EAST STROUDSBURG — A private and public sector partnership in the Poconos has set its sights on lowering local broadband internet prices by 50% and eliminating cellular dead spots in Monroe County. Accelerate Pennsylvania, the coalition behind the Monroe Gigabit Project, has taken the next in its latest endeavor, the Monroe 5G Project, by issuing a 100-second cost survey to potential customers and service providers.AcceleratePA founder Kelly Lewis, who is also a former Monroe [...]

Source Business - poconorecord.com http://bit.ly/2WowvZN

السبت، 8 يونيو 2019

8 Best Payment Methods For Your Ecommerce Site

In order to operate a fully functional ecommerce website, you need to be able to accept payments from your customers.

There is no way around this. Your entire business revolves around getting paid.

That’s why you starting selling online in the first place, right? To make money.

But there are tons of different options for accepting payments online. Whether you have an existing ecommerce platform or if you’re starting an ecommerce site from scratch, your payment gateway needs to be a priority.

You need to have options in place that will be appealing to all of your customers.

That’s because everyone has different preferences. So you should consider adding multiple payment methods to your ecommerce site.

I realize that not all of these options will be equal in terms of the cost that you’re paying to implement them on your site. But in the long run, those fractions of a percentage won’t make that much of a difference when you weigh them against the revenue from your sales.

You won’t think twice about it once your conversion rates start skyrocketing.

For those of you who are ready to take your ecommerce platform to the next level, I’ve narrowed down the best payment methods for a fast and secure checkout process in 2019. These are the top options for you to consider.

1. Stripe

Stripe is one of the top payment methods on the market today because it’s so versatile.

It’s a great choice for ecommerce shops, subscription services, or on-demand marketplaces. So for those of you who operate a business with multiple processes and services, this is definitely something that you should take into consideration.

Another top feature of Stripe is the ability for you to set up recurring payments from your customers.

It supports payments online, as well as in-person. So if you currently have a brick and mortar store, you can add a Stripe POS system in addition to the gateway on your ecommerce site. This way you can remain consistent across both marketplaces.

Studies show that brands using Stripe have increased revenue by 6.7% after implementing the payment gateway. With Stripe, you’ll have 81% fewer outages and 24% less operating costs compared to competing payment methods.

Another reason why I love Stripe is because you’ll have the option to customize your checkout process with the Stripe UI toolkit.

Stripe accepts all major credit cards and debit cards from all countries, including:

- Visa

- Mastercard

- American Express

- Discover

- JCB (Japan)

- UnionPay (China)

You can also integrate some alternative payment options into your Stripe payment gateway. Some of these we’ll discuss in greater detail as we continue through this guide.

- ACH transfers

- American Express Checkout

- Masterpass

- Visa Checkout

- Apple Pay

- Google Pay

- Microsoft Pay

It’s great for those of you who are using your ecommerce platform to drive sales from mobile users.

Stripe’s standard pricing is simple. As a merchant, it will cost you 2.9% + $0.30 for every card charge. There will be an additional 1% charge for international cards.

For ACH transfers, your cost is 0.8% of the transaction with a $5 maximum fee.

Additionally, Stripe offers customized pricing options for those of you who have a unique business model or have large volume payments. You’ll get discounts for volume and multi-product rates, as well as some country-specific rates if you’re targeting an international market.

Stripe has exceptional tech support and customer service. You can reach representatives 24/7 via phone, live chat, or email. Overall, it’s definitely one of the top payment methods for you to use on your ecommerce site.

2. PayPal

PayPal is a name that I’m sure most of you are already familiar with. The company has a reputation that speaks for itself when it comes to ease of use, reliability, and security.

This is why you should consider adding PayPal to your website.

According to Statista, there are 277 million active PayPal users across the world in 2019. That number is up from 237 million from the beginning of 2018.

Simply put, there are tons of users, and they are continuing to grow.

For those of you who don’t have a well-established name brand yet, the PayPal button can help put your customers at ease. They know that PayPal has their back for security.

Plus, people might have a PayPal balance that they want to use for spending, as opposed to charging a credit card or debit card.

PayPal is the most commonly used digital wallet in the world. Here’s something else for you to consider.

Websites with PayPal checkout options convert at an 82% higher rate than sites without PayPal.

With PayPal for ecommerce you can accept:

- Credit cards

- Debit cards

- PayPal

- Venmo

- PayPal Credit

Any ecommerce sale in the US will cost you 2.9% + $0.30 per transaction. International sales are a bit more expensive, with 4.4% per transaction, plus a fixed amount depending on the country the purchase came from.

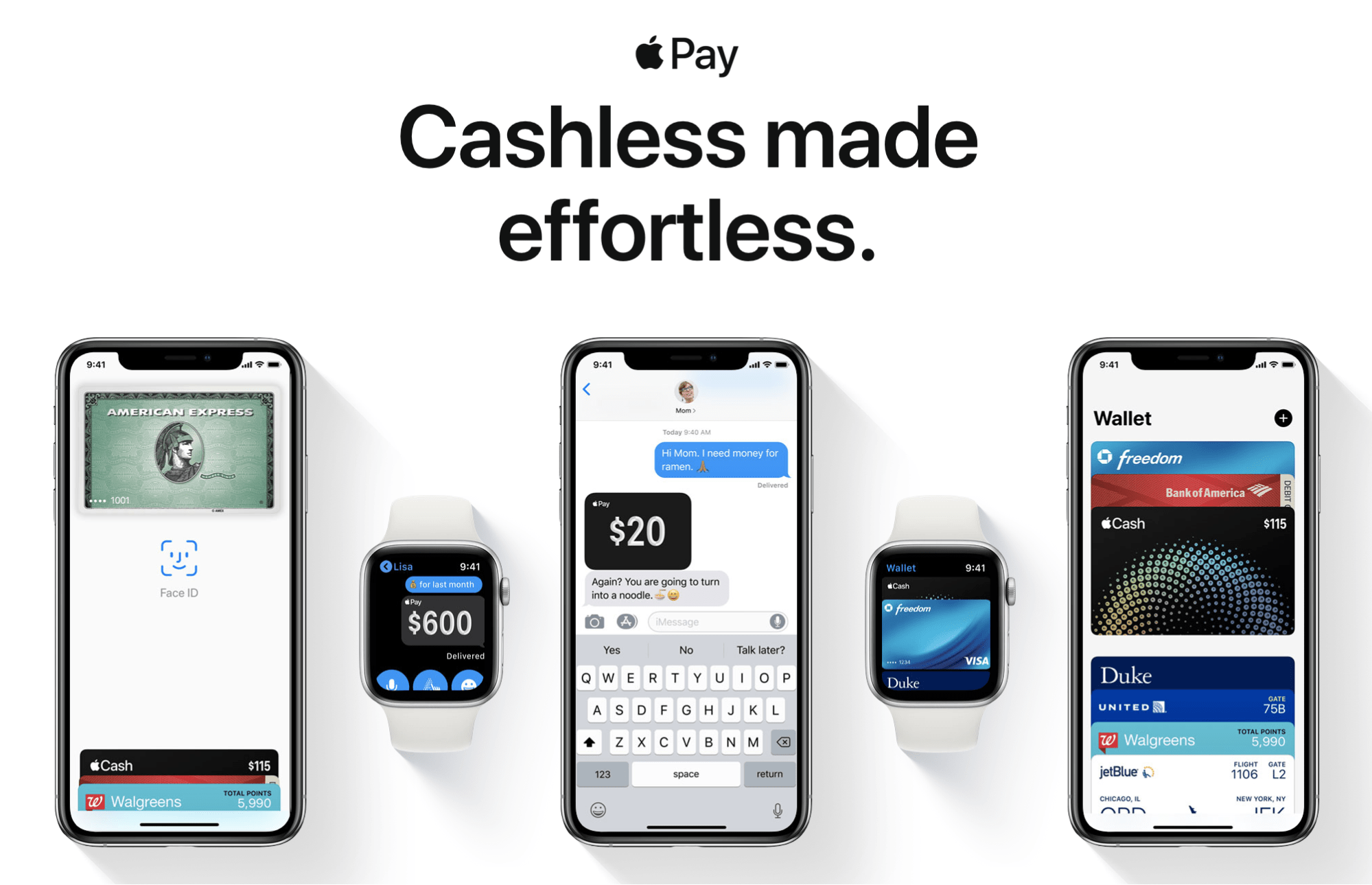

3. Apple Pay

Apple controls over 54% of the mobile vendor market share in the United States. So it’s safe to say there are more than a fair share of people in America walking around with iPhones in their pockets.

Apple Pay is the digital wallet for iOS users.

Once people set it up on their devices, they can pay for items with just one click. This is great news for your ecommerce shop. You no longer have to worry about people being turned off by filling out long form fields with their credit card numbers and billing addresses.

All of that information is safely stored in Apple Pay.

For users who are shopping on your mobile site or mobile app, they can finalize the payment just by using a fingerprint or facial recognition. It doesn’t get much easier than that.

In addition to your ecommerce site, mobile site, and mobile app, Apple Pay can also be accepted in-person at brick and mortar stores.

One of the top highlights of this payment gateway is the fact that Apple doesn’t charge any additional fees to merchants for accepting Apple Pay.

4. Square

Square is commonly associated with its POS systems for in-person payments. But it also has ecommerce options for your website.

This is a great choice for those of you who have physical retail locations and plan to start selling online, especially if you already have a Square POS system. It’s also a great option if you’re planning to open retail locations in addition to your ecommerce shop.

Square is priced competitively compared to the other methods on our list.

There is no monthly fee for adding the Square payment gateway to your website. They charge you 2.9% + $0.30 per transaction, just like Stripe and PayPal.

Integrating Square to your ecommerce platform is easy. Some of their ecommerce partners include:

- Wix

- WooCommerce

- GoCentral Online Store

- Ecwid

- 3DCart

- OpenCart

- Magento

- Miva

- Drupal Commerce

- X-Cart

- Zen Cart

- ShipStation

- Mercato

- Unbound Commerce

- WordPress

- nopCommerce

- WP EasyCart

- Sociavore

So if you’re currently using one of these platforms for your ecommerce shop, adding Square will be a breeze.

5. American Express

American Express doesn’t necessarily dominate the market share of credit cards. But it has some of the highest consumer satisfaction rates in the industry.

In fact, American Express ranked second only to Discover in a 2018 study by JD Power.

The study ranked customer satisfaction on a 1,000-point scale. American Express was given a score of 830, while Discover barely edged them out with a score of 836.

The only downside of American Express is that they have a reputation of siding with the consumer in cases of disputes, which is probably why their satisfaction rates are so high.

But with that said, they offer fraud protection for merchants as well, with 24/7 access to customer support.

Amex payments can be processed in more than 170 different countries.

The added service and benefits of American Express does come at a price. Pricing starts at $20 per month for the Amex payment gateway.

Their lowest rate comes with up to 100 transactions included before you’re charged $0.12 per additional transaction over 100. For $25 per month, you get 350 transactions included with $0.11 per additional transaction. $55 per month gets you 1,000 transactions before you’re charged $0.08 per transaction after you reach the 1,000 mark.

Depending on the plan you choose, you’ll pay a one-time setup fee of $99, $175, or $250.

Additional features like payment tokenization and Accertify fraud protection professional upgrades cost $20 per month and $24.95 per month, respectively.

But if your ecommerce store can generate hundreds or thousands of Amex transactions per month, these fees will be well worth it.

6. Masterpass

Masterpass is a way for you to target customers who are Mastercard holders.

It’s a fast and secure way for those people to pay through your ecommerce shop or mobile app. They won’t need to type in their credit card numbers and billing information if they already have Masterpass set up on their devices.

It’s very easy to integrate Masterpass on your ecommerce site or mobile app.

The payment method comes with advanced security. It has standard features like fraud monitoring, tokenization, and user verification.

There are no additional fees to you or the customer if you accept Masterpass on your ecommerce site.

7. Visa Checkout

Similar to the services offered by Mastercard, Visa Checkout is a digital wallet for Visa customers.

In the United States alone, there are more than 337 million people with a Visa card. That number skyrockets to 781 million when you factor in the Visa cards worldwide.

It’s a great way to target those people on your ecommerce site and mobile app.

82% of consumers who have enrolled in Visa Checkout have used that payment method to complete an online transaction. More than 20 million people have enrolled in Visa Checkout.

Furthermore, more and more merchants are accepting this payment method. Over 300,000 businesses now accept Visa Checkout.

So if your competitors have this on their website, you need to make sure that you do as well.

8. Google Pay

Last, but certainly not least, on our list is another digital wallet offered by one of the most recognizable names in the world; Google.

Google Pay is made for ecommerce shops, mobile apps, and in-person checkouts.

Industry giants like Airbnb and StubHub have already added Google Pay to their checkout processes. After integrating the new Google Pay API to their site, StubHub saw a 600% increase in unique visitors buying with Google Pay.

Customers are slowly but surely starting to get more familiar with it.

Google Pay is very easy to integrate into your ecommerce platform. Just gain access to the API and add it your site. After you run some tests it will be good to go.

It’s also worth noting that Google Pay can be integrated with other payment methods that you might already be using on your site, like Shopify, as well as some of the other ones we’ve already covered on this list, like Stripe and Square.

Conclusion

Your ecommerce site is useless if you can’t get paid. It’s time for you to realize that all of your customers don’t have the same preferences.

You need to give them as many options as possible to increase your conversion rates.

Digital wallets are growing in popularity. It’s easier for customers to use these alternative payment methods as opposed to manually typing out their payment information. By reducing friction in your checkout process, you’ll be able to drive more sales and reduce shopping cart abandonment rates.

That’s why you should consider adding these payment methods to your ecommerce site. The more options you have, the better it will be for you in the long run.

Source Quick Sprout http://bit.ly/2R5rXXz

Feeling Good, Feeling Bad, Feeling Broke

At some point about three years ago, I was browsing a self-improvement book at the library, just leafing through the pages. I truly wish I could recall what book it was; all I can remember is that it was probably a new release about two or three years ago, and it might not have had anything to do with finances or self-improvement at all.

I happened to stop on a page in this book where it laid out an interesting exercise for self-improvement.

It said to make a list of ten moments in the last year where you really felt good. The book encouraged the reader to try to not think about special events or big moments, but rather try to focus on the little ones, the moments of everyday life where you felt great physically or mentally or socially or in some other area of your life.

Then, the book said to make a list of ten moments in the last year where you really felt awful. Again, the book encouraged the reader to not think about special events, but the moments of ordinary life where you felt the worst physically or mentally or socially or in some other area of your life.

Why do this? The book suggested that the best thing you can do in your life over the next several months was to maximize the things that felt good and do whatever you can to repair the things that felt bad going forward.

It was an interesting exercise, one that I wanted to try someday, so I jotted it down in Evernote and saved it to my “ideas” folder, where, as ideas do, it sat around for a very long time, until a few weeks ago when I came across it again, and I decided to spend some time doing it.

I did it over two days and gave each side of the equation some thought. I wrote down a few ideas in the morning, let it bubble in my mind throughout the day, wrote down an idea or two during the day, and then put down everything else I could think of in the evening. In both the “positive” and “negative” list, I came up with more than ten things, so I trimmed them down a bit, focusing very heavily on the “everyday” things.

My aim was to make a list of ten everyday things that really made me feel good, and ten everyday things that really made me unhappy.

I’m not going to share these lists in full, as many of the details touch on the lives of people I care about and would strongly intrude on their privacy.

However, I can share with you some big themes.

The everyday things that made me feel good generally revolved around spending time with people I have a good relationship with, engaging in my own hobbies, and spending time outside or getting some level of exercise.

The everyday things that made me feel bad generally involved being unhappy with my appearance, feeling like I had let people down, and not having enough time for the things I want to do.

These things have really informed some of my thinking about the future and goal setting as of late. It’s basically a checklist of goals, from things like working on my own health and fitness to building relationships and working on my hobbies.

This whole exercise intrigued me, so I decided to extend it back a little further.

This time, my aim was to make a list of ten things during the span of my adult life that really made me feel good, and ten things during my adult life that really made me unhappy. Again, I wanted to focus on ordinary, everyday things, not obvious peak moments like my marriage or the birth of my children, or obvious low moments like the death of my grandma.

What were the things that were part of my ordinary life that made me feel great? What things made me feel really low?

When I stepped back to this perspective, I noticed a few things.

First of all, most of the moments that felt really good in my life was when I achieved something. I felt great when I finished a big project or did something I didn’t think I could do before. (The rest of the moments were just moments when lots of ordinary elements happened to line up all at once, like a particular wonderful hike with my family a few years ago that just sticks in my heart.)

One of those moments occurred when I realized Sarah and I were free of all consumer debt. We still lived in an apartment at that time and it wasn’t too long before we were going to move into a house of our own, as our second child was on the way (I don’t believe we knew about it yet). I realized that all of our credit cards were paid off, all of our car loans were paid off, all of our student loans were paid off… we were debt free. We didn’t owe anyone a dime, and it felt really good.

The day I firmly decided to write for The Simple Dollar full time was another big day. I had built The Simple Dollar up from nothing in my spare time and the thought that this could become my full time gig was huge for me.

The day when we paid off our mortgage in full was another big day. It returned us to complete debt freedom, except now we owned our house.

Those seem like big moments, but they really weren’t. They were basically culminations of a lot of ordinary days with ordinary routines that pushed us in those directions. We spent more than a year throwing everything we had at our consumer debt. We spent four years paying off our mortgage. I worked on The Simple Dollar for almost three years before I could make that leap. They weren’t special moments – they were just the culmination of a lot of ordinary moments that may have seemed difficult at the time, but were actually pretty big positives.

It’s also worth noting that, as I discussed earlier this week, the great feeling you get from achieving something is rather fleeting; achievements themselves don’t bring lasting happiness, but the journey to get there is often incredibly meaningful and a lot of achievements can profoundly reshape your life for the better.)

On the other hand, most of the low moments were when I failed at something, particularly something that I felt I should be able to handle as an adult. These were moments when I let other people down or simply wasn’t able to take care of the responsibilities laid before me in life, even though it was well within my capacity to do so.

One of them was that spring day when I realized that, even though Sarah and I both had good jobs, we were basically unable to keep our bills paid because of our awful spending habits. We had two good jobs and we couldn’t stay afloat. We had a baby to take care of and we were failing him.

Another one was a Saturday afternoon when I was working at my old job when a bunch of things went wrong at work. None of them were really my fault or my responsibility, yet I was the one that was called and basically threatened to go in and fix whatever the problem was. Sarah and I had some out of town guests that weekend and I had to go take care of work issues and missed almost their entire visit. I remember distinctly pulling out of the parking lot of our apartment and seeing them talking to Sarah through the window and I wanted nothing more than to just go back in there, but I couldn’t, because I needed that job because I was financially beholden to it.

It’s worth noting that none of the great moments in the last year or in my life really had anything to do with spending money. All of the books I bought, gadgets I purchased, meals I ate out – all of the stuff I bought to please myself or to please others – none of it had anything to do with the moments where I felt best about myself or the moments when I was happiest with my life.

On the other hand, several of the moments where I felt worst about my life involved my disastrous financial state. These moments were the consequence of spending too much money on all of those trivial things came home to roost, and it made me feel awful. It made me feel trapped. It made me feel irresponsible. It made me feel like a loser.

There is no mountain of little treats in the world that add up to enough to counter those kinds of feelings. All of the book store visits, all of the coffee shop stops, all of the restaurant meals in the world don’t add up to enough to counteract the feeling like you’ve let everyone down and completely screwed up your adult life. They’re like putting a child’s Band Aid on a gushing wound – they stick for maybe a fraction of a second and then fall off, forgotten, not having changed anything.

So, what do all of these things add up to?

First of all, none of the best moments in the last year or even in my adult life didn’t revolve around spending money or splurging or treating myself. The moments where I genuinely felt good were moments of personal achievement or moments where I felt close to other people or moments where I was deeply engaged in an interest of mine (in other words, deep in a flow state).

All of those times when I bought myself something fun or went out to eat or dropped money on something unnecessary… none of theme even remotely compare to those moments where I genuinely felt happy and genuinely felt good about myself. At best, they provided fleeting moments of happiness that faded in moments or, at best, in a day or two.

On the other hand, the moments that really lasted, the moments that genuinely felt great, the moments that still resonate in my heart even to this day, those moments usually cost nothing at all, at least in terms of dollars and cents.

You simply cannot buy real happiness. Happiness comes from achieving things or from real meaningful relationships or from doing meaningful things.

However, money can consistently help with one thing: it can help you avoid the low points. It can help you avoid those moments when your boss is forcing you to work on that day you’ve been planning for a long time. It can help you avoid those moments when you can’t pay the bills or when you look at the debt you’ve accumulated and have a sick feeling in your stomach. It can help you avoid those moments when you feel like you have no control over where your life is headed. It can help you avoid those moments when you feel like you’ve let your kid down because you’ve just kept choosing the short term indulgences for yourself.

Those moments are harsh, they’re negative, and they last.

So, if you take those two factors together, that those peak moments are based not on spending but on achievement, and that some of those low moments are brought on by spending too much, then it makes reasonable sense to think that if you want your life to be filled with more good points and less bad points, you should strive to minimize your spending.

This doesn’t mean cutting everything fun out of your life, which is the conclusion that many people jump to. It just means that when you’re thinking of spending money on anything, think of a couple of things first.

Number one, will this purchase actually matter to me in a few months or a year? Will I even remember that I bought the name brand instead of the store brand? Will it make any notable difference in my life whether I bought this gas station Gatorade or not? Will my life really be better off in six months if I grab a fast food dinner? If you answer no, then just skip it.

Sometimes you are trying to address a need, however; maybe you do need to eat. When you find yourself with a need, address it as inexpensively as possible unless there’s a real reason to do otherwise.

The other thing you should ask yourself is how will I feel when I achieve my most immediate financial goal? Maybe it’s paying off a debt, or paying off all of your debts. Maybe it’s achieving enough savings so you can confidently tell your overbearing and seemingly cruel boss to get lost and go find another job. Maybe it’s full-on financial independence in retirement.

What you might not realize is that your choice, right now, is either another step toward that financial goal or another step away from it, and it is that culmination of a lot of steps in the right direction that makes that goal feel so impactful.

So, let’s step back for a moment. What can you take home from all of this?

First, give the two exercises described earlier in this article a try. They’re really simple.

Just take out two sheets of paper. On one, make a list of the ten moments during the past year where you felt happiest. On the other, make a list of the ten moments during the past year where you felt saddest.

Give it some time. Don’t be afraid to list everything you can think of on each one and go way over ten, but try to get at least ten written down. Leave the sheets around and add to them over the course of a day or two as you think about it.

When you’re done, examine the list of happy moments. How many of them really cost you much money? Probably not many of them. Then, examine the list of sad moments. How many of them could have been avoided if you had been more responsible with your spending? Probably at least a few of them.

Keep that in mind for a while. Remember that very few, if any, of your happiest moments had anything to do with spending money or buying stuff, while some of your saddest moments were caused by overspending or could have been avoided by being more responsible with your spending.

When you’re considering a nonessential purchase, call up those two trains of thought. When you’re considering that thing you want, is it really something that’s going to bring any sort of lasting happiness? If not, why buy it? On the other hand, would not buying it also help you avoid repeating some of the difficult moments you’ve experienced in your life, or avoid similar ones? If it would, why spend the money?

If you want a happier, more joyous life, perhaps the answer isn’t in that treat you’re about to buy yourself. Perhaps the answer is in putting it back on the shelf or driving by the store or the restaurant.

Good luck!

The post Feeling Good, Feeling Bad, Feeling Broke appeared first on The Simple Dollar.

Source The Simple Dollar http://bit.ly/2ZcJ3FA

الاشتراك في:

التعليقات (Atom)