الأربعاء، 31 يوليو 2019

Fed Cuts Key Rate in Its First Reduction in More Than a Decade

Source CBNNews.com https://ift.tt/2KtBBjR

Thoughts and Strategies for Handling Ethical Shopping Dilemmas

A few weeks ago, while Amazon was running its Prime Day event, a few readers contacted me and asked me not to talk about the event in any detail because of ethical concerns they had about Amazon and their business practices. I wasn’t planning on covering the sale with much depth anyway, so it wasn’t an issue, but it did leave me thinking about the issue of balancing ethical shopping with good personal finance practices, an issue that’s been dangling in my mind for years.

I attempted to make a list of ideas, principles, and strategies regarding this difficult topic and, after a while, I realized that the core ideas I have to share actually just make up a fairly small list, so let’s just dig right in, shall we?

Everyone has different ethics and values, so it’s very difficult to make broad recommendations about ethical shopping. The reality is that different people care about different things and value different things more highly than others. We all largely agree on the set of things that are right and wrong, but which thing is more right? Which thing is more wrong? We can argue about that forever, especially when we’ve come to a consensus on some of the true black and white issues.

Take the Amazon issue that spurred this article, for example. Some readers were bothered by issues with Amazon’s warehouses and employee treatment. Others were bothered by the waste generated by shipping.

Those are both valid concerns, but they’re not necessarily high priority concerns for everyone. If I were to offer a blanket statement of “don’t shop at Amazon for these ethical reasons,” that turns the issue from good practical personal finance advice into promotion of my own ethical views. I am far more interested in giving people practical tools so they can make their own judgments than imposing my judgments on others.

So, what are those practical tools?

Know who you’re buying from. If you’re giving your money to a particular business, either a retailer or a manufacturer, it’s worth your time to spend a few moments learning about who you’re buying from in terms of the issues you care about.

If you do a bit of investigation into any sufficiently large company, you’ll likely find some issues that concern you. The question is whether or not those issues concern you enough to not be a customer of that business or that manufacturer, and that’s up to you and your personal ethics.

There are a handful of companies out there that I never want to shop from or own products made by them for specific ethical reasons, but my reasons for doing so are in line with my own values and the things I care about. I also have a second tier of companies I prefer not to do business with unless there’s not a reasonable option, and, again, my reasons are my own. I am not a perfect database or repository of information about companies, nor do my values likely perfectly match your own.

That being said, I understand that most companies out there do have some sort of ethical issue if you look close enough, whether it’s something related to how they treat employees or how they distribute products, and once a company grows to a reasonable size, it’s almost a guarantee that you’ll find complaints about their behavior. It’s very difficult to find a “perfect” company. You simply have to decide for yourself what level of corporate behavior you’re okay with, and that varies a lot from person to person.

Research the company and make up your own mind. Don’t expect perfection, but it’s perfectly reasonable to have some companies that you don’t wish to give money to, and understand that other people may have other distinctions and other issues they prioritize. Also, recognize that one giant corporation with some bad spots on their reputation may not be any worse than another giant corporation with a more clean reputation; they may just have worse public relations and marketing.

I actually prefer a different approach.

Rather than focusing your energy on taking your spending away from an unethical business, focus your energy on taking spending to an ethical business. I am far more interested in companies that do things well than I am in companies that do things poorly. I would prefer to take my business to a company that treats employees well than take my business away from a company that doesn’t. I am less interested in boycotting than in simply choosing to spend my money at a great business.

For example, I like to see companies that make reliable products. I like to see companies that treat their employees well. I like to see companies that take solid steps toward environmental responsibility. I like to see companies that expect some of these standards from companies in their supply chain.

To me, this is a positive approach to ethical spending. If you have $X to spend and you take that $X to a business with practices you’re happy with and use it to buy products from a manufacturer you’re happy with, then that’s a much better approach than taking money away from a company you’re unhappy with and merely spending it with a similar company that may be doing the same things but you don’t know about them.

In other words, I don’t usually try to go out of my way to avoid companies with mediocre or even somewhat negative reputations. Instead, I try to take my business to businesses with positive reputations if they’re available to me.

But what about the cost? Often, buying from a more ethical company with good employee and business practices and good products means that the sticker price is going to be higher. How does one solve that issue?

My approach is simple. A personal commitment to spending less overall and being careful about your purchases means that you have more breathing room to be ethical about your purchase. Part of the reason that people tend to balk at paying anything higher than the lowest possible price for something is that they want to simply buy more and more things. If you pay $80 for something at one retailer versus $100 at another retailer, that’s $20 in your pocket. If two retailers charged the same amount, then, sure, the person is likely to go to the more “ethical” retailer, but if one retailer offers lower prices, that means they can fill up their cart with more stuff or have more cash left over for other things.

But what if your approach to spending wasn’t to fill your cart up with more stuff? What if you ideally didn’t want to buy new things at all unless they filled a genuine need in your life? What if you consistently used a strong mental toolbox for avoiding unnecessary purchases? That would leave you with a much greater ability to be ethical in your shopping behavior.

In the end, I am going to suggest one single concept that I think is a very strong idea in terms of ethical buying for almost everyone.

When in doubt, buy from the more local source so that money stays in your community and thus supports other local services. Buy from the business that’s owned by a local person that employs lots of local people. Buy from the smaller chain that’s only got a handful of locations, all in your state, instead of shopping at MegaloMart.

That kind of choice might cost you a little more, but it means that a much larger portion of your spending dollar stays in your community and state. The taxes paid by those employees and business owners are going to go toward things that help you, and it’s going to make sure that people stay employed in your town.

Not sure what’s truly local? This circles back to doing the research into who you’re buying from and what you’re buying. Find out about those businesses. Who runs them? Do they operate ethically? Understand that no business is perfect, but look mostly toward businesses that try to operate in a good manner rather than away from businesses that you find negative reports about.

Good luck!

The post Thoughts and Strategies for Handling Ethical Shopping Dilemmas appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/2YzjuBR

How to Build a High-Converting FAQ Page on Your Website

FAQ pages represent a crucial component of the customer conversion funnel. Anyone who lands on this page has already identified the need for whatever you’re selling and is now entering the consideration phase of the purchase process.

Your FAQ page can provide them with the information required to finalize their buying decision.

However, I see so many websites that overlook the importance of this landing page. I read lots of FAQ pages that sound more like an afterthought, as opposed to a page that’s been designed to drive conversions.

FAQ pages must have a purpose. Don’t just add one to your website because you feel like it’s a requirement and you want to fill up space.

While most websites should have a FAQ page, yours could be doing more harm than good if it doesn’t have any clear intentions. It’s possible that your FAQ page is driving people away from buying, as opposed to drawing them in. Obviously, you don’t want that.

For those of you who are currently neglecting your FAQ page, it’s time to make changes. The rest of you might not have an existing FAQ page and want to add one from scratch.

Regardless of your situation, you’ve come to the right place. I’ll show you how to address common problems with FAQ pages and learn how to optimize them for conversions.

Ask the “right” questions

I’ve seen plenty of FAQ pages that have a great design, layout, and optimal user experience. But to be blunt, the questions are awful.

Somewhere along the line, so many sites have lost the meaning behind frequently asked questions.

Anything related to where your company was founded, how many employees you have, or where your CEO was born does not belong here. You can include details about the history of your company on your about us page. I have a separate guide on how to create an impactful about us page on your website.

But adding irrelevant or useless questions and answers to your FAQ page is just going to confuse your visitors.

They’ll end up having a more difficult time finding information that will answer their actual question. So you need to have questions that are more related to conversions.

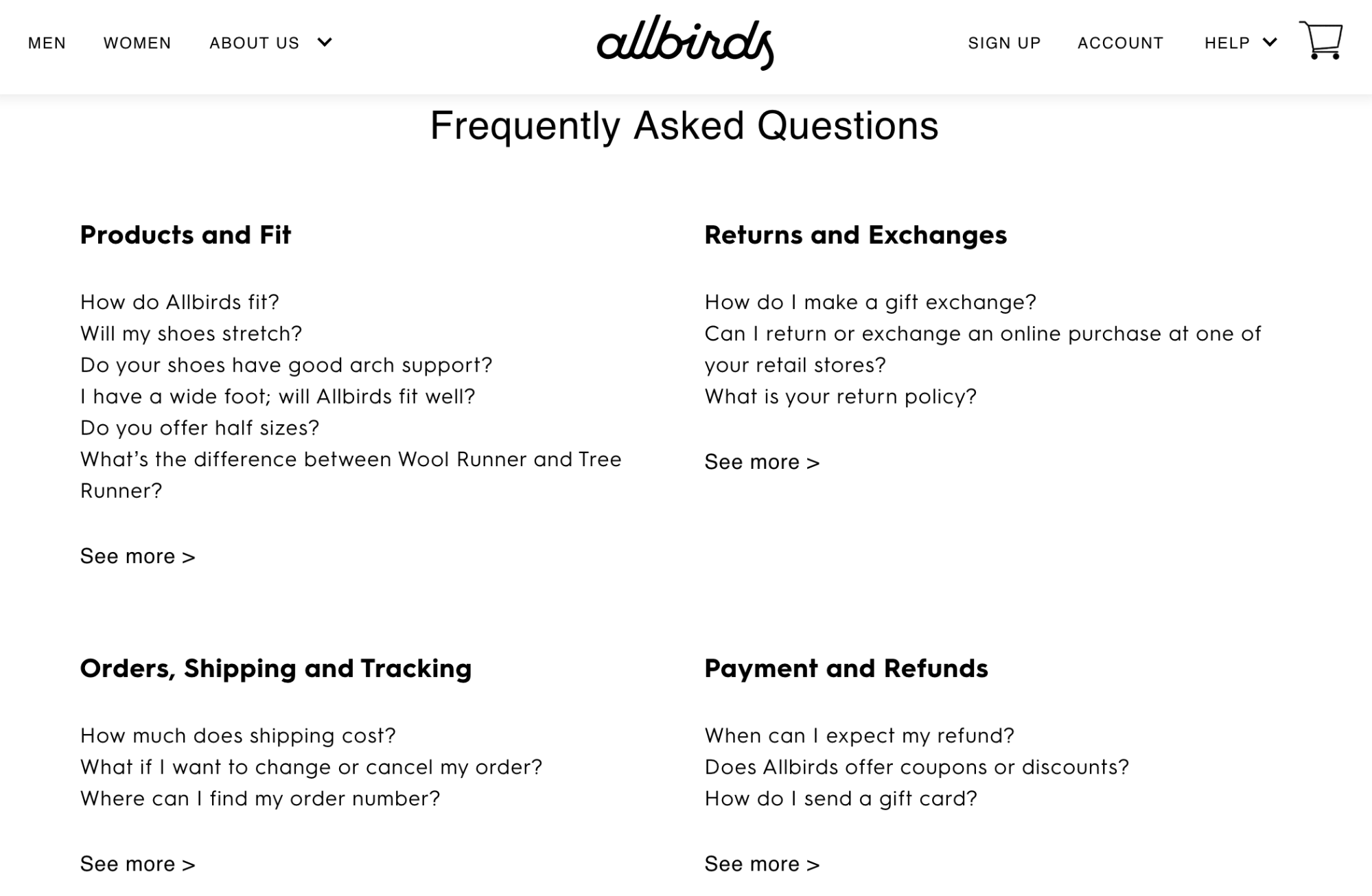

Check out some of the questions on the Allbirds FAQ page.

This company has an ecommerce platform for selling shoes direct to consumer. So all of the questions are intended to drive sales.

They have questions related to how the shoes fit, sizing, returns, exchanges, refunds, and shipping. All of these are important to the consumer buying decision.

Allbirds does not offer half sizes in their shoes, which is definitely something that might throw some of their shoppers off. But they have questions directly made to address this potential concern.

Do you offer half sizes? Will the shoes stretch? Do the shoes fit a wide foot?

These are all logical questions that someone would ask before buying. You want your customers to feel confident when they’re shopping.

Buying a product, such as sneakers, online can be a challenge. Customers don’t get a chance to try on different sizes, walk around, and see what feels good like they would in a store.

But Allbirds alleviates any uneasiness by asking the right questions on this FAQ page.

If you’re still unsure about how to ask the “right” questions, just see what your customers are actually asking. Take a look at questions and comments from:

- Submission forms

- Customer emails

- Live chat

- Social media comments and messages

- Phone support

Keep a database to track all of these questions and group similar ones. If lots of people are asking the same thing, it definitely belongs on your FAQ page.

Simplify the navigation

Like the rest of your website, Your FAQ page must be frictionless.

You might have great questions and answers, but if your site visitors can’t find them, then your FAQ page is going to fail.

Do your best to try and emulate an in-person shopping experience. If a customer was in a physical store, all they would need to do is find an employee and ask their question. Sure, sometimes that employee might direct the customer to another department or something like that. But in the end, the question is answered directly and timely.

Don’t make people hunt for answers on your website.

If the format of your FAQ page is just questions followed by answers repeating all down the page, visitors will have to keep scrolling to find what they’re looking for. This is not ideal. They might even overlook their question, which wouldn’t solve their problem.

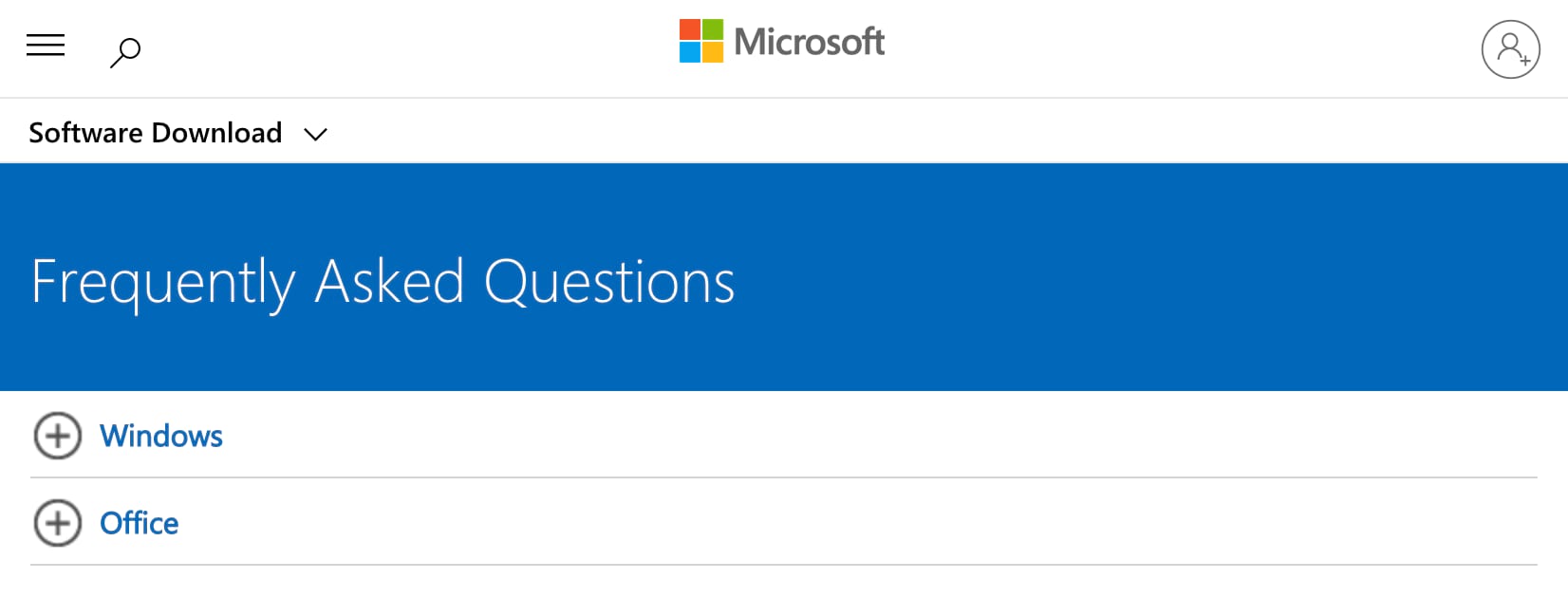

Take a look at how Microsoft simplifies things on their FAQ page for software downloads.

Right away, you’ll see that there are two categories to choose from.

So the website visitor can narrow the results depending on if their question is related to Windows or Office. That way any Office questions won’t have irrelevant Windows questions that need to be sifted through.

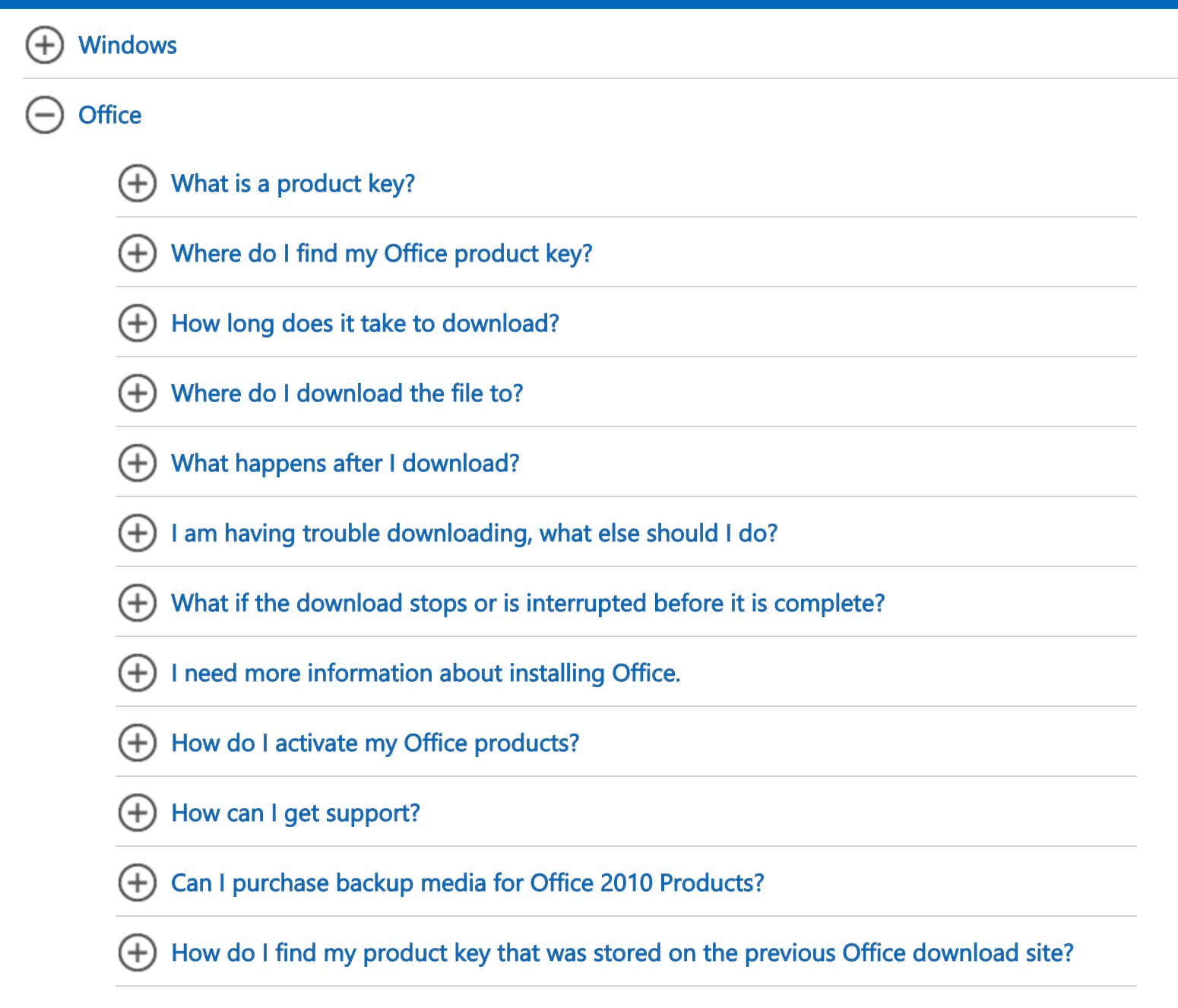

When a user clicks on one of the options, the menu expands, without redirecting to a new page.

Here’s what it looks like if I click on Office.

All 12 questions can be read without having to scroll. This makes it extremely easy for people to find exactly what they’re looking for.

Now, imagine if there was an answer directly below each of these questions. It would take up probably four or five times the amount of space on the page.

That layout would be much more challenging and require additional scrolling and text to read through. But this approach by Microsoft is clean and simple.

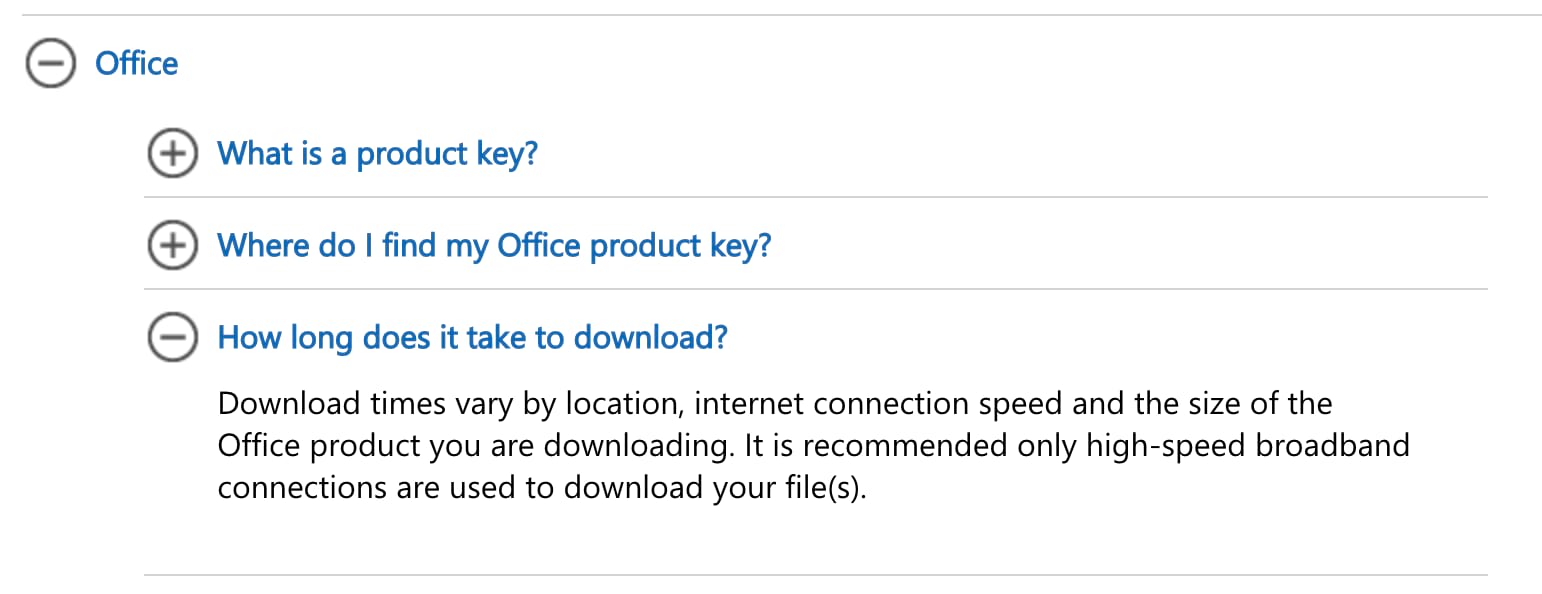

If you want to know something specific, like how long it takes for software to download, just click on the question and the answer will expand below it.

Frictionless.

If a site visitor has multiple questions, it’s still easy for them to navigate and find answers to everything.

Here’s the way you need to look at your FAQ page. If a site visitor has a question and it does not get answered, they aren’t going to convert. It’s that simple.

So if you approach your FAQ page trying to design the navigation in a way that’s optimized for user-experience, then it will increase the chances that people will find what they’re looking for.

Keep the answers short

Another common mistake that I see made on FAQ pages is the length of the answers. Everything needs to be clear and concise.

For the most part, your FAQ page should be fairly broad. You want everything to appeal to as many people as possible.

So you won’t have super-specific questions that require in-depth explanations.

But even for a general question that most people would ask, you still need to keep the answer concise. You don’t need to answer everything. Certain details can be left out.

I’d rather see FAQ pages with 30 questions that have short answers, as opposed to 15 questions with long answers. So if you currently have long paragraphs on your FAQ page, see if you can take one question and break it down into two or three.

This will provide a much better user experience.

Visitors shouldn’t have to read through an essay or short blog post to get a simple answer.

Let’s say that a website visitor is able to locate their question and ends up reading through a long answer. They might end up having additional questions, based on the length and details of that answer. You don’t want that to happen.

So sharpen your writing skills and only include the most important information related to the question.

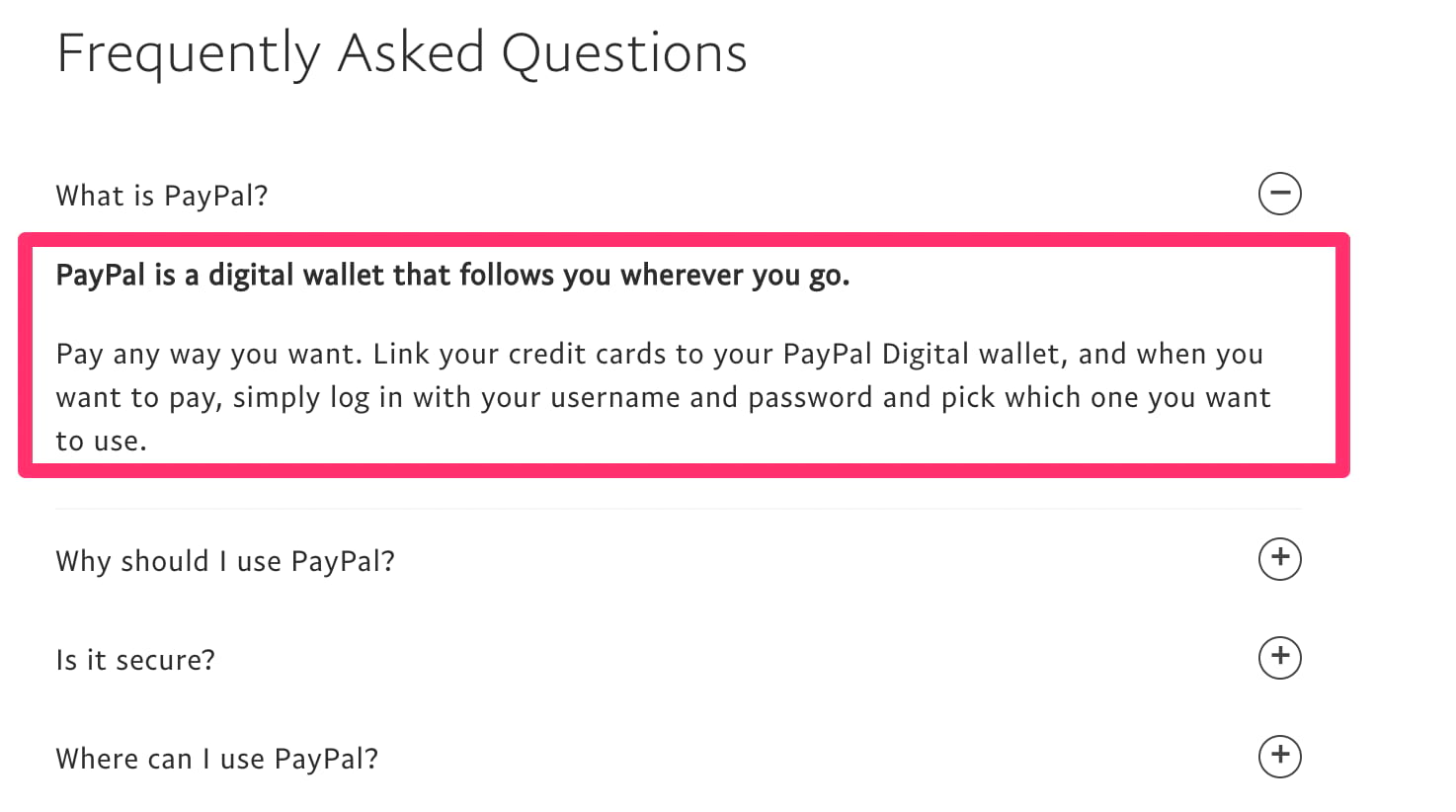

Check out this example from the PayPal FAQ page.

Look at the first question—what is PayPal?

Talk about a loaded question. PayPal is so many different things. They offer services for businesses, consumers, and websites. They could probably answer this question in 50 pages if they wanted to, going into details comparing PayPal and Stripe for ecommerce.

But no, they take a much simpler approach. The entire answer is just three sentences.

If they got into all of the specific details of PayPal, what it is, what it does, and who it’s for, it would only confuse the initial question. The answer above is clear, concise, and still answers the question.

Offer added support

While a FAQ page should be written to help most of your website visitors with broad questions, sometimes it’s just not enough.

No matter how good your questions are, how great the answers are, or how simple the format is, some people will still need additional assistance. That’s OK.

If it’s going to take a little bit of extra support to get people to convert, then give it to them.

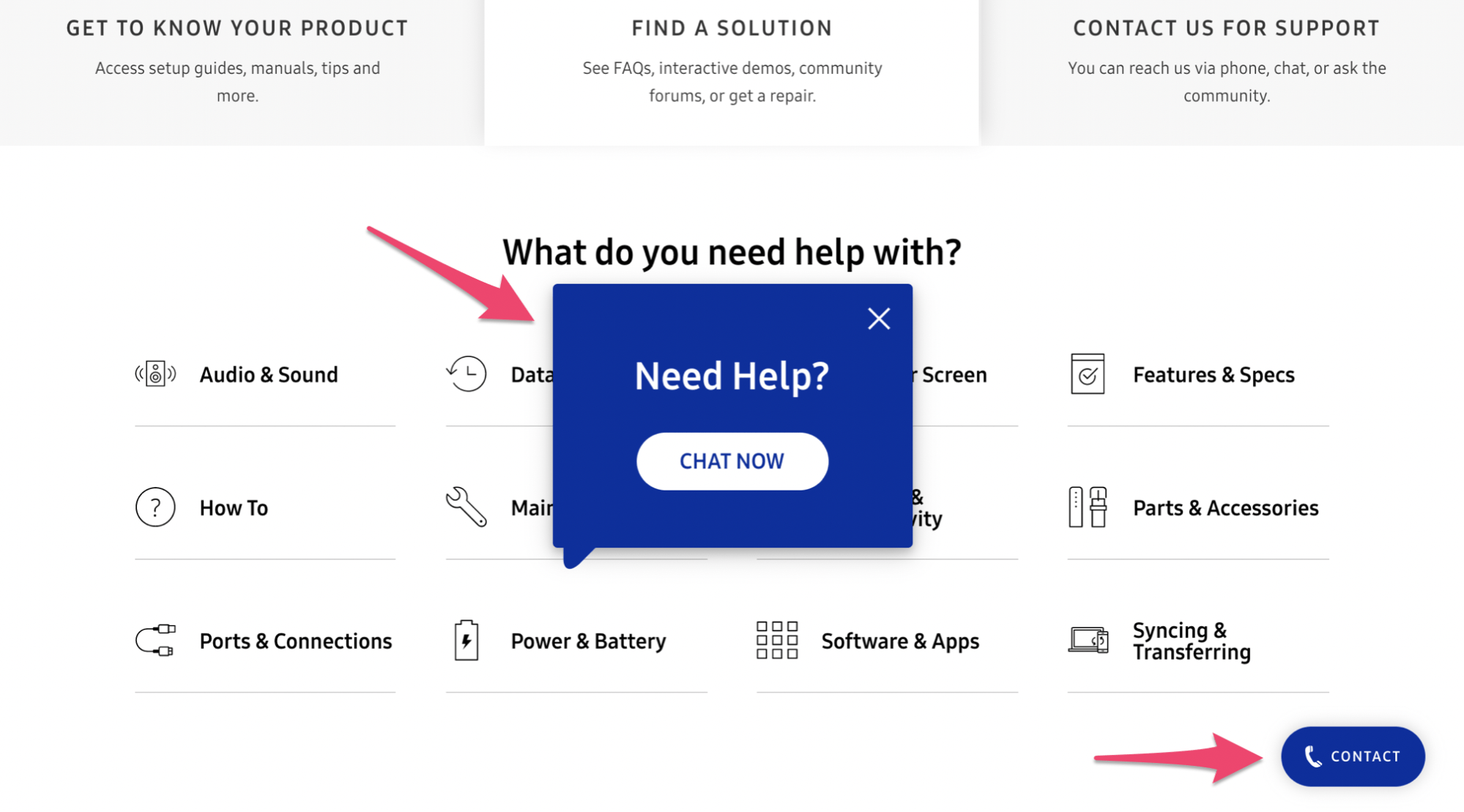

Just make sure that all support options are available. Here’s how Samsung approaches this on their FAQ page.

The first thing I noticed when I landed on this page was the list of categories. Samsung is a huge company, so it makes sense for them to start this way.

But as I stayed on the screen without making any actions for a while, this pop-up window appeared prompting a live chat session.

They obviously have this triggered to appear whenever someone doesn’t scroll or click since the implication would be that they can’t find what they’re looking for. I love this approach.

It’s much better than forcing the site visitor to go back and find another support page or make them go through countless questions manually until they find an answer. That’s just too many added steps.

Put a live chat window directly on your FAQ page.

Furthermore, Samsung has a phone support button in view at all times as well, as I pointed out in the screenshot above. So the customer has options.

Can’t find a solution on the FAQ page? No problem. Just pick up the phone or speak with one of our live chat representatives. This strategy should be incorporated into your FAQ page if you want to drive as many conversions as possible. The extra effort will go a long way.

Optimize for SEO

When you’re crafting a high-converting FAQ page, you need to keep the big picture of your website in mind. Nothing screams big picture louder than SEO.

For the most part, FAQ pages are designed with the idea that a visitor will land somewhere on your website, have a question, and then navigate to the FAQ page. In many cases, this very well might be the case.

However, you can set up your FAQ page to get traffic directly from organic searches as well.

So every question doesn’t need to be brand-specific. For example, let’s say your website offered web hosting plans for small businesses. Your FAQ page could ask, what is shared web hosting?

This question isn’t exclusive to one of your products or services. But it’s definitely something that one of your prospective customers will search for online. Your question could end up in the SERPs, driving more traffic to your website, and ultimately leading to conversions.

A great tip for finding SEO questions is to just use Google.

Let’s say you sell sneakers. Type in keywords that you’re trying to rank for, like “sneakers for travel,” and then scroll to the bottom to view related searches.

Based on these search suggestions, you can get SEO-inspired questions for your FAQ page.

So you can add questions related to shoes for walking all day or stylish shoes for Europe.

Another way to improve your SEO is by creating dedicated landing pages for your questions. Now, this slightly contradicts what we talked about earlier in terms of user experience. Redirecting people every time they want to see a new question could be a bit annoying.

However, these dedicated landing pages that interlink with each other can give you a boost in terms of SEO, if your website architecture and sitemap are optimized properly.

Conclusion

FAQ pages are critical resources for your website visitors.

Anyone who lands on this page is on the verge of converting. Sometimes getting a question answered is all it takes for them to finalize a decision.

So stop wasting time and space with FAQ pages that don’t add real value to your site.

Focus on questions that are related to conversions. Keep the user experience in mind by simplifying your design and writing concise answers. Offer additional support options for people who still have questions. Go the extra mile and optimize your FAQ pages for SEO.

If you follow the tips that I’ve covered in this guide, you can turn your FAQ page into a conversion machine.

Source Quick Sprout https://ift.tt/3310yvh

Fund briefing: Emerging markets

Source Moneywise - 29 years of helping you with your finances https://ift.tt/2yo7bd7

“How should we invest to pay for our children’s university education?”

Source Moneywise - 29 years of helping you with your finances https://ift.tt/2MuknFE

Should we transfer our rental property into joint names?

When we moved, we decided to rent out our old property rather than sell. As I was a higher-rate taxpayer we transferred ownership to my husband. He took out a mortgage on the property in just his name. The property has been rented out since then.

We’re now considering putting it back into joint names as we are both retired and only have my occupational pension and the rental income. Neither of us is a higher-rate taxpayer any more. My husband’s tax-free allowance covers the net income on the property virtually every year.

We’re not looking to sell for the next few years but may do so in the future. Is it worth our while making this transfer and what are the likely costs and consequences?

Yes, putting the property back into joint names or to ‘tenants in common’, owning 50% each as opposed to owning it in joint names, is a good idea because gifts between spouses are exempt from CGT. When you do sell the property, you will be able to offset your husband’s and your own annual CGT allowances (£12,000 each in 2019/2020) against the sale proceeds.

You could possibly inform the Land Registry of your intentions without incurring any legal costs, but I’d suggest that you speak to a solicitor to make sure that everything is handled properly.

While you are there, this would be a great time to review your wills to ensure that should you die before selling the property, your intentions of how it should be passed on are clear.

If you split the tenancy into a 50/50 (or other) percentage ownership, this also means that on the first death you could pass on the deceased partner’s share of the property to someone other than the surviving partner. Depending on your circumstances, this can be really helpful for IHT planning.

Owning the property in different percentages can also be helpful for income tax planning while the property is rented. This is because you can assign more income to a lower earner and potentially save some income tax legitimately.

While I wouldn’t expect this work to be more than a few hundred pounds, do get some quotes from a few solicitors and read their reviews before you make your decision on who to use.

Source Moneywise - 29 years of helping you with your finances https://ift.tt/2ypjuWr

الثلاثاء، 30 يوليو 2019

After Hackers Stole 100M Users' Info from Capital One, Here's How You Can Tell if Online Church Giving Is Safe

Source CBNNews.com https://ift.tt/2SWBdOr

A Mental Toolbox for Avoiding Unnecessary Purchases

Jeremy writes in:

You have mentioned before that when you’re considering buying something, you put it aside in a list and think it through before buying it by looking for flaws in the item. Can you explain how exactly you think it through?

First, let’s start with looking in detail at how I handle non-essential purchases (things I don’t strictly need).

If I don’t need something and I’m considering buying it, I put it on a list that I keep on my phone. I just type in what it is and add an online link if there’s one available.

Sometimes, if an item isn’t too expensive and I haven’t spent much of my incidental/hobby money for the month, I might just go ahead and buy the item spontaneously. I budget a certain amount for my hobbies and for such purchases each month and so some smaller purchases will come out of that money in a spontaneous way, but that’s the exception rather than the rule. An example of this: recently, I bought a couple bottles of seasoning at Trader Joe’s that we really didn’t need. I just wanted to try them out and they weren’t too expensive. I didn’t add them to any list – I just bought them.

At the start of each month, I add a big dotted line at the bottom of this list to indicate a fresh new month. I also delete the highest dotted line in the list.

So, let’s say I have a list that looks like this:

Item 1

Item 2

Item 3

———-

Item 4

Item 5

Item 6

———-

Item 7

Item 8

Everything above the first line is something I first jotted down before the first of last month. If this were late July, everything above that first dashed line was put on my list before June 1. Everything in that section is okay to buy if I find it at a good price. I’ve given it enough time and consideration.

Everything between the first and second line is something I jotted down during the previous month. Again, if this were late July, I jotted it down sometime in June. I don’t buy things from that section.

Everything below the second line is stuff I added this month. I don’t buy things from that section either.

At the start of the month, when I add a new line at the bottom, I delete the first line. So, on August 1, my list would now look like this:

Item 1

Item 2

Item 3

Item 4

Item 5

Item 6

———-

Item 7

Item 8

———-

I’m simply looking for a really good price on the first six items, but the other two are still in a holding pattern.

Every few days, when I have a bit of downtime, I go through the items on this list, from top to bottom, ignoring the dotted lines. I try to convince myself not to buy each of those items, and if I realize it’s a bad idea – or if I just come to an item and realize it doesn’t have any interest to me – I delete it. Sometimes, if it’s a small item that seems like it’d be fun but really unnecessary, I will stick it on my Amazon wishlist, which some relatives use for holiday gift-giving occasions. I often wind up with a bunch of sauces and other things like that on there.

This is the thought process I go through when evaluating each item. My goal is to find reasons not to buy the item, so that the stuff I buy is stuff that’s really purposeful and useful. You can apply this thought process to any purchase you’re considering, whether in the heat of the moment or reflecting on it later.

My Toolbox of Questions for Eliminating Unnecessary Purchases

I ask myself the following series of questions whenever I’m thinking about a potential purchase on my list.

Is this item of reasonable quality? If I’m actually going to buy something I don’t need, I generally don’t want the “junk” version of it that will barely meet my needs. If I go and look at comparative reviews of items like this one, does it score at least reasonably well?

This usually spurs me to look at reviews of the item to make sure that it compares well to similar items and doesn’t have any notable flaws.

Is this item durable? One key element I always look for in reviews is whether an item is durable or not. For newer products, this is hard to tell, so what I’ll often do is go back and look at previous similar products from that company as well as the company’s overall reputation.

For the most part, companies that have worked to cultivate a reputation for making well-made, durable, reliable products make well-made, durable, reliable products. I trust socks made by Darn Tough, for example. I trust Lodge to make cast iron items. In terms of bang for the buck, I trust cars made by Toyota. In each of those cases, I can’t necessarily know how reliable and durable their products are in the current model year, but I can rely on the company’s reputation.

Is this item easy to flip to someone else to recoup much of my cost if I decide it’s not for me? Does it depreciate slowly? I’m more likely to spend my money on an item that depreciates very slowly than an item that’s going to lose a lot of value quickly or wear out quickly.

I’ll poke around the secondary market for a particular item and see what it sells for. I’ll also look at the secondary market for similar items, particularly older ones, and see whether the price has held up.

Will this item take up a lot of space? This is important to me for a lot of reasons. Something that takes up a lot of space comes with a lot of drawbacks and thus I need to be extremely sure about a purchase if it’s going to be bulky.

What’s the problem with a large item? It takes up space in my home, which means that I need the space to house it. That space comes with a direct cost in terms of the portion of my home it takes up. If I have many large items, I either have to ditch some of them or get a larger place to live, and that’s pricy.

Furthermore, moving becomes progressively more difficult when you have more large items. You have to rent a larger truck or pay a moving service more. I simply don’t want to deal with it unless there is an extremely good reason.

Is this item something I can make myself? This question often applies to food items, which I can usually make for myself at home. A great example of this is the spice mixes I noted earlier in this article. I could have gone home and looked up the recipe for that spice mix and simply made it myself in an empty shaker bottle.

Take food purchases, for example. When I’m considering many food purchases, what I realize that I’m actually buying most of the time is a slightly lower quality (or sometimes much lower quality) but much more convenient version of something I could make for myself at home, and unless it’s complicated, I’d rather just make it myself unless it’s something I’ve never tried before. I don’t mind buying raw ingredients but I’m less and less interested in buying food for convenience.

Does this item do something new, or does it merely replace things I already have? This is an important distinction because each side of this coin triggers a different set of questions and things to think about. Let’s look at these divergent paths.

If it’s new, is there a less expensive way to test drive the new experience before investing this money? The thing I’m really looking at here is the new actions in my own life that this new item will cause. Whenever you buy something new, you’re theoretically trying to imprint some change in your life that you honestly aren’t sure about in terms of whether it will “take.”

For example, let’s say I’m interested in buying a musical instrument with the goal of teaching myself how to play it. While I might eventually want a good instrument that’s well built and sounds good, it’s kind of silly to invest a lot of money in an instrument that I’m not sure I’m going to really get into playing. I’m much better off finding a beat-up used instrument for learning and initial practice. That way, if I do decide that I really want to dig into this, I can always flip that older used instrument for most of what I paid for it and buy a much nicer instrument.

If it’s a replacement, what am I actually gaining for this additional expense? Ideally, I’m replacing a broken (or nearly broken down) item so that what I’m gaining is the core functionality I need. However, if I’m replacing a fully functional item that isn’t in danger of failing, what am I actually gaining?

For example, part of me wants to upgrade to the current generation of iPads. I use my iPad all the time for notes and other things and there are a number of little improvements I’d really like, but is it worth the several hundred dollar upgrade cost to have much more convenient recharging of my Apple Pencil? It might be nice, but when I put it in that context, it seems ridiculous.

Is it easily compatible with things I already have, or are other upgrades going to be necessary? Some items require other items to function. For example, if you buy a new cell phone, it’s likely you already have charging cables that will work with it… or might not work with those old cables at all. An upgrade that requires a bunch of peripherals to be replaced as well adds an additional cost.

Keeping with the phone example, many phone upgrades require buying a new case to keep them safe, which is an additional cost added on to the upgrade that most don’t consider. New kitchen appliances sometimes end up requiring new peripherals and attachments. For some, clothing items often require new accessories. New electronic devices sometimes end up triggering a domino effect of other purchases, like a new video game console replacing an old one and requiring new game purchases to be enjoyed.

These things need to be carefully considered and, if you’re not happy with that new upgrade chain, you should avoid the purchase unless there’s a strongly compelling reason to go ahead with it.

Am I going to be compelled to replace older things by comparison, and if so, am I really gaining enough value overall? This addresses the Diderot effect, which I wrote about last week and in an earlier article a few years ago (thanks to reader Rex for pointing that out; I had completely forgotten my earlier article when writing the new one, which is why they cover some of the same material and some different things, too).

If I buy a new article of clothing, is it going to make the rest of my wardrobe look really shabby by comparison and then convince me to start replacing lots of clothes? If so, the I need to consider that as part of the expense. Is this really the time to start replacing my wardrobe (or a significant part of it)? What do I really gain out of it?

When I step back and look at the clothing I have, I’m actually pretty happy with it. It only seems bad in comparison to a really nice new shirt or something. Without that new shirt, everything is great.

In general, this thinking leads me down the path that leads to my current wardrobe strategy, which is to buy individual well-made items that last a long time and only replace them as needed. (Surprisingly, I find them on occasion at secondhand shops, where someone takes in a really nice item of clothing that seems to have been barely worn.) That way, I tend to think of clothing items on a more individual basis. Does this item look excessively worn by my own standards? If so, I should replace it. If not, I don’t need to shop for clothes.

Could I just borrow this item from someone or someplace? If it’s an item that you’re just going to use for a while and then stick on a shelf, like a movie or a book or a video game, ask yourself whether or not you can just borrow it instead. The same is true for a tool or other device that you need for one task and then you’re probably just going to stick it in the closet or in the garage.

Does the library have a free copy available that I can borrow or request? Are there any places that offer the item for rent, like a hardware store or a Redbox? Does a friend have this item and would allow me to borrow it?

Buying something you only need for a short while should be avoided. Save your purchases for things you’re sure that you will use many times over a long period of time.

What about the opportunity cost? Whenever you spend $X on something, that means you no longer have those $X to spend on anything else. Is this use of $X the best use of $X you can conceive of right now? Is this really the thing to use that money on?

If I’m considering spending $50, I spend time thinking about the other things I could use that $50 for, both now and later. Are there things I would rather have than what I’d spend this $50 on?

Will I still be happy with this purchase a year from now? Five years from now? Purchases that provide a short term burst of joy and use only to quickly fall into disuse are not wise purchases unless that initial experience is amazing. I prefer to buy things that I’m still engaged with a year later or, ideally, five or more years later.

When I look at my Steam library (in other words, the computer games I’ve bought over the last decade), most of them were purchases on sale that I played for a few hours and then basically uninstalled and forgot about. Those were poor purchases.

The good purchases were the ones that I’m still playing years later, which is actually a very small handful of games. If I’m going to spend money on a computer game, it’s a good idea to just buy an expansion for those games or something in their vein.

It’s worth it for me to consider what those games have in common and then look only for new games that have those threads.

The same goes with books. What books on my shelf are ones that I’ve had for years and still read occasionally and get value out of as a reference book or as a book I’ve read several times? Books that don’t have something strongly in common with those items probably aren’t smart buys for me at this point – those books should be borrowed. Perhaps those borrowed books will prove themselves to me and eventually be purchased, but the odds are relatively low.

In the end, do I really want this thing? After asking all of these hard questions, I come back to the core of the matter. Do I still really want this thing, even after addressing all of the issues with buying it?

I dredge all of the items on the list through these questions several times before they make the cut. If I start realizing that this purchase isn’t worthwhile, I just delete it from the list and it’s forgotten. If I change my mind later, I add it back on at the bottom.

Doesn’t This Just Take the Fun Out of Buying Stuff?

Yeah, and that’s a big part of the point. Spending your hard earned money shouldn’t be fun. That feeling of “fun” is disguising the cold hard fact that you’re spending your hard-earned resources and losing all of the opportunities that those resources bring to you.

I don’t mind spending my money on something I genuinely want, but I want to make absolutely sure that I want it first and that I’ll have a good use for this item in my life. If that’s not true, then I’ve just spent my money on something that’s not bringing value into my life, and that’s the surest route to financial frustration. I would far, far rather have my money sitting in my checking account or savings account or investments than have some item that I don’t really like or have a use for.

I prefer to find my “fun” elsewhere, outside of spending money on things I don’t need.

Final Thoughts

In general, I don’t want to buy stuff. That’s a change in perspective from where I was in life several years ago, when I very much wanted to buy things. I’ve learned that when you buy things, they often end up underwhelming you when you bring them home. I’m interested in things that exceed my expectations or handle things I really want to do very well. I’m not interested in things that don’t.

The point of these questions and this process is to do my best to filter those purchases before I make them. I do this for lots of non-essential purchases, even relatively small ones.

Not only does this process help me filter out good and bad purchases as I go, it also helps me hone my own internal sense of worthwhile purchases so even my spur-of-the-moment spontaneous buys are of higher quality.

Consider using these questions and some kind of similar system for your own non-essential purchases. You’ll not only find that they help you start to eliminate the things that aren’t big wins in your life, but they’ll also help you hone your shopping instincts.

Good luck.

The post A Mental Toolbox for Avoiding Unnecessary Purchases appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/2Kr7l9h

10 financial chores you need to tackle now

Source Moneywise - 29 years of helping you with your finances https://ift.tt/2GCdQoj

How can I minimise IHT on a £150,000 gift to my son?

I have taken a 25% lump sum from my self-invested personal pension plan (Sipp). The plan is to gift the £150,000 to my son to help him buy a house. Should I make the gift paperwork in joint names with my wife with no breakdown of the amounts shown? Or should I show 50% from each by way of a £75,000 transfer to my wife’s bank and then send £75,000 from each of our bank accounts? I’m aware of the seven-year inheritance tax (IHT) rule and my son’s IHT liability when I die.

My thoughts are that if I make the gift solely in my name then on my death my son would face an IHT liability. Whereas if the gift was made jointly with my wife, then he would be liable to IHT only on the remaining parent’s death. Could you confirm that this is right?

As the gift you are looking to make is more than the allowance exempt amounts, this would be treated as a potentially exempt transfer (PET) for IHT purposes.

For a PET to be free of IHT, you need to survive for seven years after making the gift.

If you die within seven years of making a PET, and the total of all PETs you make is less than £325,000, then the value gifted will simply reduce your nil-rate band on your death. Your nil-rate band is the amount your estate can be worth before any IHT becomes payable.

So while this means that those receiving the gifts won’t be liable to tax, it also means that you won’t make any IHT savings by making these gifts.

It is only if the total value of PETs that you make is more than £325,000 that your son would face a potential IHT bill on your death. The tax bill would reduce on a sliding scale if your death occurs between three and seven years after making the gift.

So, assuming you make the gift on your own, the total value of gifts you make is less than £325,000, and you die within seven years of making it, your nil-rate band would reduce by £150,000 (assuming you’ve made no other PETs) from £325,000 to £175,000.

If you make the gift jointly with your wife, you will be deemed to have gifted £75,000 each and as a result, if one of you dies, the value of their nil-rate band would reduce from £325,000 to £250,000.

For IHT purposes, the gifts from you and your wife will be assessed separately when each of you dies and won’t be delayed until after the second partner’s death. So, you would be better off gifting the money jointly with your wife.

Source Moneywise - 29 years of helping you with your finances https://ift.tt/2ZhdWcw

الاثنين، 29 يوليو 2019

Questions About MLMs, Safe Deposit Boxes, Package Theft, Clark Howard, and More!

What’s inside? Here are the questions answered in today’s reader mailbag, boiled down to summaries of five or fewer words. Click on the number to jump straight down to the question.

1. Spouse withdrawing tons of money

2. Small benefit insurance

3. Nudging child out of nest

4. Getting out of Scentsy / MLM

5. Thoughts on safe deposit boxes

6. How to stop package theft

7. Clark Howard radio show

8. Borrowing money to invest

9. Elderly parent in decline

10. Easiest pasta at home?

11. Computer games?

12. Books with Impact suggestions

For a week each summer, our children go away to visit their grandparents, splitting the week between Sarah’s parents and my parents and effectively giving Sarah and I a child-less stay-cation for a week.

It’s incredibly enjoyable to not have to worry about them for a few days and to have some time alone with my wife. We’ve had children at home for more than a decade and we’re going to have at least one child at home for at least the next decade going forward.

At the same time, there’s a bit of an underlying realization that this is what our house will always be like when they move out. It will be much quieter and less lively. I suspect that Sarah and I will host a lot of dinner parties and game nights and get more involved in community groups when they move out, just to keep up the liveliness.

When I was younger, I never quite got why my parents and Sarah’s parents always seemed so genuinely happy when we would visit for a weekend or for the holidays and why they’d rush around and make our favorite meals. I love going to visit them, but it never quite clicked why that was the case.

Now I get it. There’s going to be a time eventually when the house is quiet and I’ll give anything for it to be lively again with our three kids there.

On with the questions.

Q1: Spouse withdrawing tons of money

Recently found out that my wife has been withdrawing about $500 in cash per week from our checking account. I have no idea what she’s doing with it. Initially very angry but decided to wait before confronting her. What should I do?

– Marcus

Remember, you don’t know for sure where this money is going. Some of the answers can be relatively innocuous – perhaps it’s being used in large part to pay for ordinary things or even being used in a productive way. Some of the answers can be more troubling. Whatever the reason, you don’t know what it is yet, so don’t jump to conclusions.

At some point, you need to bring this up in a non-angry and low confrontation fashion. Your best approach would be to gather up recent bank statements, whether printed off or elsewhere, highlight all of these withdrawals, and simply ask where this money is going.

Your spouse is likely to respond in an emotional way, with defensiveness or anger or sorrow. Expect that this will happen and don’t elevate your own emotions. Instead, when you figure out what the source is, give yourself some time to figure out what comes next. Don’t escalate your own emotion along with hers. Keep calm, gather information, then take some time to think about what comes next.

It may be that there’s a reasonable explanation and no changes are needed. It may be that some changes are needed in how you guys handle your finances. There may be other challenges. The point is, you don’t know, and the first thing you need to do is gather information, and you need to do that as calmly as possible.

Q2: Small benefit insurance

I have a question about paying for things like short-term disability insurance and accident insurance. Paying a monthly premium for an event that may or may not happen has never made sense to me. If I pay $15/month premium for the unlikely event that I might break my arm or end up in the hospital, I might get $500-$1,000 payout, but wouldn’t I have been better off just saving $15/month and having an emergency fund? There’s no guarantee that I’d ever have an accident, and I could be paying hundreds or thousands into insurance premiums over the years to never see a dime paid out or to not get the amount paid out that I had paid in. How do you assess the risk vs. the benefit and justify paying for insurance plans – or not? Aren’t we better off just keeping an emergency fund?

– Anna

Insurance is only valuable in terms of the negative consequences of an unexpected event that it protects you from, and that varies a lot from situation to situation and from person to person.

For example, if you have a policy that only pays out $1,000 in a specific uncommon event and it has a less than 1% chance of occurring to you in a given month, then you’re better off putting $15 per month into an emergency fund. That’s basic math.

In general, insurance is most valuable when it protects against something catastrophic, like the death of an income-earning spouse or parent, and the policy provides enough of a payout that it makes up for at least some of the shortfall, preventing a disastrous financial situation for the survivors. If you can easily afford the financial consequence of that situation out of pocket, insurance doesn’t make much sense.

Where it does make sense is in situations like that death of a loved one. Imagine that you’re married with a couple of kids and your spouse makes as much as you do. One day, your spouse suddenly and unexpectedly dies. That’s going to have a very bad impact on your finances and standard of living beyond just that of losing a spouse unless you happen to have enough cash sitting around not earmarked for anything that could make up for your partner’s income for many years. Very few people have that, so life insurance makes sense.

Yes, most insurance policies only pay out in rare circumstances, but people buy insurance because those circumstance are dire and they’re still common enough that they do regularly happen to people. If those circumstances aren’t actually dire for you, then you don’t need the policy.

For small policies like the ones you name, if you have more than enough in your emergency fund to handle the expenses related to the event that would trigger the policy, you probably don’t need the policy.

Q3: Nudging child out of nest

We have a 20 year old son who lives at home while he goes to nearby university about 15 miles away. He has a part time job on campus there. We don’t have any conflict with him living here but we have a strong sense that after graduation he intends to keep living here, and we don’t think that’s a good idea long term for any of us. We are looking for simple ways to encourage him to get out of the nest when he graduates or even before. Do you have any suggestions?

– Adam

One of my college friends lived at home and her parents had what I considered to be a really good arrangement with her. While she was in college, each month they put some amount into a “moving out” fund for her. When she graduated, she was welcome to stay at home, but each month she did so, they put less into the fund. After six months post graduation, they stopped contributing to the fund and in subsequent months they started to take money out of the fund to pay for some of the costs of her continuing to live at home.

In other words, a couple of months after graduating, it quickly became a matter of diminishing returns for her to live at home. If she moved out then, she basically had a year’s worth of rent covered. The longer she stayed at home, the less and less rent was covered, and if she had stayed at home for a couple of years, the fund would have entirely vanished.

This motivated her to move out quite effectively.

Aside from something like this, I think the best tool in your arsenal is communication. Talk to your partner about what kind of timeline and what situations you’d like to see for your child to move out, then once you’re on the same page, open up those discussions to your child and make it clear what you have in mind before it ends up being a difficult situation.

Q4: Getting out of Scentsy / MLM

My sister has sold Scentsy rather aggressively for the last two years but recently said that she is thinking about getting out of it but doesn’t really know how. Do you have any advice?

– Erika

I don’t know the absolute specifics of how the Scentsy program works, but almost all MLM programs work along the same lines.

The first thing she needs to do is to cut herself off from her upline or sponsors. Delete group chats, block those people, ignore and block their texts. They’re going to apply a lot of pressure to keep her selling Scentsy, so she needs to cut them off.

If she has any automatic shipments of Scentsy products, she needs to cancel them immediately. She should also look into whether or not there are any buyback or return policies; I poked around the Scentsy website but couldn’t find any. If she has stock that isn’t already sold, she should tell people that she’s ending her Scentsy “business” and is selling what she has at a discount.

Beyond that, she should spend some time talking to anyone in her personal life that she used aggressive selling tactics on while selling Scentsy. MLMs damage relationships and they have to be repaired. This can be hard.

If she has any downlines or people she’s sponsored, she needs to have a chat with them, too. Keep it simple, though – she doesn’t have to reveal everything about her life.

The hardest part is going to be ignoring the pressure from the upline/sponsor to keep selling. They have a basket of tactics to use to keep their downlines in line and they will use them. Be there for your sister, because this will probably be hard for someone who was really into selling just a short while ago.

Q5: Thoughts on safe deposit boxes

Do you still recommend safe deposit boxes as a place to put valuables? https://www.nytimes.com/2019/07/19/business/safe-deposit-box-theft.html

– Erik

After reading this article and doing some homework, there are three things worth pointing out.

First, anything you put in a safe deposit box should be insured. Check with your homeowners insurance to see whether coverage is extended to the contents of such a box and, if not, whether it can be extended to it. You may have to take out a separate policy for a valuable collection, but the premiums on a collection stored in a bank vault are pretty low.

Second, the contents of a safe deposit box are much less likely to be broken into than your home. They’re also much less likely to be damaged in fire than your home. That does not make them riskless. It simply means the risk is much lower.

Third, a safe deposit box is a good place to put documents that aren’t significantly valuable on their own but could be really difficult to replace, like deeds and Social Security cards and so on.

I do keep a small number of reasonably valuable collectibles in our safe deposit box. They do not have enough value, in my opinion, to insure on their own. I mostly just want to have them in a separate and rather secure place besides our home.

Q6: How to stop package theft

I think that someone is stealing packages off of my front step but I don’t really know how to prevent it. About half the time in the last six months when UPS or FedEx or post office leaves a package for me, it has vanished. At first I thought it was a fluke but it’s pretty clear someone is either targeting my house or walking through the neighborhood grabbing packages. What’s a good solution for this that isn’t really expensive?

– Jerry

The best solution, though it’s kind of expensive, is to buy a parcel drop box. This allows packages to be deposited in a large opening at the top and then they drop down into a locked box below. You then unlock that box when you get home and there’s your package. I’ve seen these in a few front yards as of late.

You can also put up a small camera ($50 or so) and a sign indicating that the property is under surveillance. Then, if someone actually takes the package, you can watch the video and see what happened. This can help you and your neighbors get rid of the package thief entirely.

The best free (or low cost) solution is to talk to the delivery services and see if you can have your packages held at their location so you can just pick them up when they arrive.

Another approach would be to talk to the police in your area and report that packages are consistently being taken from your front step in a particular timeframe and likely from other homes in the area.

Q7: Clark Howard radio show

Any thoughts on the Clark Howard radio show? He seems to mostly say sensible stuff.

– Bill

90% of the time, Clark Howard does a very good job of making solid personal finance advice into an entertaining radio show. Of the people on the radio who talk about personal finance, he’s probably the one I like the best.

What about the other 10%? It seems like sometimes he starts talking positively about companies and how great they are and I just don’t see why. I’ve assumed that there is some paid product placement in places during his show, but I don’t know that – there’s just parts that feel very off when he’s recommending products or companies, like he’s talking about a company that really isn’t a great bargain or isn’t anywhere near the best in a particular market as though they’re a fantastic deal.

If you avoid his specific product recommendations (and tune out the ads), his show is pretty good.

Q8: Borrowing money to invest

What do you think of the idea of taking a cash withdrawal from a 0% interest credit card and investing that money now, then paying it back over time before the 0% interest rate deal ends? Seems like that would get money into a Roth faster at the start of the year instead of spread throughout it.

– Barry

While this can gain you a little money in your Roth if everything goes well, it comes with significant risk. You’re essentially banking on everything going well in your life, and if it doesn’t, this strategy could cost you a great deal. Plus, there’s the inherent stock market risk – there’s not a guarantee that this will make you money. You’re essentially taking out a favorable loan to make a short term stock market play, and the stock market isn’t a great short term investment.

I wouldn’t do this. You should take out 0% credit card offers in an effort to reduce financial risk in your life, not increase it. Use those things to pay off credit cards that actually have a balance or other fairly high interest debt. That’s a move that reduces your personal financial risk. Use such an advance to buy a necessary purchase instead of using a credit card with interest or using cash savings. That’s another move that reduces your personal financial risk.

This is a bad move.

Q9: Elderly parent in decline

My husband and I are in our mid 60s. We have not yet retired but were planning to do so around 70. My mother is 91 years old and on the verge of no longer being able to live independently. I am her only living child. She is still sharp of mind but her body is very frail. She currently receives a pension from the state plus Social Security so she’s better off financially than many people her age but her medical costs are really starting to ramp up.

The big issue is that we want to be able to move her in with us but our home is not accessible for her in any way. The cost of building on a room for her with a handicap accessible bathroom and easy access to kitchen and living room is expensive but doable for now but we are not sure we will be able to recoup the investment later if we sell the house.

Do you have any advice for our situation? Things we can look into or think about?

– Karen

The best advice I’ve found for this situation comes from AARP, as this is the kind of issue that they handle extremely well. I found this article on the decision to live with aging parents to be really valuable.

In short, the best thing you can do right now is to communicate a lot with your husband and then with your mother, and then when issues of concern come up, research those specific areas of concern.

As for the home addition, your best approach is to start gathering quotes sooner rather than later so that the room is ready when you need to make this move. If you and your husband are really committed to doing this, get started now so that everything goes as smoothly as possible. This means starting with some serious conversation as soon as possible.

We’ve had a bunch of heavy questions this week, so let’s finish up with three lighter ones.

Q10: Easiest pasta at home?

Want to try making pasta at home from scratch but don’t want to invest in a machine until I’m sure it’s worth it. Suggestions for first steps? Looked at some pasta cookbooks but they all jump in to the deep end.

– Alex

Make lasagna noodles by hand. Seriously. It’s not that hard at all and you don’t need a machine.

Use a simple homemade pasta recipe, like this one. It’s mostly just flour and eggs with a tiny bit of salt, olive oil, and possibly a bit of water depending on elevation and humidity. You basically mix flour and eggs until you make a thick dough, break it into small pieces, then roll it very thin, fold it over a couple of times, and roll it thin again. You basically just trim the edges a bit, cook it, and use it in lasagna.

When making lasagna, I actually think it’s worth the effort to make noodles like this instead of using boxed noodles. The homemade fresh noodles taste better and have a better texture in the mouth. I straight-up prefer them, though it’s not a life changing difference. They’re just easy to make.

For me, the real work of homemade pasta is cutting them into small noodles in any sort of efficient way (think spaghetti or fettuccine). This is easiest done by machine.

Q11: Computer games?

You said you spend a few hours a week playing computer games. What kind of games do you play?

– Adam

I basically play long simulation-style games. Over the last three years, aside from occasionally playing other types of games with my kids, I’ve really only played five computer games: Factorio, Stellaris, Northgard, Europa Universalis IV, and Civilization VI.

These are all relatively slow paced games where you spend time thinking about your next move and you can easily just save your game at pretty much any time and play later, though there is a strong “one more turn!” temptation with all of them. The only one that’s even “click-y” at all, and it’s very minimal, is Northgard.

I have several friends who play similar games and so I often talk to them about it, so it has a social component, but I play these games almost entirely solo. I enjoy them for the problem solving and the kind of slow and meditative pace.

My philosophy on computer games is that I’d rather play a game to utter death and earn most/all of the achievements rather than hopping from game to game.

Q12: Books with Impact suggestions

I have really enjoyed your Books with Impact reviews, especially when you write about personal finance adjacent books like personal development and productivity and leadership. Here are some books you might want to consider for this series.

Extreme Ownership by Jocko Willink and Leif Babin

Atomic Habits by James Clear

How to Be a Stoic by Massimo Pigliucci

A Guide to the Good Life by William Irvine

The Slight Edge by Jeff Olson

I look forward to reading your summaries and thoughts on these!

– Jared

Believe it or not, all five of these are on my list of personal development/personal finance books to read or, in the case of three of those books, to re-read. I tend to read a new book and re-read a different book in those areas about once every two or three weeks at this point.

The books I choose to actually review on here as a “Book with Impact” is one that I’ve read, then re-read, and also applied the content within in some successful fashion in my own life in a lasting way or it impacted my thinking in a meaningful and lasting way. I read a lot of good books, but they’re usually not ones I end up applying in any sort of meaningful and lasting way aside from perhaps a minor tactic or two.

I have about five or six books that are definitely going to be covered in this way in the future, and the books on my re-read list number about 20 and at least a few of those will probably pop up. My “to be read” list is much longer, but I usually prioritize ones that my readers ask me about, and that means that the ones above that I haven’t read are likely to be read or re-read soon.

If you have any suggestions for personal finance books, personal development books, productivity books, or books that just made you think a lot about the general direction of your life and perhaps the role that money plays in it, please send them to me at the link below (along with any other questions for the mailbag you might have).

Got any questions? The best way to ask is to follow me on Facebook and ask questions directly there. I’ll attempt to answer them in a future mailbag (which, by way of full disclosure, may also get re-posted on other websites that pick up my blog). However, I do receive many, many questions per week, so I may not necessarily be able to answer yours.

The post Questions About MLMs, Safe Deposit Boxes, Package Theft, Clark Howard, and More! appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/2SU5VI8

A Life Well Lived

One of the best people I’ve ever known celebrated his 90th birthday very recently. His children put together a wonderful birthday party for him and invited tons of people – old friends, extended family members, all kinds of folks. There were people I knew well, people I knew vaguely, people I didn’t know at all, all drawn together to celebrate this occasion.

At events like this, the most wonderful part is how our shared relationships with this guy drew us all together. It was the common touchstone for all of us, and because of that, stories about him flowed. I wound up swapping stories about the guest of honor with all kinds of people and getting to know some of them along the way.

The thing that stuck out to me more than anything else was that people really don’t care what kind of house you have or what kind of car you drive or whether you have the latest gadgets. No one at that party cared in the least about any of that. They cared about the person – his humor, his kindness, his generosity, his good advice, his character, his reliability. So many of the stories involved the guest of honor opening his door to someone or showing up in a needed moment or coming through over and over again or doing something hilarious.

I didn’t hear stories about his house or the cars he drove or the fancy restaurants he dined at or how well he dressed or anything like that. That’s not what drew literally hundreds of people to his party. That’s not what filled all the bedrooms in several nearby houses and had people camping in tents and campers.

He spent much of the party holding court, with people sitting down to chat with him for a bit, then making room for other people. The sheer number of people and memories that shifted across his table in that afternoon was almost unbelievable, a true celebration of a lifetime of memories.

When I’m 90, what will I remember?

I won’t remember going out to expensive restaurants with my wife or with my friends. I will remember eating with them and laughing with them and enjoying their company.

I won’t remember the expensive watch I owned forty years ago. I will remember a random lazy afternoon with my kids when we rolled down hills and blew tufts of dandelions.

I won’t remember that I had the latest and greatest smartphone. I will remember being able to be there for a friend, and when they were there for me.

I won’t remember the books that filled my bookshelf. I will remember the things I learned from reading books, the lessons they taught me, and some of the great stories.

When I’m at my 90th birthday party, I don’t want to hear people talking about my board game collection. I’d rather hear them talking about the time we stayed up most of the night playing a game together, or how I showed up at their doorstep when they were down with a sack of food, some beverages, and a board game and spent the evening with them.

When I’m at my 90th birthday party, I won’t remember the exact details of some trip I went on with friends years and years ago, but I will remember us doing something new and laughing together.

When I’m at my 90th birthday party, I won’t remember the money I frivolously spent, but I will remember when I was able to help a friend and when they were able to help me.

Those are the things he remembers and laughs about when he talks about his life. Those are the sources of the pieces of wisdom he offers, the things that just come naturally from him. Those are the things that people talk about when they talk about him.

His old farmhouse isn’t full of expensive artifacts from forgotten trips. They’re full of meaningful memories, of things made by him and things made for him by loved ones, of photographs, of well-used and well-loved functional items.

The people who came to that party weren’t there hoping for a spot in a will. They were there to appreciate a wonderful person. They remember his character. They remember time spent with him. They remember the skills he had. They remembered what he gave of himself.

Those things aren’t bought. They’re earned over a lifetime of living.

When I look ahead at the life I have yet to live and I ask myself whether I’d rather have a house full of stuff or a life full of good memories and great relationships, I want the latter, and it’s not even a question.

That’s why my financial plans are largely in service of that. I want to have a life that gives me the ability to be there for friends, to be a part of people’s lives, to be more than just a career and a shiny car and a nice house.

I don’t want to end up in an empty house full of stuff with my kids counting down the days to clean it out and sell it off, without friends and people in my life.

With every year that has passed, he has taught me how to live that life. You don’t get there by spending money on forgettable things. You get there by spending time and care on the people in your life. You don’t get there by getting. You get there by giving.

Later that evening, as the festivities were winding down, I wound up sitting fairly close to the guest of honor, engaged in a conversation that he was merely listening to. I looked over at him and he looked absolutely tired, but he had this half-smile on his face that simply said he’d rather be there than anywhere else in the world.

After he went to bed, about forty people were still hanging out, playing cards and swapping stories and laughing. I can’t imagine a better sound to fall asleep to.

Thanks for the example, Herb.

The post A Life Well Lived appeared first on The Simple Dollar.

Source The Simple Dollar https://ift.tt/30VUaUa

الأحد، 28 يوليو 2019

Pike County needs a hospital closer to home

Source Business - poconorecord.com https://ift.tt/2OlMBEN

Legal cannabis could pose law enforcement challenges for Pa.

Source Business - poconorecord.com https://ift.tt/2Yc0J86

A hospital closer to home

Source Business - poconorecord.com https://ift.tt/32Tipo1

السبت، 27 يوليو 2019

Get Paid to Read and Review Books from Home

How would you like to get paid to read books and share your opinion of them? If you have a love for reading, then a paid book reviewer job is the perfect work-at-home opportunity for you! Whether you’re sitting on the couch in your jammies or beachside in your bathing suit, you can cozy up […]

The post Get Paid to Read and Review Books from Home appeared first on The Work at Home Woman.

Source The Work at Home Woman https://ift.tt/311UX65

Is NEPA underserved for hospitals?

Source Business - poconorecord.com https://ift.tt/2yton0V

The Value of Time Tracking – And How I Do It

Over the past few years, I’ve made several small references to the fact that I’m a pretty active time tracker. I like to keep track of what I do with my time throughout the day, to the best of my ability, and I find a ton of value not just in doing so, but in the accumulated data.

A few readers over the years have touched base with me on the subject, asking for more details, so I thought there might be value in explaining the full system in detail – why I do it, how I do it, and what value I get from the results. There are definitely some real financial and professional benefits, and benefits in other areas of life, too.

What Is Time Tracking?

Time tracking is pretty much exactly what it sounds like. I simply keep track of my time use each day. Any time I do something for more than about five minutes, or if I interrupt an ongoing task for more than about five minutes, I record that.

Let’s say I wake up in the morning and I decide that I first want to take a shower and get dressed for the day. I mark the time, that I’m no longer sleeping, and that I’m now practicing morning hygiene. When I’m done with that and I decide I want to meditate, I mark the time, that I’m no longer doing morning hygiene, and that I’m now meditating. This goes on and on, to the best of my ability, until I’m ready to go to sleep, at which point I mark the time, that I’m no longer doing whatever it was I was doing right before bed, and that I’m now sleeping. I’ll get into the mechanics of this in a bit, but it takes me less than a second to record those transitions, so it’s practically effortless.

In general, I don’t bother recording very short things, less than five or ten minutes or so. I’m more interested in the larger blocks of time I devote to things like sleep, work, hygiene, meals, hobbies, and so on.

I do not aim for perfection. That would be impossible. Instead, I just aim to get as close as I can to recording the actual edges of the significant chunks of time throughout my day. I’m never absolutely perfect at it.

Why Do It?

The first question most people ask when they hear about this is why. Why would a person even want to do this?

This actually is a practice that I started using at my previous job to document my personal time. I was frustrated by my performance reviews and felt that the reviews didn’t actually assess all of the different things I was actually taking care of and responsible for at work, so for the last year or so of my job, I started tracking my time very carefully using an Excel spreadsheet, doing it all manually. I wanted to produce documentation that showed that I spent X hours in an average week – and Y hours over the last year – doing a particular task and so on. So, the entire thing was initially borne out of a frustration with managers not really understanding or appreciating all of the things I was quietly doing and maintaining.

I learned several things as I was doing this.

First of all, the act of time tracking nudges me to make better use of my time. When I made the conscious decision to be as honest as possible with my time tracking, I quickly realized that I didn’t want to track silly uses of my time. If I were to look at my time tracking data at the end of the day or the end of the week or the end of the month and think to myself that some of those entries were absolutely wasteful or silly, that wouldn’t feel good. I don’t want to see entries like that in my data. So, during the day, I consciously choose things to do that will look better in the data.

This is very similar to the phenomenon of writing down every dime you spend. If you do that honestly, there will be bad expenses that you don’t want to write down, and that desire to not have to record that silly expense pushes you away from that expense. You don’t want to write it down, so you don’t do it.

Second, time tracking keeps me on task. I have a rough rule that if I’m stepping away from the task at hand for more than five minutes, I write down that the task has ended and that I’m moving on to something else. This actually does a great job of keeping me on task. I recognize that if I start browsing websites for very long, I’m actually effectively ending the block of time I spent on task and, as noted above, I don’t want to do that, so I find myself nudging away from pure time-wasting activities.

Finally, time tracking data is incredibly useful, especially as I accumulate more and more of it. I’ll get into this below in the “How I Use the Data” section, but suffice it to say that the data has a great deal of value, professionally, personally, and financially. The things I’ve learn from looking at the time tracking data I’ve accumulated have helped me make better career decisions, make better hobby choices, make better personal decisions, and so on.

When I walked away from that job, I found that the unstructured life of self-employment and contracted work made it very easy to start using time in a … let’s say, less than optimal manner. After a while, I began to realize that I needed to figure out better practices for using my time, and that’s when I returned to time tracking, and I’ve more or less been using it constantly over the last several years. I found that the benefits it brought to my professional life back then actually exist in almost every aspect of my life now.

How I Track My Time

So, how do I actually pull this off without being overly clunky?

For me, the number one most important principle of time tracking is that it must require absolute minimum effort to actually track time. When I first started doing this, I would manually track time in a spreadsheet document, and that was often cumbersome. I had to develop a set of codes to use to make the entry more efficient, but even that was fairly slow. It is very likely that if I were still recording my time manually on a spreadsheet or with a piece of paper, I wouldn’t still be doing it.

The big change for me was the arrival of online services that handle time tracking for you. They basically handle all of the data tracking and reduce it all down to a single button click, though there is a lot of setup work that needs to be done to make it work that well.

I’ve tried a bunch of services and the one I’ve been using for the past few months is far and away the best one I’ve ever used. I use Timery, which is an app that serves as a very user-friendly front end for the Toggl time tracking service. This might require a bit of explanation.

I have been using Toggl as my time tracking service for years because I like the way they handle all of the data that I’ve recorded. The only problem with Toggl is that their actual data entry tools are a bit cumbersome. I usually use my phone or (occasionally) my tablet to record when tasks start and end, but the tools Toggl provides themselves require several taps to do almost anything, which often takes me out of my train of thought.

Timery‘s entire focus is on making data entry into Toggl as simple as possible, reducing most of the time entry down to a single tap off of the Control Center screen on my phone or tablet. I can literally do it in less than a second, fast enough and thoughtless enough that I don’t have to break whatever I’m concentrating on. This has been a revelation for me.