Every business needs to come up with creative ways to drive sales.

Sure, you may be doing well today, but how are you planning on making money tomorrow? What about next month or next year?

Whether your company sells a physical product or offers a service, the subscription business model is something that you should consider using to generate recurring sales.

Historically, implementing a subscription business model has proven to be highly profitable.

In the last five years, this model has grown by more than 100%.

Businesses that know how to offer valuable subscriptions end up with extremely loyal customers, which is why it’s such an effective customer retention strategy.

Even ecommerce brands have been using subscriptions to drive sales.

That’s because the consumer market has accepted this model, causing it to grow in popularity over the last year.

Once you’re able to get customers to pay for a subscription, you’ll get recurring sales on a monthly or annual basis.

As a result, your company will be in a great position for sustainable growth over time.

But if you’ve never implemented a subscription model to your business, it might be a little bit intimidating for you. Where do you start?

Some of you may have already set up a subscription model for your business. But unfortunately, it’s not working out as well as you thought it would.

That’s why I created this guide.

Whether you’re new to the subscription concept or you want to make adjustments to your existing subscription model, I’ll explain what you need to do to be successful in this space.

Don’t charge for your basic package

Offer your most basic package for free.

Now for some of you, this may not be realistic. For example, if you’re offering clothing or accessories delivered on a monthly basis to your customers, you can’t just give that away for free each month.

But for those of you who are offering an intangible service, it’s a great way to get people interested if you have multiple packages.

- games

- mobile apps

- streaming services

These are all great examples of how you can leverage a free package to eventually get your customers to pay for the service if you’re in these industries.

For those of you who have a mobile application, this strategy is a great way to improve the profitability of your small business mobile app.

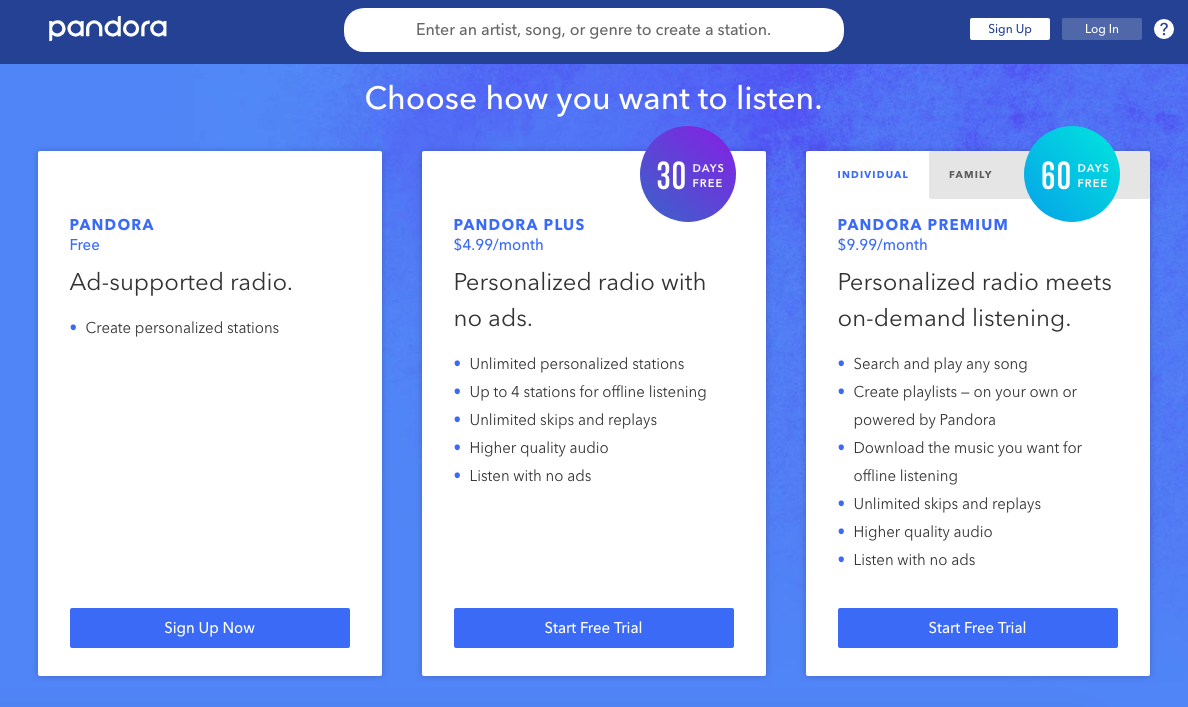

Let’s look at the Pandora packages as an example.

For those of you who aren’t familiar with this company, they offer a music streaming service.

As you can see from their website, they have three different listening packages. The basic package is free.

This introductory package gets people familiar with the service. If they had to pay from the beginning, they’d be less likely to try it out in the first place.

But if you offer something for free, there is no risk in people using it.

Now you’ll have a better chance of getting these free subscribers to upgrade their service for a fee.

Offer a free trial for your premium services

So you’ve offered your basic package for free. But customers still haven’t upgraded yet.

Why not?

Well, they don’t know what they’re missing.

If you offer them a free trial of a paid service, it will be harder for them to go back to the basic version. Let’s refer back to the Pandora example.

They offer a 30-day free trial for their $4.99 package. So for one month, customers on this trial will experience personalized content with no advertisements.

Once they go back to music that’s not personalized and are forced to listen to ads, they’ll be more inclined to pay the monthly fee for the enhanced experience.

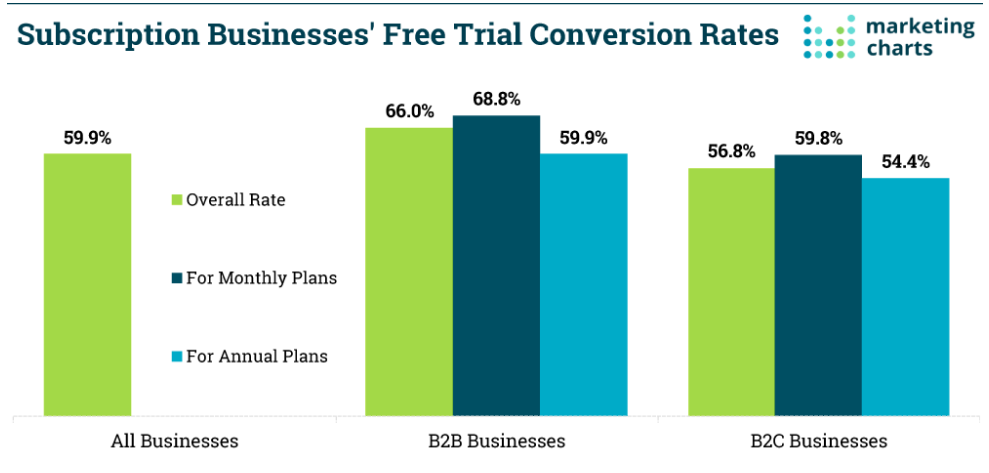

Roughly 60% of all businesses are able to convert free trial users to customers.

Those conversion rates are outstanding.

For those of you who are offering physical products, such as a box of items mailed to customers on a monthly basis, you can use this strategy as well.

Even though you may not be able to do this long-term, you can still offer a month or two of your package for free.

Here’s something else to consider. The more expensive your subscription is, the longer you should offer the free trial for.

Again, we’ll continue to use Pandora as an example.

They offer a 60-day free trial for customers who want to try out their most expensive package at $9.99 per month.

It’s worth giving away two months for free if they’re able to generate $120 per year from each subscriber.

Set up different membership plans

Profitable subscription models have different plans. There are a few reasons for this.

First of all, not everyone can afford your most expensive membership, but you don’t necessarily want to exclude those people from being paying customers.

Second, you want to offer plans based on the needs of different customers.

People don’t want to pay for a feature or benefit that they won’t use. But if someone knows that they need something, they’ll gladly pay an additional fee.

Let’s look at the Netflix membership plans as an example.

All of their plans offer the first month for free and the ability to cancel anytime. Their customers can watch from their laptops, tablets, phones, and TVs.

But the basic membership doesn’t offer HD video and only lets you watch on one screen at a time.

So for someone who doesn’t have an HD television and doesn’t plan on sharing the account with anyone else, this is a suitable option.

But if you’ve got a family that’s going to be sharing the account and streaming simultaneously from multiple HD devices, this won’t be enough for you.

Those customers will need to subscribe to the most expensive option.

Allowing customers to select their plan gives them a personalized experience. Plus, we already know that personalizing your website boosts conversions.

So analyze your features and come up with a few different membership plans that target the needs of various customers.

Give discounts to customers who pay in advance

Obviously, you want your customers to be a subscriber for as long as possible. That’s how you make money with recurring sales.

But with that said, you don’t want to force your customers into a long-term contract.

This strategy can make people hesitate to sign up. Consumers like having the option to cancel at any time without having to pay a penalty.

That’s why monthly subscription plans are so common.

The problem with monthly subscriptions is that if a customer cancels after a couple of months, you didn’t really have a chance to generate high profits from them.

Who knows. Maybe in that short period of time they didn’t have a chance to fully experience everything that your subscription plan has to offer.

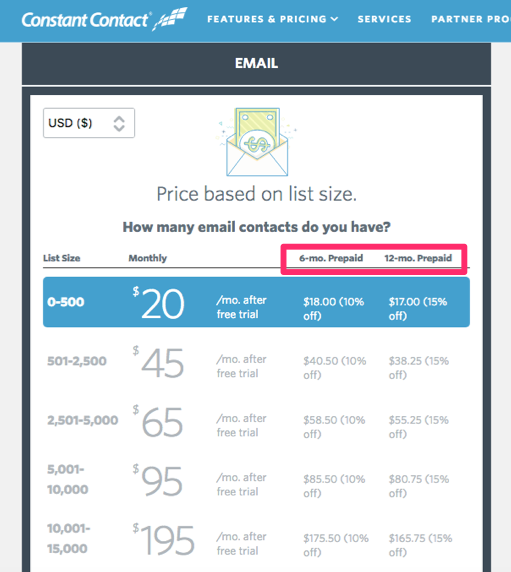

If you want people to commit for longer periods of time, you can offer discounts if they pay in advance. Take a look at this example from Constant Contact.

As you can see, they offer a 10% discount and 15% discount for subscribers who pay for six months and 12 months in advance, respectively.

Even though you’re making less off each customer per month, you’re locking them in for a longer term.

This is a much more effective strategy than forcing your customers to commit to a year contract that charges them on a monthly basis.

Giving them the option benefits both of you. They’ll get a discounted rate, and you’re guaranteed to make money.

Plus, it adds more of a personal touch, which we previously talked about and we’ll continue discussing in greater detail throughout this guide.

Provide added benefits to your customers

Depending on your business, offering subscriptions exclusively may not be in your best interest.

You can still have other business models that you use in addition to your subscription model.

So for those of you who fall into that category, you need to make sure that the subscription memberships come with benefits that justify the cost to your customers.

Otherwise, they won’t have any incentive to join.

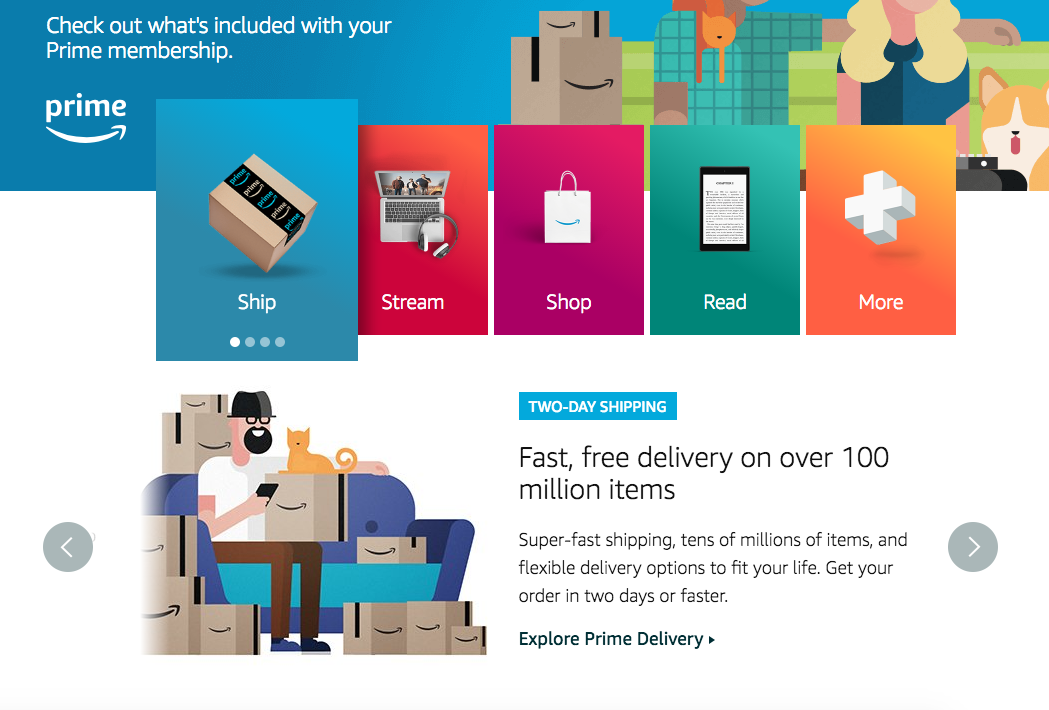

A perfect example of what I’m talking about is the Amazon Prime membership.

You don’t need to pay a monthly or annual fee to buy something on Amazon. Anyone can use this ecommerce platform.

But for customers who shop frequently and want their items delivered as fast as possible, they may be more inclined to pay for the Amazon Prime subscription.

This membership offers two-day free shipping for subscribers.

In addition to the shipping benefits, Amazon Prime members also get access to music and video streaming services.

As I explained earlier, they have packages designed for everyone.

For customers who just want the video streaming service, they can pay $8.99 per month.

To get all of the membership benefits, including video streaming, two-day shipping, music streaming, photo storage, unlimited reading, and free same-day delivery for certain items, it costs $12.99 per month.

That totals just under $156 for the year, assuming that they keep the membership without canceling.

But if a customer wants to save money and knows that they’ll use the service for an entire year, they can pay $119 annually and save roughly 25% on their membership.

Amazon also offers a free trial for prospective members to try out their Prime service for 30 days at no cost.

Do you see how they incorporated most of the strategies that we talked about so far?

It’s always a good idea to follow the lead of successful companies and apply their concepts to your own business.

Set your subscriptions to renew automatically

Let’s say you get someone to sign up for one of your subscriptions. That’s great news!

You’ve got their credit card information, and you’re ready to start processing their account.

But you want to make sure that you set these memberships up to renew automatically.

Don’t worry, I’m not saying that you should do this to be deceiving or trick your customers. Just include this in the terms that they agree to when they’re signing up.

You don’t want to annoy them each month asking them for their credit card information again. So get their permission from the beginning to bill their card each month.

This is a great way to get recurring sales.

If you give the customer the option to opt-out each month, they may decide to cancel.

But if their card just gets charged without any contact or notification, they may just keep the service whether they’re using it or not.

For example, how many of you have a gym membership or have had a gym membership in the past? You get charged each month whether you’re there every day or never show up.

You don’t cancel it because it’s more of a pain to go through that process and then sign up again when you want to go.

So your customers will treat this membership the same way. Sure, you obviously want your customers to take advantage of the products and services that you’re offering.

But if they’re paying for it, either way, does it really matter if they do? Not really.

Allow your customers to customize their subscriptions

We’ve talked about personalization quite a bit in this guide.

You can take this concept to the next level by allowing your customers to fully customize their subscriptions. Take a look at this example from Sirius XM Radio.

They have membership options that allow customers to pick and choose which stations they want on their account.

You can find ways to apply this same concept to your business as well.

For example, let’s say that your brand sales beard grooming and shaving products for men.

You sell products directly from your website, and you also have subscription options to deliver a box of products on a monthly basis. Allow your membership subscribers to customize each order.

Some customers may want more razors, while others want more shaving cream and after shave lotion.

The membership prices will vary based on the type of products and quantity of items that the customer wants to be delivered each month.

Conclusion

The subscription business model is extremely profitable, and it’s growing in popularity.

Whether you’re adding subscriptions to your business for the first time or you’re making changes to your existing model, there are certain tips and tricks that will improve your chances of being successful.

Offer your basic package at no charge. Then, let customers try out the premium options with a free trial.

Create different membership plans to target a wider range of prospective customers.

Your standard memberships should be charged on a monthly basis and renew automatically. Encourage customers to pay in advance by offering discounted rates for an annual plan.

Provide added benefits to make sure that your subscriptions are worth the cost.

Focus on personalization and customization that entice consumers to sign up for your subscription service.

If you follow the advice that I’ve outlined in this guide, you’ll be able to achieve sustainable growth in the form of recurring sales through subscriptions.

How is your brand using the subscription business model to generate recurring sales?

Source Quick Sprout https://ift.tt/2Neudfe