it seem like a great deal based on the customer perception of the one product.

You can use this same strategy with your product bundles by adding more expensive bundles, or selling the solo products at a higher price than when they’re bundled. It doesn’t matter if your customers don’t purchase the higher priced packages. They can serve as anchors to make the rest of the options more appealing.

Recommend products to your customers

Show your customers products that will enhance the item that they’ve already added to their cart. Depending on the circumstances, the customer may not even realize that you sell those additional products or remember that they need to buy them until you do this.

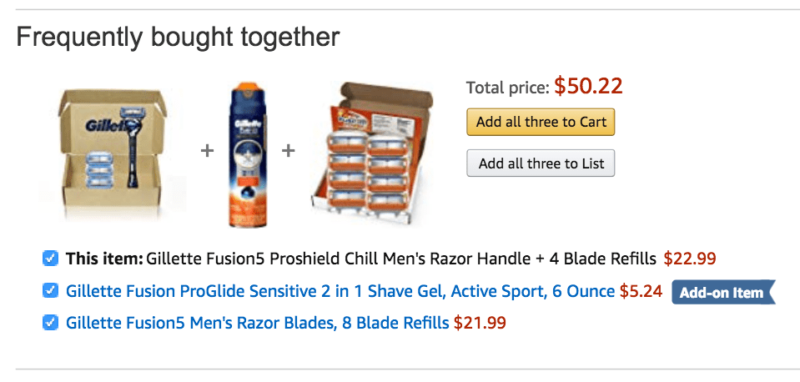

Amazon uses this strategy better than anyone else.

If you’re browsing for razors on their platform, Amazon will show you which products are frequently bought with those razors: shaving cream and blade refills. The customer will realize that they need these items to complement what they were initially shopping for.

Instead of having to go back and browse for these products, Amazon has a button that makes it easy to add all three items to the shopping cart. You can get more conversions by optimizing your checkout process. Click to add and Amazon has increased the order value with product recommendations.

Here’s the kicker: none of the products are even discounted.

You don’t necessarily need to offer sales or drastically slash your prices to have an effective bundling strategy. Just by showcasing and recommending similar items that add value to the consumer, you can increase your AOV.

Offer volume discounts

But, you can also offer discounts. In addition to bundling products with other items, you can bundle the same product or service with itself. Amazon does this with Subscribe & Save. It gives your customers a reason to buy more, order-value wise, than what they were going to buy — and to make that next repeat purchase from you, instead of wherever else they would be in the future.

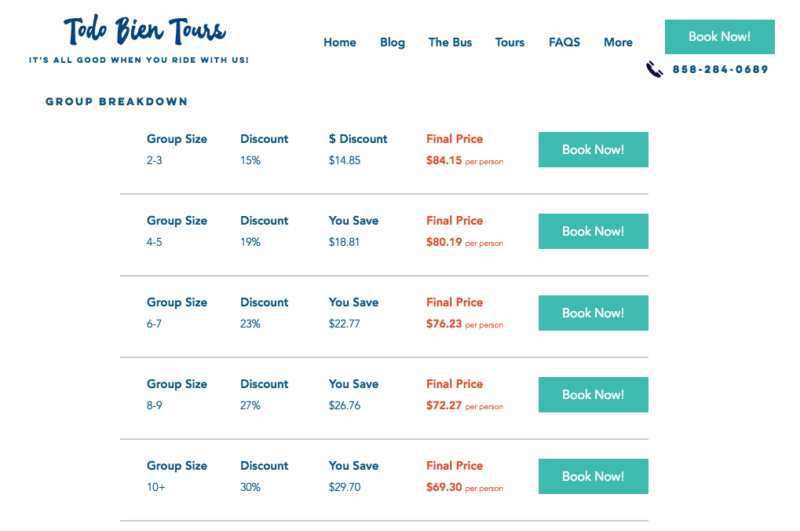

Just like the 5% subscription discount on Amazon, as the volume increases, the price per item decreases. But your average order value will still rise. Here’s a perfect example from Todo Bien Tours.

This company provides a service: bus tours. The price per ticket for their tours varies by the number of tickets sold at once. If you buy two tickets, they will cost $84.15 each, so the total transaction will be $168.30. But, groups of ten pay $69.30 per ticket. While the price per item is less, the total transaction ends up being $630. That’s more than a 400% increase in order value.

Notice how their pricing structure is set up on the website.The chart displays the percent discount based on the number of tickets purchased as well as the monetary value saved per ticket. This is an example of one of our previous points: emphasizing savings. By combining this strategy with volume discounts, Todo Bien Tours can benefit from higher average order values.

Allow customers to create custom bundles

Studies show that 80% of customers are more likely to buy something if they are offered a personalized experience.

Furthermore, 68% of customers will pay more for this type of experience. That’s why customization can highly benefit your bundling strategy. It’s a great way to increase your average order value. Rather than telling your customers which products you’re bundling, let them decide for themselves.

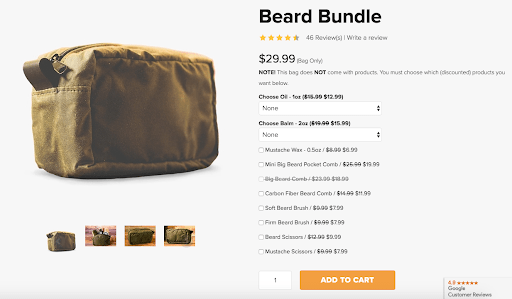

Look at how Texas Beard Company accomplishes this.

By purchasing the bag, their customers can benefit from discounted prices on other products. The customized bundle makes it more enticing for people to buy. Here’s why. Let’s say that the bundle was preset with a bag, beard balm, mustache scissors, and beard brush, but the customer already owns a pair of mustache scissors. For that person, the bundle isn’t enticing. They don’t need one of the products offered, so it’s not a good value for them.

This goes back to perceived value. Though the mustache scissors have a literal value, the value to that customer is $0, so the entire perceived value of the package is lowered. Customized options make the bundle so much more enticing.

Find a way to implement this strategy for your business as well. It can work regardless of if you’re offering products or services.

Conclusion

One of the easiest ways to grow your company is to increase your average order value.

That’s because you don’t need new products, new customers, or higher conversion rates to accomplish this.

All you need to do is find ways to get your customers to spend more money each time they shop:

- Make sure you’re not bundling something inexpensive and irrelevant with one of your premium products.

- Bundle similar items. You can even recommend products to your customers to create a bundle.

- The savings should be obvious, which enhances the perceived value of what you’re selling.

- Focus on your pricing strategy. Offer volume discounts and use anchor prices.

- You can charge more for your products by letting your customers customize their own bundle.

If you follow these strategies, you’ll be able to increase your AOV.

What types of product bundles is your business offering to increase the average order values on your website?

Source Quick Sprout http://bit.ly/2Q79EPi