The Bon-Ton department store at the Stroud Mall is closing.The store is among 42 locations nationwide and one of eight in Pennsylvania the company decided to close as a part of their turn-around plans.The store will close at the end of liquidation sales beginning Feb. 1."As part of the comprehensive turnaround plan we announced in Nov. 2017, we are taking the next steps in our efforts to move forward with a more productive store footprint," Bill Tracy, president and [...]

Source Business - poconorecord.com http://ift.tt/2FypGgg

الأربعاء، 31 يناير 2018

Fed Leaves Key Rate Unchanged at Yellen’s Final Meeting

The Federal Reserve has left its benchmark interest rate unchanged but signaled that it expects to resume raising rates gradually to reflect a healthy job market and economy.

Source CBNNews.com http://ift.tt/2nqhXKx

Source CBNNews.com http://ift.tt/2nqhXKx

These 10 Cities Are Great For Tech Jobs — and They’re Actually Affordable

If I asked you to describe the top places for tech jobs in the U.S., you’d probably rattle off the usual list of uber-expensive, congested cities: San Francisco, Boston or Seattle.

The money seems to flow to where the tech jobs go, which means rising rents (you’ll pay more than $1,700 for a one-bedroom apartment in Santa Clara, California) and sky-high grocery store receipts.

But what if I told you there were underrated tech centers where you could actually save enough to pay back those student loans?

With the help of a new report by Abodo, I set out to answer that very question.

The rental search company used data from the U.S. Bureau of Labor Statistics to determine the best cities for computer and math, community and social service, business and finance, construction and mining and health care occupations.

Abodo used a statistic called the location quotient, which compares a local concentration of a particular set of jobs to the national average in order to rank each city.

I grabbed regional price parity data from the U.S. Bureau of Economic Analysis to measure how expensive goods and services are in each city. I also grabbed rent statistics from the U.S. Department of Housing and Urban Development and unemployment numbers from the Bureau of Labor Statistics to gauge each city’s economic health.

Then, I applied a standard score for each category (prices, economic health, location quotient) so I could compare each one apples-to-apples. Finally, I averaged the scores by city across those categories to determine the 10 best cities for tech jobs you can actually afford.

The 10 Best Cities for Tech Jobs Where You Can Afford to Live

First off, all these cities have a higher concentration of math and computer gigs than that of the entire U.S. It should be noted that the ratio may not be as high as some of the IT heavy-hitters.

For example, Washington D.C. has a local job quotient of 2.45 (we’ll call this the tech jobs score), meaning it has more than double the concentration of tech jobs as the U.S. average. But it didn’t make our list because a single bedroom apartment goes for more than $1,400 (yikes!).

And D.C. has a 105.6 regional price parity (which we’ll call the cost index), meaning goods and services are 5% more expensive in the city than the national average.

So here’s the list: the 10 best cities for tech jobs where you can actually afford to live and save.

1. Kansas City, Missouri

Tech Job Score: 1.43

Rent: $681

Cost Index: 96.4

Unemployment Rate: 3.2%

Population: 2,104,115

2. St. Louis, Missouri

Tech Job Score: 1.15

Rent: $649

Cost Index: 94.2

Unemployment Rate: 3.4%

Population: 2,807,954

3. Cincinnati, Ohio

Tech Job Score: 1.04

Rent: $625

Cost Index: 93

Unemployment Rate: 3.7%

Population: 2,161,441

4. Raleigh, North Carolina

Tech Job Score: 1.96

Rent: $817

Cost Index: 97.4

Unemployment Rate: 3.9%

Population: 1,302,946

5. Columbus, Ohio

Tech Job Score: 1.43

Rent: $683

Cost Index: 97.4

Unemployment Rate: 3.5%

Population: 2,041,520

6. Salt Lake City, Utah

Tech Job Score: 1.31

Rent: $849

Cost Index: 96.3

Unemployment Rate: 2.6%

Population: 1,186,187

7. Indianapolis, Indiana

Tech Job Score: 1.05

Rent: $665

Cost Index: 97.6

Unemployment Rate: 3.1%

Population: 2,001,737

8. Dallas, Texas

Tech Job Score: 1.38

Rent: $807

Cost Index: 97.8

Unemployment Rate: 3.2%

Population: 7,232,599

9. Charlotte, North Carolina

Tech Job Score: 1.26

Rent: $726

Cost Index: 97

Unemployment Rate: 4.2%

Population: 2,474,314

10. Pittsburgh, Pennsylvania

Tech Job Score: 1.06

Rent: $602

Cost Index: 98.1

Unemployment Rate: 4.3%

Population: 2,342,299

So if you recently graduated with a tech degree, don’t worry too much about ending up in a pricy town. Check out the job listings in these cities — you might be surprised what you find.

Alex Mahadevan is a data journalist at The Penny Hoarder. As a bonafide Florida Man, he probably won’t be leaving the state for a while.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2GAVF0W

Here’s How HBCU Students in Georgia Can Apply to Win a $2,500 Scholarship

Georgia may be known for its peaches and Southern hospitality, but it also has one of the highest numbers of historically black colleges and universities (HBCUs).

Atlanta-based Delta Community Credit Union, in partnership with Atlanta radio station KISS 104.1 FM, sponsors a quarterly scholarship giving students attending one of the state’s 10 HBCUs a chance to win $2,500 toward their education expenses.

Not only can students apply for the scholarship themselves, but others can nominate deserving undergrads or incoming freshmen.

The deadline for this quarter’s crop of applicants is quickly approaching, so you’ll want to apply soon.

However, if you miss out on this opportunity, the good news is the sponsors will award three more scholarships throughout the year.

Apply for Delta Community Credit Union HBCU Scholarships

Scholarship Amount: $2,500

Number of Scholarships Awarded: 1 each quarter

To qualify for the scholarship, applicants must:

- Be a Georgia resident who is at least 17 years old

- Be enrolled at or accepted at any of the following schools: Albany State University, Clark Atlanta University, Fort Valley State University, Interdenominational Theological Center, Morehouse College, Morehouse School of Medicine, Morris Brown College, Paine College, Savannah State University, Spelman College.

- Write an 100-word essay on why you (or the person you’re nominating for the scholarship) deserve or need the money

Scholarship Deadline: February 15, 2018

The scholarship winner will be announced about a week after the deadline. Delta Community Credit Union will first contact the winner, and then KISS 104.1 will announce the student’s name on air.

See here for more information and to apply for the Delta Community Credit Union HBCU Scholarship.

Nicole Dow is a staff writer at The Penny Hoarder. She is the proud alumna of an HBCU — Hampton University.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2E4y7mq

Smashburger Deal Makes it Easy to Slash Your Check in Half This Week

Is it one of those nights when you just can’t bother cooking, but you don’t want to break your budget? We’ve got a dinner deal for you.

Use this printable coupon to get a free entree at Smashburger through Feb. 4, 2018, when you buy one adult entree.

To claim your free sandwich, just find your local Smashburger restaurant and present the coupon. The cheaper of the two entrees you order will be free.

Here’s the Fine Print on the Smashburger Coupon

You can order nearly any entree from the menu and get this deal, but it’s not valid on the promotional Twin Cities burger.

You also want to remember that you can only use one coupon per person per visit. That means you might have to split your orders up if you want to treat the whole family to this BOGO deal.

Act fast because this coupon is only good through Sunday, Feb. 4.

Desiree Stennett is a staff writer at The Penny Hoarder. Jessica Gray, editorial assistant at The Penny Hoarder, contributed to this article.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2vkjGWO

What You Can Do Now to Get the Most from the New Tax Law

The most sweeping tax overhaul in decades became law in December 2017. What should U.S. taxpayers do in 2018 to benefit from the tax code changes?

Source Business & Money | HowStuffWorks http://ift.tt/2EtAsoV

Source Business & Money | HowStuffWorks http://ift.tt/2EtAsoV

What You Can Do Now to Get the Most from the New Tax Law

The most sweeping tax overhaul in decades became law in December 2017. What should U.S. taxpayers do in 2018 to benefit from the tax code changes?

Source Business & Money | HowStuffWorks http://ift.tt/2EtAsoV

Source Business & Money | HowStuffWorks http://ift.tt/2EtAsoV

FroYo or Ice Cream? Who Cares? It’s All Free at Yogurtland on Feb. 6

Lieutenant Dan, ICE CREAM!

On Tuesday, Feb. 6, Yogurtland will celebrate International Frozen Yogurt Day by dishing out free 5-ounce cups of ice cream or frozen yogurt with as many toppings as you’d like from 4-7 p.m. at participating locations.

You’ll want to run, Forrest, run for this sweet freebie!

That’s right: You can enjoy your choice of free ice cream or frozen yogurt in whatever flavor you fancy and covered in as many toppings as you can handle!

I’ll go for one of Yogurtland’s newest selections: Chocolate Malt Ball ice cream made with Whoppers. Oh. My. Yum. Then, I’ll probably top it off with some Reese’s Peanut Butter Cups to re-create the Whoppers Reese’s Peanut Butter candies that seem to have sadly been discontinued. So long, farewell, my dear sweet Whoppers Reese’s Peanut Butter balls.

Anyway, if you’d rather go for the free frozen yogurt, you have oodles of toppings and flavors to choose from, including another new flavor: Chocolate Wafer Bar frozen yogurt made with Kit Kat.

Mmm… I just might have to visit two locations so I can have dessert before and after dinner

Jessica Gray is an editorial assistant at The Penny Hoarder. She once worked at an ice cream shop… and gained 20 pounds.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2DQ5WUZ

8 CRO Quick Wins for Ecommerce Sites

How well does your ecommerce website convert?

On average, ecommerce sites in the United States convert at about a 3% rate.

If you’re hovering somewhere around that number, you might think your website is already optimized for high conversions.

Even if you think you’re doing well, there’s always room for improvement.

In fact, some of the top performing websites, such as the Google Play Store, have a conversion rate close to 30%.

Companies such as the Dollar Shave Club have roughly a 20% conversion rate.

Do you still think 3% is sufficient?

I don’t.

If you have an ecommerce website, you need to constantly make improvements that add credibility to your website. This will help you get more conversions.

For the most part, these changes won’t cost you much money but will bring a massive return.

You could double or even triple your conversion rates in just a few months by implementing some of these conversion rate optimization (CRO) strategies.

Those of you who don’t know how to optimize your ecommerce site for conversions are in luck.

I’m an expert in this space and have plenty of experience consulting businesses about their CRO.

I’ve come up with a list of the top eight ways for ecommerce sites to increase their conversions.

Here’s how you can get started right away.

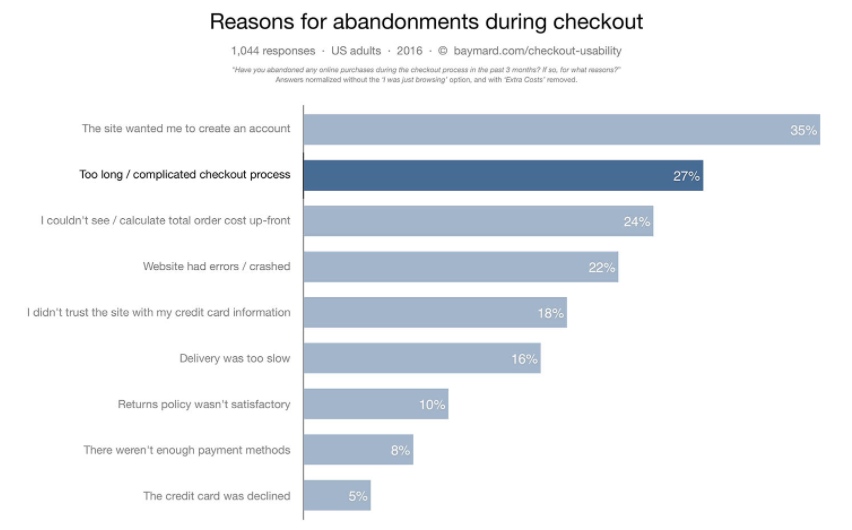

1. Simplify the checkout process

How long does it take for someone to complete a purchase once they’re done browsing on your website?

Studies show 27% of shoppers abandon their carts on an ecommerce website because the checkout process is too long and complicated:

On average, the number of steps to check out on an ecommerce website is 5.42.

If you’re somewhere in that average range, nearly 30% of your prospective customers think your checkout process is too long.

Think about how much money you’re leaving on the table.

The more steps a customer has to take to complete the checkout, the more likely they’ll abandon the cart.

It gives them too many reasons to back out.

Don’t give them an excuse. Finalize your sale.

Get back to the basics, and narrow down the information you actually need from the customer:

- shipping information

- payment information

- email address to send a receipt.

That’s really it.

You don’t need to know their favorite color or who referred them to your website.

While additional insight may be beneficial to your marketing department, you still have plenty to work with from just those few pieces of information.

Based on the shipping location, you know where the customer lives. You have their name from their payment information. And you have a way to contact them via email.

Now you can send them a confirmation email as part of an actionable drip campaign to try to cross-sell and upsell products based on the customer’s current order or location.

You can even personalize that message since you know the customer’s name.

Don’t force your customers to fill out a form that’s longer than paperwork at the doctor’s office.

Simplify your checkout process and only ask for essential information needed to complete the sale.

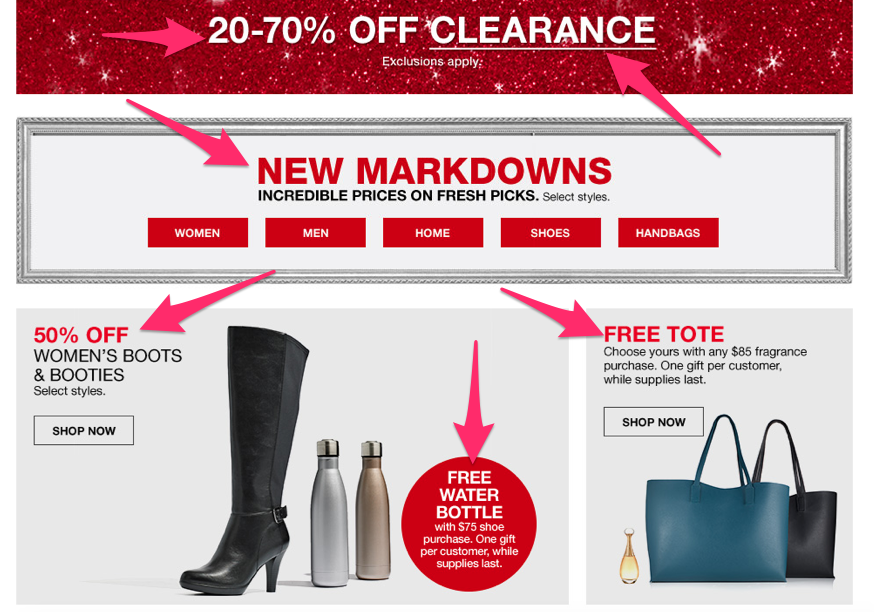

2. Highlight items that are on sale

Most online shoppers—86% of them— say it’s important for them to compare prices from different sellers before making a purchase.

It’s no secret price is an important factor when it comes to a purchase decision.

That’s why you shouldn’t hide your discounted items.

Take a look at how Macy’s highlights markdowns on their homepage:

The website is absolutely plastered with buzz words like:

- free

- X% off

- markdowns

- sale

That’s why they are able to get higher conversions than their competitors.

Customers love to get a deal.

Buying something that’s on sale makes your customers feel better about spending money.

All too often I see companies try to hide their sale items.

They would rather sell items listed at a full price.

That’s a big mistake.

Instead, highlight discounted products and services.

You can always try to cross-sell or upsell to those customers later by enticing them to buy something else through other marketing efforts.

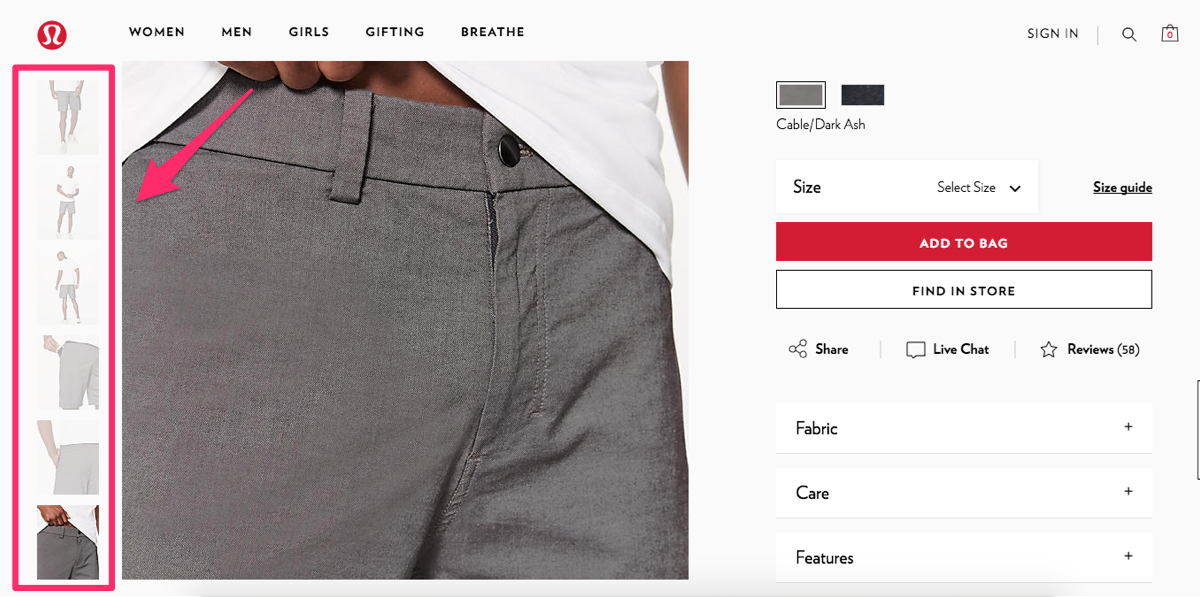

3. Display multiple pictures of the product for sale

You shouldn’t be selling anything based on just a description.

Your customers want to see exactly what they’re purchasing.

Make sure your images are high quality and portray the item in question accurately.

Here’s a great example from Lululemon to show you what I’m talking about:

There are six different pictures of just one pair of shorts.

They show the product from different angles and even zoom in on some of the top features like a pocket that’s designed to keep a cell phone secure.

Pictures are much more reliable in relating information about a product than a written description of it.

You can apply the same concept to your ecommerce site.

Sure, it may take you a little bit more time to set up each product.

You’ll have to take more pictures and include additional images on your website.

But I’m sure you’ll notice a positive impact in terms of your conversions after you implement this strategy.

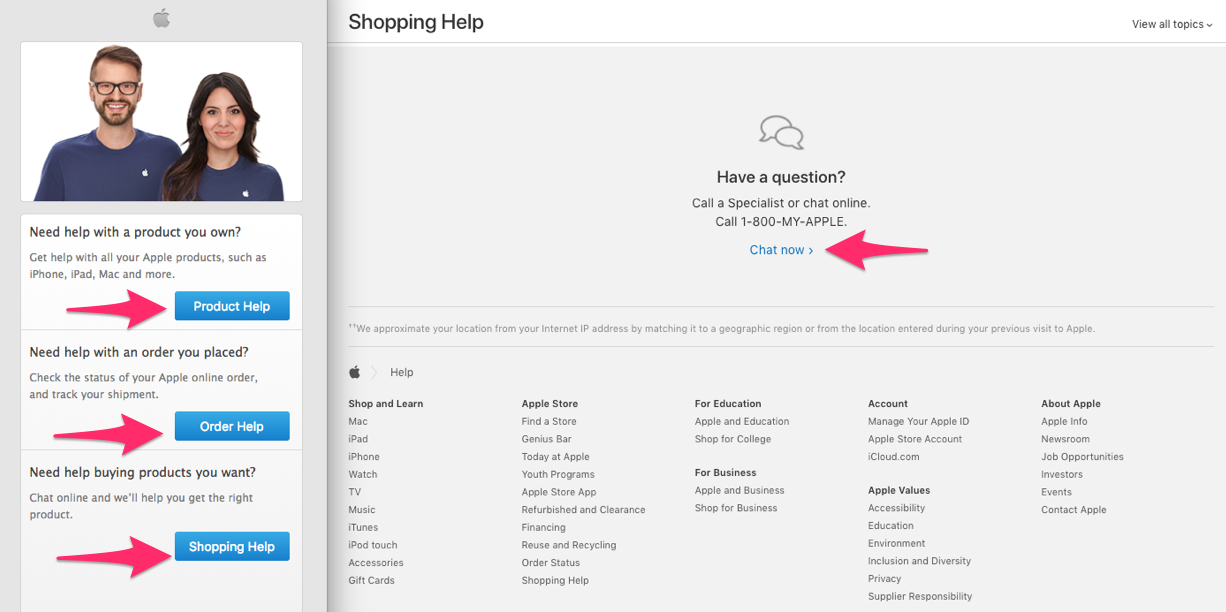

4. Provide live chat support for customers who are shopping

Even if your website is very informative, some customers may still have questions while they’re shopping.

You should set up a live chat option for your site visitors to communicate with a customer service representative.

Imagine someone wants to buy something, but they don’t—simply because they have a question and don’t have a way to get an answer.

Try to offer an online shopping experience they would get inside a physical store, with a sales associate available to assist them.

Look at how Apple does it. They offer a live chat for shoppers on their website, and it looks like this:

They make it super easy for customers to get all their questions answered online.

This is especially important if your company sells products that may need some extra explanation.

Realize not all of your prospective and current customers may be experts in your industry.

Although your product descriptions may be accurate, it’s possible there’s some terminology the customer doesn’t understand.

Rather than forcing them to pick up the phone or do outside research, offer them a live chat. Receiving this type of help can be the deciding factor that leads to a conversion for this customer.

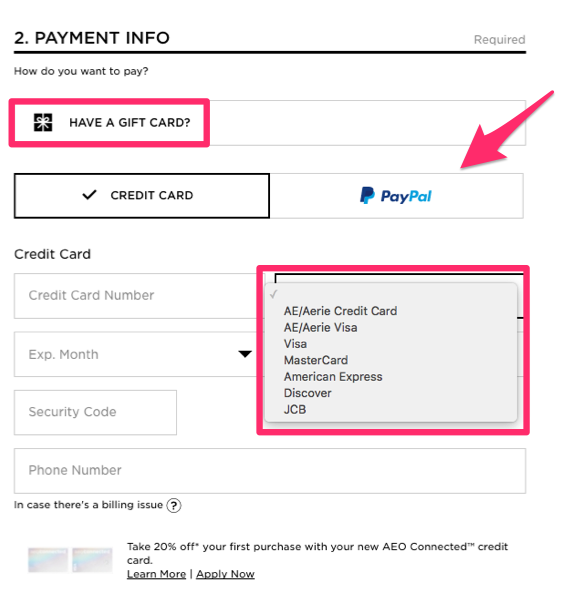

5. Offer multiple payment options

Imagine this.

Someone wants to buy something on your website, but they can’t because you don’t accept their preferred payment method.

This should never be the reason for you to miss out on conversions.

While I realize some credit card companies may charge you higher rates than others, it doesn’t mean you should restrict payment options for your customers.

Try to accommodate as many people as possible.

While I’m not suggesting you need to accept cryptocurrency like Bitcoin, you should be accepting every major credit card, e.g.:

- Visa

- MasterCard

- American Express

- Discover

You should even offer alternative payment options such as:

- PayPal

- Apple Pay

- Venmo

Here’s an example from American Eagle:

They accept nine different payment methods on their ecommerce site.

You need to offer as many options as possible for your customers.

It all comes down to convenience.

Some companies may just accept MasterCard and Visa.

They figure those are popular options, so everyone must have one, right?

But here’s the thing: you don’t know everyone’s financial situation.

While someone may have a Visa, it could already have a high balance on it, forcing them to use a different payment method.

Others may want to use their American Express card or Discover card because they get better rewards there.

And some people may not want to use a credit card at all if they have a sufficient PayPal balance.

The more options you offer, the greater the chance you’ll appeal to a wider audience.

Don’t assume everyone wants to pay with the cards you accept if that selection is limited.

Assume people will find a similar product elsewhere, where their preferred payment option is accepted, which will crush your conversion rates.

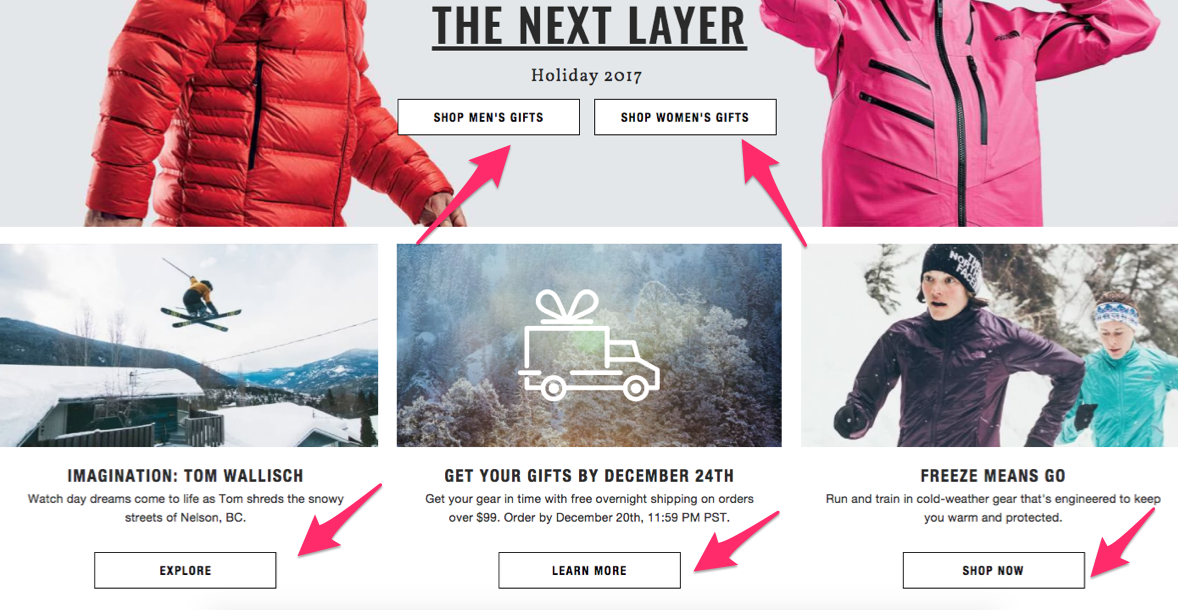

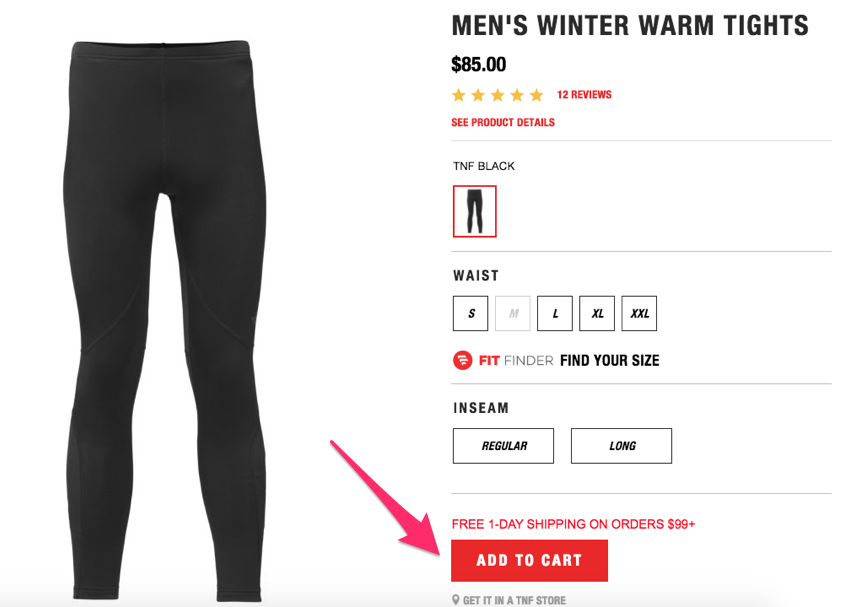

6. Have clear CTA buttons

Make sure your call-to-action buttons are clear.

They should be bold, standing out from other content on your website.

You can even put a box around the CTAs, clearly separating them from other text on each page.

Take a look at how The North Face does this on their website:

It’s clear which buttons on their homepage will direct customers to the right page.

Even though they have lots of different options, their website isn’t cluttered, and it’s organized in a professional way.

This makes navigation easy.

Now their customers can find what they’re looking for faster and start adding items to their carts.

Look at how the CTA button changes when a customer views an item:

Now the button is even more apparent because it’s red.

It stands out, so it’s clear what the customer should do.

Don’t hide your CTA buttons.

It should be easy for customers to navigate and add items to their carts.

Big, bold, clear, and colorful call-to-action buttons can help improve your conversion rates.

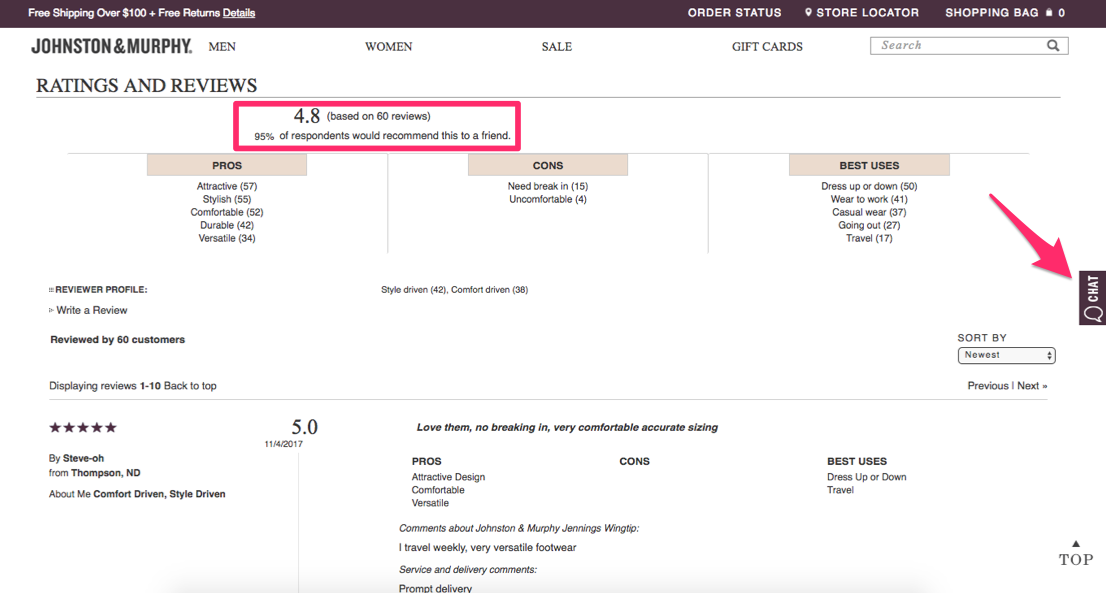

7. Include user reviews

Consider this: 88% of shoppers say they trust online reviews as much as they trust personal recommendations.

That means nearly 90% of people trust a stranger’s opinion online as if it were coming from their spouses, best friends, or family members.

Furthermore, 39% of people say they read product reviews on a regular basis, and only 12% of customers say they don’t check online reviews.

Basically, this means customers want to see what their peers have to say.

Encourage customers to review products they’ve purchased, and display those reviews on your website.

Take a look at how Johnston & Murphy does this on their ecommerce site:

More reviews means more credibility.

Obviously, you’re going to say only great things about the products you’re selling.

But other customers will be truthful about their experiences.

That’s why consumers trust these ratings and reviews.

Customers share personal stories about the uses of the products they purchased and the reasons for recommending them (or not).

Notice I also highlighted the chat option on the Johnston & Murphy website—a topic I covered earlier.

Don’t be upset if not all your reviews are absolutely perfect.

You’ll get some negative comments.

It happens.

Those negative remarks can actually help you. It shows shoppers your reviews are legitimate.

Hopefully, the positive ratings will largely outweigh the negative ones.

This will help you get more shoppers to convert and complete the purchase process.

8. Add a video demonstration

If your products are unique, include video demonstrations showing how to use them.

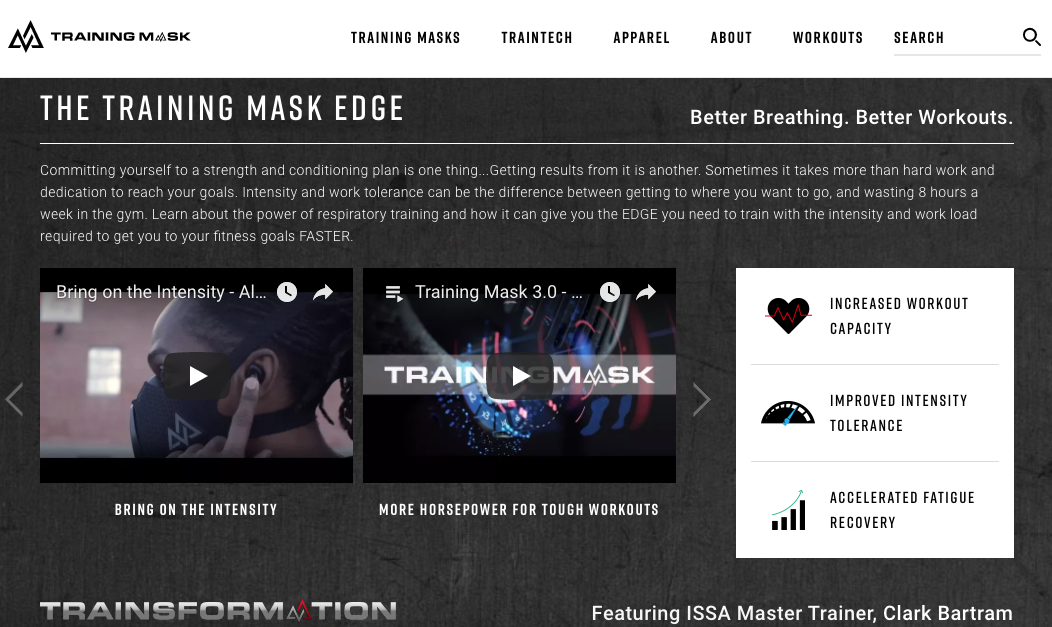

Here’s an example from the Training Masks website:

They have workout videos to show people how to use their product to train harder and smarter.

Since this product isn’t something you see every day, the majority of the population may not know how it works.

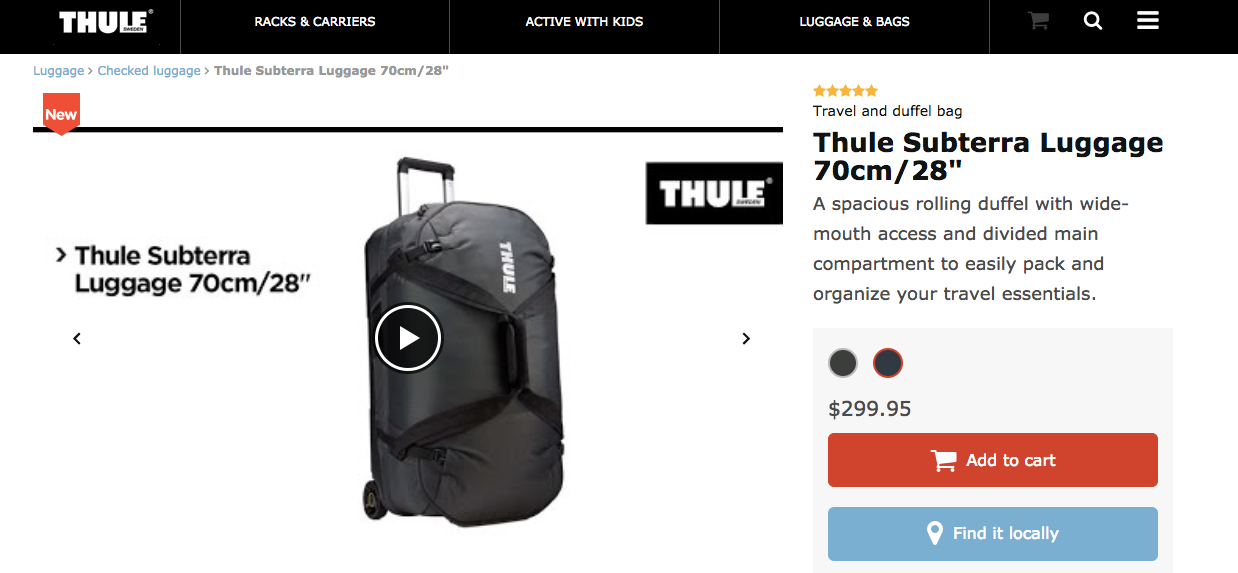

But don’t think you can’t use videos even if you’re selling something simple.

For example, everyone knows how to use a piece of luggage, right?

Well, that doesn’t stop Thule from including a video demonstration on their website:

The video shows all the hidden compartments of the bag.

It also shows customers how they can adjust the handles and straps and utilize other features.

In addition, you can include a video demonstration highlighting the features that set your product apart from similar products.

Even if you’re selling something simple, like a shirt, a video can show customers the item’s versatility for different occasions, scenarios, or weather conditions.

You just have to get creative.

Conclusion

Your ecommerce site should be making more money.

Don’t settle for average.

Take steps to improve your conversion rates.

You can make subtle changes or additions to your site that will get more people to make purchases.

Start by simplifying the checkout process. You’ll get higher conversions with fewer steps.

Emphasize items that are on sale or discounted.

Include multiple photos of each product from different angles.

Allow your customers to chat online with customer service representatives to answer any questions they might have while shopping.

This will give your customers the same feeling they get whenever they are shopping inside a brick-and-mortar store.

Don’t restrict payment options. Offer as many payment methods as possible to appeal to a wider audience of prospective shoppers.

Your CTA buttons need to be big, bold, and clear.

When placed in proper locations, these buttons can help you get more conversions.

Make sure you include customer reviews for all your products.

These recommendations can encourage others to make a purchase.

Create videos showing detailed explanations of how your products work.

This is the perfect chance for you to highlight the unique features of your product.

These tips are easy to implement, and they won’t cost you much money at all.

Trust me, they work.

You can start applying some of these elements to your website right away.

What have you done to increase conversion rates on your ecommerce site?

Source Quick Sprout http://ift.tt/2BGvuSI

The “Cash on Hand” Dilemma: How Much Is Too Much?

The idea of having “cash under the mattress” has a lot of appeal to many people. After all, cash is king and having some cash around in a quick pinch can solve a lot of problems.

An older friend of mine used to have a coffee can full of cash that he kept hidden away somewhere in his house. I’m not sure where he kept it, but I saw it produced a time or two and I couldn’t help but notice that it contained a large quantity of cash. He used it to take advantage of opportunities and to take care of things in emergencies.

A professor at the college I attended kept a false bookend in his office. It had a removable bottom and he kept about $1,500 in cash in there in $100 bills – I kid you not. He trusted me enough once to dig into it right in front of me and give me some cash to help me out in a desperate moment, an act that I still appreciate to this day because of the unquestioning generosity behind it. (I was almost completely broke and couldn’t afford the book for his class; I showed up to his first two office hours and he produce a $100 bill for me to buy the class textbook with. That’s just extraordinary generosity.)

Simply having a pool of cash around to tap into at a moment’s notice when a great opportunity appears or when disaster strikes is very worthwhile. Cash is king, after all – it solves problems.

Still, it’s hard to ignore the downside of a practice like this. Cash is untraceable, and once it’s gone, it’s gone. If you lose that cash, it’s gone. If someone steals it from you, it’s gone. If your home or apartment or car is broken into and the cash is taken, it’s gone. If your home or apartment or car burns to the ground, the money is gone.

So, there’s some risk and reward when it comes to holding onto cash. The risk is that risk of losing the money and, theoretically, the small amount of financial gain that might come from investing it elsewhere. The reward is the flexibility and opportunity that comes from having cash on hand at a moment’s notice.

Where’s the tipping point between those factors?

For me, the tipping point is enough cash to make sure my family is fine for three days during a complete natural disaster. I want enough cash to ensure that I can get my family at least 100 miles from home, feed them for three days, and house them for three days and nights. I might tap that cash for other purposes in the heat of the moment, but I replenish back up to that point.

I decided that I wanted to have enough cash available to simply handle this kind of major emergency with no questions asked. I simply produce the cash and we’re on our way.

So, how much money does that represent? I tried to imagine what would happen if there was a giant earthquake along a fault line that knocked out phone and internet and cellular traffic – no cell phones, no credit cards, and lots of destruction and fires. What do I do? I drive away from there and use cash for lodging until services start coming back up.

The exact number, then, depends on personal calculations – where you live, what things cost near your home, and so on.

In my area, and using my own calculations, that amount is $500. I keep that exact amount in cash – 5 $100 bills – hidden away at a point on my property that I can easily access in a pinch if need be.

What about you? What should your amount be? Spend some time assessing the type of emergencies you would want to be able to address with that money and what that emergency would cost you. Everyone has a different scenario that presents worry, so consider what that scenario is for you. What scenario presents you with enough concern that you would want to have cash in your house to cover it, even given the relatively small risk of possibly losing the cash to disaster?

The reality is that the tipping point comes down to your own perception of risk. Cash stored in your home for an emergency is, more than anything else, a tool that will bring peace of mind and help you sleep at night. It presents a solution to a scenario that pops up in your head and presents concern and worry into your life, and by having that solution in hand, that source of concern and worry – and perhaps other concerns and worries – melt away.

Cash stowed away in your home should be a net reliever of stress. If you find that stowed away cash is creating more stress in your life than it alleviates, then you should consider not having that much cash in your home and evaluate different plans for solving those emergencies or taking advantage of those opportunities.

Where exactly does one store that money, though? I would suggest avoiding many of the common places listed online for storing money. Burglars know about those places and will often check the obvious ones. Don’t keep it in a portable safe. Don’t keep it under your mattress or in a sock drawer. Don’t stick the bills between pages of the family bible.

Instead, think of a place in your home that you’ll remember but isn’t immediately visible and wouldn’t likely be targeted in a burglary and put it there. Mundane is usually better than super-creative. A home invader simply does not have the time to investigate every mundane and non-obvious place in your home.

If you’re still not sure, think of a few mundane places in your home, then search Google for places to stash cash in your home and use none of those places. Cross any overlapping places off of your list and use only other ideas that you may have.

Should you bury it? I consider literally burying money in a box or a glass jar to be overkill. While it is extremely unlikely to ever be burgled by someone who doesn’t already know the exact location and it’s unlikely to be damaged in a fire, it does run the risk of being completely forgotten and it takes some time and a digging tool to be able to access that money. This may be a scenario that appeals to you, but I want to have that money in a place that I can access with just a moment or two’s notice without needing any tools to access it.

What about gold or other precious items? The problem with such items is that they’re generally not items that you can directly trade for the goods and services that you want. If you’re in a situation where you’re running down the street with a gold coin hoping to swap it for a loaf of bread or a ride out of town, you’re likely already facing hardships far beyond that which you haven’t anticipated yet. Outside of those extremely rare at best and impossible at worst apocalyptic scenarios, gold and precious metals and rare coins and other such things are strictly worse to have around than cash because you have to find someone who will give you cash in exchange for them and usually at a very bad exchange rate if you’re doing it on the spur of the moment.

Remember, the purpose of having a supply of cash on hand in your home is to have easy access to it as a medium of exchange in an emergency. Items that can’t easily be exchanged in most situations are items that you shouldn’t have on hand.

Small bills or large bills? It’s likely that you already have some change and some small bills – $1s and $5s – in your possession most of the time anyway, so there’s no real need to have an emergency store of them. Plus, the more bills you have stowed away, the more space they take up and thus the easier they are to discover. Stick with larger bills – $20s at a minimum, and preferably larger ones. Yes, you may have some difficulty with change in some narrow situations if you ever have to use it, but having a smaller number of larger bills minimizes the risk of discovery.

What about keeping everything in cash? Some people have deep concerns about the banking system and want to keep all of their money in cash. My response to that is that if the banking system is ever in such complete collapse in the United States that you can no longer access any funds in your accounts and FDIC insurance has failed, there’s an extremely high likelihood that dollars are now worthless. That scenario is extremely unlikely in any case. Thus, having your money in cash is a pretty unnecessary safety risk; unless there are additional factors, you should be using banks or financial institutions to keep your money more secure than you can keep it at home.

So, let’s summarize. I think it’s a good idea to have a relatively small amount of cash on hand to handle emergencies that genuinely worry you, but not enough so that your concern about the cash is greater than the emergency you’re trying to cover. Your goal should be to minimize worry and stress by finding the right balancing point for you. If you do have money at home, store it in a mundane but uncommon place, a spot where burglars won’t immediately check; if you’re unsure, search Google for lists of common hiding places for money and avoid those entirely. Don’t keep all of your money in cash unless you have an exceptionally good reason to do so!

Good luck.

The post The “Cash on Hand” Dilemma: How Much Is Too Much? appeared first on The Simple Dollar.

Source The Simple Dollar http://ift.tt/2E03uie

This College Grad Found an Affordable Way to Start Investing in Real Estate

Buy land. They’re not making it anymore. — Mark Twain

Katie Smith had always been a saver. Even at a young age, she’d managed to save thousands of dollars.

But she was tired of watching her savings just sit in the bank, doing absolutely nothing. She needed a way to make her money grow.

“I had it all sitting in a savings account, getting something like 0.01% interest. You can only take that for so long,” says the 21-year-old, who just graduated from Georgetown University in Washington, D.C.

Ah, but there was a problem.

She didn’t want to invest in the stock market, which had been climbing for nearly nine years in a row. Smith didn’t trust it to keep climbing much longer. She’s not alone there.

“I think everything is a little overvalued right now,” Smith says.

She had always liked the idea of owning real estate. She’s familiar with the old folk saying about land being a good investment — they’re not making any more of it.

“It’s pretty limited in supply,” she says. “I like the idea that it’s super tangible.”

Ah, but there was another problem.

To start investing in real estate, you generally need a lot of money. Houses or land can cost thousands — or hundreds of thousands — of dollars. And once you buy some rental property, you’ll have to play landlord, which can be a pain.

Smith had saved herself a few thousand dollars, but it wasn’t “buy a house” kind of money. Not yet. After all, the college senior was just starting out in life, studying accounting and finance at Georgetown.

Real Estate Investing for Beginners

She wasn’t liking her investment options — savings account or stock market? — but then she heard about Fundrise.

The Fundrise Starter Portfolio would invest her money into two portfolios that support private real estate around the United States. It would do all the heavy lifting for her — and play landlord on her behalf.

She didn’t need to have hundreds of thousands of dollars stashed away, either. She could get started with a minimum investment of just $500.

“It’s a pretty low barrier to entry in terms of the amount of money you need,” Smith says. “I invested a couple grand, and I’ve been really pleased with the results.”

Through Fundrise’s online dashboard, investors can see exactly which properties are included in their portfolios — like a set of townhomes in Snoqualmie, Washington, or an apartment building in Charlotte, North Carolina.

“I can go into my Fundrise account and see what I actually own,” Smith says. “I own a piece of an apartment complex in Ann Arbor, Michigan. Property on the West Coast. Bits and pieces of apartment complexes in Texas and Denver, a construction loan, a mixed-use property.”

Many Happy Returns

More than a year after buying in, Smith has been pleased with her Fundrise experience.

Fundrise lists an average annualized return of 11.44% in 2017. Investors pay 1% in annual fees — a 0.85% asset-management fee and a 0.15% investment advisory fee.

Investors can earn money through quarterly dividend payments and potential appreciation in the value of their shares, just like a stock. Cash flow typically comes from interest payments and property income (e.g. rent).

Keeping It Rolling

A busy person, Smith likes the simplicity of the online dashboard.

“It shows your earnings to date,” she explains. “It tells you when your next dividend is. It shows you the breakdown of where your money is invested. It has a risk scale that makes it pretty easy, visually, to see how much risk you’re taking on.”

Today, having earned a bachelor’s degree in finance from Georgetown, she has a job lined up at an investment bank. Any money she makes from Fundrise just gets rolled right back into real estate.

“They give out dividends every quarter, and they have an option where I can reinvest all my dividends into their portfolios,” Smith says. “That way, I can make sure it keeps going. I don’t have to actively put more money in it unless I want to.”

The publicly filed offering circulars of the issuers sponsored by Rise Companies Corp., not all of which may be currently qualified by the Securities and Exchange Commission, may be found at www.fundrise.com/oc.

Mike Brassfield (mike@thepennyhoarder.com) is a senior writer at The Penny Hoarder. He likes real estate.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2GziXnM

Understanding This Marketing Trick Can Help You Avoid Impulse Buys

A few times per year, Adidas releases a new version of rapper Kanye West’s signature shoe, the Yeezy. Whenever this happens, sneaker fans everywhere lose their collective minds. Social media blows up, people wait in line for hours to secure a pair, and soon after the release, the shoes might command thousands of dollars on the secondary market (yes, there is a secondary market for brightly colored athletic slip-ons).

To the layperson, the Yeezys look like any old shoe. They don’t give you the ability to run faster or jump higher, nor do they unlock the secret of happiness.

So, what exactly is going on here? The answer is that Adidas does a brilliant job of leveraging an age-old sales tactic: scarcity marketing.

What Is Scarcity Marketing?

Scarcity marketing is a broad term that covers any instance in which a seller highlights the fact that an item is either rare, expiring, or in high demand. It’s a way to encourage a customer to make a purchase in a hurry, and usually at a premium price.

Scarcity marketing can involve capping how much of an item is produced, marking items down for a limited time, putting an expiry date on an offer, adding a timer to a checkout page on a website, and many other variations along those lines.

All of these tactics are based on manipulating the supply of – and, to some extent, even the demand for – a given item. All marketers know Economics 101: When supply is low and demand is high, prices go up.

Also, when something feels exclusive, hype builds, further driving up the perceived value. That’s part of the reason the latest iPhone or the hottest video game system always seems to have a production shortage just when people want them most.

To be clear, I’m not implying that these tactics are devious or underhanded. There are quality goods out there that can’t be mass-produced, and they should be priced accordingly. My aim is simply to make you aware of this specific and highly effective way that companies try to get you to part with your hard-earned money.

The Psychology of Scarcity Marketing

Scarcity marketing is effective in part because it plays on our innate sense of loss aversion. Most of us hate to lose something more than we like to win, a point famously proven by Nobel winning psychologists Amos Tversky and Daniel Kahneman.

I recently found out just how powerful loss aversion can be when my wife and I were searching for a home to rent on Airbnb.

After perusing the site for a while, we located a house we liked and started the process of checking out. Once we reached the final page of the checkout process, we paused, considering whether to put down a hefty deposit or keep searching for a better rental.

That’s when we noticed a pop-up message: “22 other people are currently viewing this property for these same dates.”

Before that pop-up, I could take the house or leave it. After I saw that message? I had to have it. I mean, this was a busy tourist season we were talking about. What if we didn’t get the place, and we ended up at a dingy motel on the outskirts of town?

If 22 other people were on the same page as me, one of them could book at any second! Then, I’d lose! The fact that so many others were interested in the property made me think it had to be a truly excellent house.

I entered my credit card information as fast as possible, happy to be “beating” those other folks.

I hope you can see the lunacy at play. One second, I didn’t even know there was competition. The next, I felt like I was in a race with 22 strangers to secure the vacation spot of my dreams.

While not everyone is hyper-competitive, I think the example elucidates just how effective a simple marketing tactic can be.

This same principle comes into play when buying just about anything online. Amazon will tell me that an old novel I’m interested in “only has two copies available!” When I book flights, Delta is constantly reminding me that the plane “only has three seats left!”

These little nudges create a subtle anxiety, pushing me to act just a bit more hastily then I might otherwise. As Harvard economist Sendhil Mullainathan says, “That’s [the] heart of the scarcity trap. You are so focused on the urgent that the important gets waylaid.”

Finally, perceived or real scarcity is a contributing factor in getting people to make ill-advised bets on financial bubbles.

Anyone with an interest in investing has witnessed the white-knuckle ride that bitcoin has been on lately. The once-obscure cryptocurrency rose in price by 1,800% last year.

A big factor in the rise was scarcity. Because only a finite amount of bitcoin can ever be made, some people treat it like digital gold. New money poured into bitcoin because people wanted to stake their claim on the scarce resource. The folks selling cryptocurrency-related services were more than happy to play up the scarcity aspect in order to whip people into a buying frenzy.

By all means, invest in bitCoin if you feel it has inherent value as the currency of the future. But investing just because you want a piece of something scarce makes little sense. My old Teenage Mutant Ninja Turtles sitting in my mom’s attic are scarce, but that does not make them valuable.

How to Stay Strong

In order to get better at making poised, rational, spending decisions, I highly recommend reading Trent’s post, “10 Questions to Ask Yourself Before Any Purchase.” In it, he lays out a strategy that is pretty much tailor-made to combat scarcity marketing.

The key is to carefully consider each and every purchase, as opposed to acting on impulse. Asking yourself questions such as “Have I looked for lower-cost alternatives?” and “Can I delay this purchase?” forces you to calm down and look at the situation in a more measured way.

If you run through a checklist of questions before making a purchase, you’ll be less likely to make a poor decision. Waiting 30 days can also be an effective way to sort fleeting urges from stuff you truly want.

Budgeting can also be very helpful. Just pick a budgeting style that works best for you and stick to it. If you’re diligent about buying only what you need or have saved up to afford, it’ll be easier to resist the siren call of the next great thing.

Summing Up

Scarcity marketing is real, and it’s powerful. But if we recognize its existence and do our best to make deliberate decisions when we encounter it, we can save some serious money.

The next time I feel pressured to buy an airline ticket because of seat availability, I will take the time to remind myself that there are 87,000 flights taking off in the U.S. every day. If I can’t find one that meets my specifications, I’m probably not trying hard enough.

Related Articles:

- 10 Useful Strategies for Learning Financial Self Control

- Money Can Buy Happiness – Just Not in the Way You Think

- Why Does Spending Cheer You Up? How to Break That Connection

The post Understanding This Marketing Trick Can Help You Avoid Impulse Buys appeared first on The Simple Dollar.

Source The Simple Dollar http://ift.tt/2GwXWdp

Help People Answer the Call of the Wild With This Work-From-Home Job

Hear the call of the wild from the comfort of your own home.

Aspira, which connects outdoor adventurists with parks, campgrounds and conservation agencies across the country, wants to hire remote customer service agents in 17 states: Alabama, Florida, Georgia, Idaho, Indiana, Kentucky, Maryland, Mississippi, New York, Ohio, Oklahoma, Pennsylvania, South Carolina, Tennessee, Texas, Virginia and Wisconsin.

The company promises there’s no cold-calling or commissions. It will also send you all the equipment you need for the job, except for a computer monitor, which you’ll have to provide yourself.

Pay is hourly based on location, but the posting does not indicate what the pay rate is or what your schedule might look like.

Not quite ready to take a walk on the wild side? No worries, you can find other jobs by checking our Jobs page on Facebook. We post new opportunities there all the time.

Customer Service Agents at Aspira

Responsibilities include:

- Fielding calls from customers, handling questions, requests and issues

- Assisting customers with camping and activity reservations, as well as hunting and fishing license requirements

- Attending initial and ongoing virtual training

Applicants for this position must have:

- Landline phone (no cell phones)

- Wired high-speed internet connection (no wireless)

- Quiet work environment

Benefits include:

- Bi-weekly paychecks

- Employee incentive program

Apply here for the customer service agent jobs at Aspira. Scroll through the open positions list to find the post for your area.

Tiffany Wendeln Connors is a staff writer at The Penny Hoarder.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2EtaFwQ

الثلاثاء، 30 يناير 2018

What to watch out for before getting a smart meter

Smart meters are the energy gadgets being offered and installed in every household that wants one across England, Scotland and Wales by 2020.

By the end of the programme, which began in 2016, around 53 million smart meters will be fitted in over 30 million premises, according to the government – which is spearheading the scheme.

But providers, consumers and industry bodies have reported problems with the roll-out.

Moneywise explores what’s happened and looks at whether a smart meter is right for you.

The benefits

A smart meter is a tool (or tools if you have gas and electricity) you can have installed in your home – usually where your existing meters are – which sends automatic digital meter readings to your energy provider.

This means bills should be far more accurate than at present, when they are estimated, and it saves householders from having to submit their own meter readings.

On installation, you’ll receive an in-home display gadget detailing how much gas and electricity you’re using, as well as the cost. According to the government, this will help households to manage their energy usage better, save money, and reduce emissions.

Smart Energy GB – the company communicating the smart meter roll-out – adds that smart meters will enable households with prepayment meters to top up their energy online or over the phone rather than having to go to a shop (although they can continue to do this should they wish).

Another point to consider is that some suppliers are offering their cheapest average tariffs to customers who take out smart meters with them.

According to energy comparison site uSwitch, British Gas and First Utility’s cheapest tariffs are only available to households that take out a smart meter with them. These tariffs, which cost £916 and £995 respectively per year, are not available to those who already have a smart meter.

However, while they are the cheapest average annual tariffs offered by these suppliers, they don’t beat the current cheapest deal on the market open to everyone, which is £807 from Outfox the Market.

There have also been some major issues with the smart meter programme. Here are the five key problems.

1. Not all households can get a smart meter to begin with

Moneywise spoke to 11 energy providers, including the Big Six. We found that some are installing smart meters to priority customers to begin with – such as to prepayment meter customers – while others are rolling out meters area by area, which means you may need to get in the queue.

Other providers exclude homes with prepayment meters or solar panels, although by 2020 every household will have to be offered a meter – see the table below for full details.

For example, SSE says: “Where customers need a prepayment meter, have two rate tariffs such as Economy 7 or a more unusual or complex meter, there may be a delay in getting a smart meter installed.”

{kind=link}

2. You may lose smart connectivity if you switch providers

While you can switch energy suppliers if you have a smart meter, many meters installed to date won’t send meter readings to your new provider, which means you’ll have to revert to manual meter readings and estimated bills until the problem is resolved.

The issue is that most providers have only installed first-generation smart meters – known as SMETS1 meters – and some of these can’t connect to the national smart meter communications network run by the Data Community Company (DCC). With British Gas, for example, SMETS1 meters will only continue to operate if you join from EDF, Scottish Power, Spark, SSE or The Co-operative Energy. Of the 11 providers we spoke to, only a few have begun trialling second-generation meters – known as SMETS2 – which will resolve this issue.

Only this month (January 2018), the Department for Business Energy and Industrial Strategy (BEIS) extended the starting point from which SMETS2 (second generation meter) installations will count towards suppliers’ targets from 13 July to 5 October, due to providers not being ready.

A BEIS spokesperson says: “We have taken this step to ensure that customers can continue to feel the benefits of smart meters and suppliers can be completely ready to roll out SMETS2. This will not affect the rollout of the programme, or the 2020 final deadline.

“Smart meters are a vital upgrade to our energy infrastructure and millions of people are already benefiting from them. They will provide accurate bills and save consumers £300 million in 2020 alone.”

Prior to the government’s SMETS2 extension, a spokesperson for Octopus Energy told Moneywise: “We are concerned that there are so many SMETS1 meters installed in the UK, which aren’t interoperable, and not a very long time period for SMETS2 meters to be rolled out.”

Energy regulator Ofgem says the DCC is planning to connect all SMETS1 meters to the network by mid-2019, but in the meantime, you’ll have to revert to manual meter readings and estimated bills.

Robert Cheesewright, director of policy and communications at Smart Energy GB, explains: “You can speak to your new supplier ahead of switching to find out whether your smart meter will be affected, but rest assured that you’ll always be able to switch, and if you have experienced some loss of smart functionality when switching supplier, this will only be temporary. Earlier smart meters [SMETS1] will be enrolled into the national communications network over the air, without the need for a visit from an engineer.”

3. You may experience delays in getting a smart meter

Households keen to have a smart meter installed may experience delays. Renewable energy provider Green Energy explains that as it’s a small energy provider, it needs to ‘piggy-back’ off Big Six orders for SMETS2 meters as it’s not cost- effective for manufacturers to supply the small number of meters it needs. Its chief executive, Doug Stewart, says he’s “hamstrung” by this reliance on larger companies making orders.

He explains: “There aren’t enough smart meters to go around and they’re slow to get hold of when you’re a smaller provider, plus there aren’t enough engineers to install them; we keep turning down customers. As an industry, I don’t think we’ve got a prayer of installing them by 2020.”

This worry of getting smart meters installed by 2020 is one echoed by other providers. British Gas’s parent company Centrica and Ovo Energy have both separately labelled the government’s target as “ambitious”.

A spokesperson for Scottish Power adds: “Due to the delays with the DCC becoming operational, the target dates will be a challenge for the whole industry.”

4. Energy bills may rise as a result

Centrica has called on the government to “address inefficiencies” in the programme to make it more cost-effective. It says the roll-out is “costly to implement” and adds “the equivalent of almost £40 on the bill of each Centrica customer”.

It also warns that forthcoming plans to cap energy bills could have “serious implications” for the smart meter programme, as it may result in there not being enough money to fund the rest of the roll-out.

5. Households pressured into to getting a smart meter

Households are being unfairly pressured into getting smart meters, according to complaints received by Citizens Advice, which runs the Chartered Trading Standards Institute (CTSI) helpline.

Issues seen by the CTSI include households being given so-called ‘deemed appointments’ – where suppliers say they’re coming to install smart meters without giving consumers a chance to opt out.

Other complaints include communications about smart meters omitting the fact they’re not compulsory.

As a result, the CTSI has written a letter to industry body Energy UK asking it to remind suppliers not to give the impression to households that smart meters are obligatory. The organisation is concerned suppliers may be breaching the Consumer Protection from Unfair Trading Regulations 2008.

Steve Playle, lead office for energy at the CTSI told Moneywise: “The industry is under great pressure to install meters by the 2020 deadline, but they’re slipping behind, and as such, they’re finding more and more ‘interesting’ ways to get people to sign up.”

The CTSI has the power to launch criminal prosecutions against rule breakers.

Victoria MacGregor, director of energy at Citizens Advice adds: "We are concerned that some companies are using aggressive sales practices to install smart meters. People have come to Citizens Advice for help because their energy supplier has said they’ll force entry to install a smart meter, or told them that they are required to have one.

"Smart meters are not compulsory and customers shouldn't feel pressured to have one installed if they don't want one.

"We appreciate that suppliers are under pressure to install more smart meters but they have a responsibility to act reasonably towards their consumers and not to use misleading or aggressive sales practices."

Moneywise has also seen reports of such behavior by energy suppliers. One text we’ve seen, which was sent to an Npower customer who wishes to remain anonymous, said that the provider was due to install a smart meter without the customer requesting one, and without stating that the scheme isn’t compulsory or how to opt out.

The text message says: “Hello! We are due to attend your property on behalf of Npower to fit Smart meters on 30/01/2018. Please call us today on [number has been blanked out by Moneywise] to confirm or rearrange your appointment.”

On raising this with Npower, it told Moneywise: “While smart meters bring many benefits to consumers, they are not compulsory and customers are not forced to have one. Customers who are offered an appointment but don’t want a smart meter can contact us to cancel their appointment.

“This specific message relates to a reminder to the customers who have not confirmed, rescheduled or cancelled an existing appointment. These are sent via SMS or email as part of the follow up process.

“When the initial appointment communications are sent via the customer’s preferred channel, they are given options on how they respond to the proposed appointment date and time, including the option to cancel the appointment.”

However, while Npower says the message is a follow-up text, the reader is adamant that it was the first communication they’d received on smart meters. About a week later they did receive a follow-up email from Npower, which again Moneywise has seen. While this did contain more information about smart meters, again it only gave the customer the opportunity to ‘confirm’ or ‘change’ their appointment – not to cancel it.

When we raised this issue of customers being pressured into getting a smart meter with energy regulator Ofgem, it told us suppliers must treat customers fairly and be “transparent and accurate”. However, it has no open investigations into domestic smart meter wrong-doing at the time of writing.

An Energy UK spokesperson says: “Energy companies are committed to meeting the government’s deadline of ensuring all households and businesses are offered a smart meter by 2020.

“Energy companies will be adopting various methods of communication with their customers to increase engagement and enable as many people as possible to experience the benefits that smart meters bring.

Section

Free Tag

Related stories

Source Moneywise http://ift.tt/2DNeZtO

St. Luke's leasing new Stroudsburg property

STROUDSBURG — St. Luke's Hospital is moving into the building vacated by Northwood Urgent Care, across Route 611 (North Ninth Street) from the Pennsylvania Department of Transportation facility."St. Luke’s is considering the space for a family practice and possibly other medical uses," said Sam Kennedy, Corporate Communications director for St. Luke’s University Health Network.The building sits on one of three adjoining parcels totaling 14.3 acres. [...]

Source Business - poconorecord.com http://ift.tt/2GvyDIB

Source Business - poconorecord.com http://ift.tt/2GvyDIB

How to Hire a Virtual Assistant for Your Business

By Holly Reisem Hanna If you’re anything like me, you launched your business with the idea that you would be able to spend more time with your family, but as time goes on and your business grows the more administrative tasks that end up on your plate. Now you have less time to focus on […]

The post How to Hire a Virtual Assistant for Your Business appeared first on The Work at Home Woman.

Source The Work at Home Woman http://ift.tt/2DJn5j5

Why Now Could Be a Great Time to Ask Your Insurers to Lower Your Premiums

Insurance can really save the day if you’re in a car accident or your neighbor’s stupid tree falls on your garage.

But until you need it, it’s a giant pain in the butt.

Those premiums you pay seem like a monthly or quarterly flushing of money down the toilet. That’s why there are so many insurance companies telling you they have the best rates.

Now, thanks to the new tax code, your premiums should go down, according to two consumer watchdog groups.

Do Corporate Tax Cuts Mean Lower Insurance Premiums?

According to Consumer Affairs, the new laws that cut corporate taxes from 35% to 21% mean big profit boosts for some of the country’s largest companies.

Some companies have stepped up and are handing out bonuses or wage increases to their employees. Nice.

Last year’s Fortune 500 list included 20 insurers. These companies are poised to cash in on those new tax breaks.

But the Consumer Federation of America and the Center for Economic Justice let them know it’s not that simple in a letter to the insurance commissioners for all 50 states and Washington, D.C.

Your insurance premiums — home, auto, health… all of them — are calculated to include a provision for profit for the insurance company based on the after-tax rate of return.

The letter says insurance companies are legally required to lower those rates now that they will be earning more by paying lower taxes.

Each state regulates the insurance rates within their own borders. A department of insurance, or a similar body, monitors insurance rates to ensure they are not excessively high or low, or discriminatory.

Will state insurance commissions agree with the Consumer Federation of America and the Center for Economic Justice? We don’t know just yet.

The letter tells insurance commissioners that premiums should be lowered by approximately 5%. California’s commissioner has tasked his staff with reviewing rates to keep them within the legal parameters. So far, he’s the only state insurance commissioner to make a move.

Yes, You Can Negotiate Your Insurance Rates

If your state doesn’t put pressure on your insurer, you may be able to negotiate your rates yourself. Now that you know insurance companies are making extra profit — a lot of it — you may be able to use that knowledge to lower your premiums.

If your current company won’t do it, it may be time to shop around. The new laws may also allow competing companies to offer deals that are far better than what you saw a year ago. Don’t be afraid to tell your current insurer that you’re willing to jump ship and switch to a new company. This threat could be just the push your insurance company needs to cut your premiums now.

Don’t skimp on your coverage just to save money, though: Insurance is a godsend when you need it. You need the right level of insurance coverage, but why not pay as little as possible to get it? Those insurance company CEOs don’t need another yacht.

Tyler Omoth is a senior writer at The Penny Hoarder who loves soaking up the sun and finding creative ways to help others. Catch him on Twitter at @Tyomoth.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2DPaizP

Need a Full-Time, Paid Internship? The Obama Foundation is Hiring Right Now

College internships are a great way to get your career off the ground, and may even land you a job before you graduate.

If you’re a college student looking for a summer internship, this high-profile opportunity could be just what you’re looking for.

The Obama Foundation is hiring full-time paid interns in its Chicago, Illinois, and Washington, D.C., offices.

If you’re pursuing a legal career, the Office of the General Counsel at the Obama Foundation is also accepting applications from law students to intern for either the Summer 2018 or Fall 2018 term.

You’ll have to act fast, though — both application windows close on Feb. 12 at 5 p.m. Central Time.

Paid Internships at the Obama Foundation

According to the job description, summer 2018 interns “will play a key role in providing departments at the Obama Foundation with the administrative, logistical, and operational assistance needed to execute their work.”

Compensation:

Summer 2018 interns will receive a $1,500 stipend and will be compensated for up to $1,500 in expenses directly related to the internship, for a total of up to $3,000.

Eligibility Requirements:

- Availability to work 40 hours per week in the Chicago or Washington, D.C., office

- Availability to work from May 29 – Aug. 17 (If you are a student on the quarter system, your summer internship will run from June 18 to Sept. 7)

- Be an undergraduate or graduate student at the time you apply

- Be at least 18 years old when the internship begins

- Be able to legally work within the United States

- Fluency in spoken and written English

- Strong writing and researching skills

- Excellent time management and organizational skills

Apply here for summer 2018 paid internships at the Obama Foundation.

Lisa McGreevy is a staff writer at The Penny Hoarder. She loves telling readers about new internships so look her up on Twitter (@lisah) if you’ve got a tip to share.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2DOgqEB

Something to Smile About: Free Dental Services for Kids in February

Taking your kids to the dentist might elicit a groan or grumble.

But if that dread is coming from you — over the cost of dental care — and not your children, you might want to check if a local dental provider is participating in this year’s Give Kids A Smile program.

Thousands of participating dental providers across the country will be offering free services for a day as part of Give Kids A Smile.

This year’s program kicks off February 2, but not all participating providers will offer free services on that day. Many providers will host their events sometime in February, during National Children’s Dental Health Month.

You’ll want to check with your local participating provider to find out when their event will be held, what services will be provided and who is eligible to receive the free services.

For example, the Florida Department of Health in Pinellas County (near where The Penny Hoarder is headquartered) is a participating provider near me. Dental professionals will provide free exams, X-rays, cleanings and sealants on February 19 starting at 8 a.m. to uninsured children and teens from age 4 to 18 — as well as those on Medicaid.

Check the Give Kids A Smile program’s 2018 list to see which provider or organization is participating near you. More than 6,600 dentists have pledged to take part in more than 1,300 free dental events this year, serving approximately 290,000 children.

You can also get information about participating providers by calling 1-844-490-GKAS (4527) Monday through Friday from 8:30 a.m. to 6 p.m. CST.

In addition, the Give Kids A Smile Facebook page has information about related events.

Nicole Dow is a staff writer at The Penny Hoarder. She enjoys writing about parenting and money.

This was originally published on The Penny Hoarder, which helps millions of readers worldwide earn and save money by sharing unique job opportunities, personal stories, freebies and more. The Inc. 5000 ranked The Penny Hoarder as the fastest-growing private media company in the U.S. in 2017.

source The Penny Hoarder http://ift.tt/2Gs8JW5

الاشتراك في:

التعليقات (Atom)